Skip to content

Skip to content Managing a loved one’s trust can feel overwhelming—but with the right legal guidance, it doesn’t have to be. Taking on the role of a trustee is a significant vote of confidence, but it often comes with a nagging question: are my own personal assets now on the line?

The short answer is, yes, they certainly can be. While you're not automatically liable for every bump in the road, Texas law holds trustees to an exceptionally high standard. A few wrong moves could put your personal wealth at risk, making it crucial to understand your responsibilities.

The Weight on Your Shoulders: Understanding Trustee Personal Liability

The idea of trustee personal liability in Texas is enough to make anyone nervous. Our goal here isn't to scare you, but to empower you with clarity. When you know the rules of the road, you can navigate your duties confidently while keeping your own assets safely protected.

The law sees a trustee as a fiduciary. This is a formal term for someone in a position of sacred trust. It’s the highest standard of care our legal system recognizes, meaning you have a legal and ethical duty to act only in the best interests of the trust and its beneficiaries.

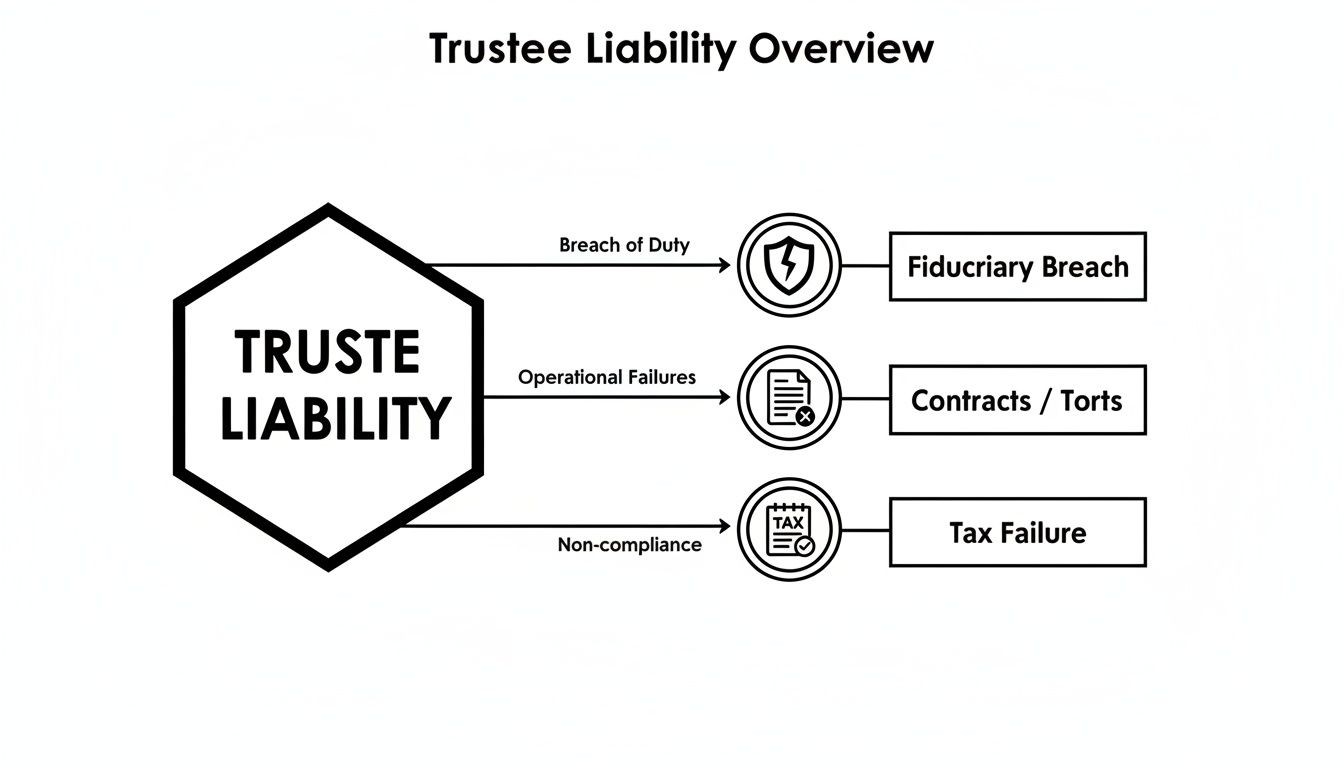

Where Does Personal Liability Come From?

Under the Texas Trust Code, you generally aren't personally liable for contracts you sign for the trust, provided you make it clear you're acting as the trustee. The real danger zones are actions—or inactions—that violate your core duties as a fiduciary.

A trustee is personally liable for torts committed in the course of administering a trust…only if the trustee is personally at fault.

That phrase, "personally at fault," is the key to understanding your risk. It covers everything from simple carelessness to a major breach of duty.

For example, say the trust owns a rental property. If you, as the trustee, ignore repeated requests to fix a rickety handrail and a tenant gets hurt, you could be found "personally at fault." That means the liability could jump from the trust's bank account directly to your own.

This guide is designed to give you a solid foundation, demystifying personal liability so you can serve as a trustee without fear. We’ll walk through the specific missteps that create risk and provide practical, real-world steps to protect yourself. By understanding the core principles of fiduciary duties in Texas, you can manage this responsibility effectively and honorably.

Your Shield Against Liability: Mastering Fiduciary Duties in Texas

Think of your fiduciary duties not as a heavy burden, but as your best line of defense against trustee personal liability in Texas. Mastering these core principles isn't just about following rules—it's the single most powerful way to protect your personal assets while honoring the immense trust placed in you. When you commit to these duties, you build a legal fortress around your decisions, making it incredibly difficult for a beneficiary to successfully argue you acted improperly.

The Duty of Loyalty: The Trust Always Comes First

The duty of loyalty is the absolute bedrock of your role. It’s simple in theory but demands constant vigilance: you must act solely in the best interest of the trust and its beneficiaries. Period.

This means you must avoid any situation that even hints at self-dealing or a conflict of interest. For example, you cannot sell your own property to the trust, even at a fair price. You also cannot lend trust funds to yourself or a close family member. These actions are textbook conflicts of interest and a direct violation of this sacred duty.

The Prudent Investor Rule: Managing Assets Like a Pro

The Texas Trust Code outlines the prudent investor rule, which is your playbook for managing the trust’s assets. This doesn't mean you need to be a Wall Street wizard, but it does require you to manage the trust's investments with the same care, skill, and caution that a sensible person would use for their own financial future.

This breaks down into a few key jobs:

- Diversification: You must spread the investments around to minimize the risk of a major loss. Putting all the trust's assets into one stock or one type of investment is rarely prudent.

- Balancing Risk and Return: You need to find the sweet spot between growing the investments and protecting the original principal, always keeping the trust's purpose and timeline in mind.

- Constant Review: Investing isn't a "set it and forget it" task. You have a duty to regularly review the portfolio and make adjustments based on the market and the beneficiaries' needs.

Failing here can have disastrous results. In one cautionary tale, a trustee invested 80% of a trust's funds into volatile tech stocks, going against the trust's conservative goals. When the market tanked, the court held the trustee personally liable for every penny lost.

Impartiality and Disclosure: Keeping Things Fair and Open

Two other duties are critical for keeping you out of hot water: impartiality and disclosure.

The duty of impartiality means you can't play favorites among the beneficiaries. Unless the trust document specifically tells you to, you must treat all beneficiaries fairly and balance their often-competing interests.

For instance, if a trust has an income beneficiary (who gets investment earnings now) and a remainder beneficiary (who gets what’s left later), you must invest in a way that’s fair to both.

Finally, the duty of disclosure requires you to keep the beneficiaries informed about the trust and your management of it. This proactive communication builds trust and nips misunderstandings in the bud before they can grow into lawsuits. Regular, clear communication is one of your best risk management tools.

The Legal Minefields That Put Your Personal Assets on the Line

Knowing your duties is like having a map, but knowing the common pitfalls is what gets you to your destination safely. Let's discuss the real-world mistakes that can entangle your personal finances in a trust dispute. These are practical, everyday scenarios that even well-intentioned trustees can stumble into.

A Breach of Fiduciary Duty

This is the big one. A breach doesn't require malice; often, it's a simple oversight or lapse in judgment.

Take self-dealing, for example. Imagine you're a trustee and also own a small IT company. The trust needs a new computer system, so you hire your own company to do the job. Even if you give the trust a fair price, you've created a massive conflict of interest. That’s a breach of your duty of loyalty, and beneficiaries could sue, demanding you repay every cent from your own pocket.

Another classic mistake is failing to manage assets prudently. If you let trust money sit in a low-interest checking account for years, inflation will erode its value. Beneficiaries can argue that you failed to grow the assets as a "prudent investor" would, and a judge might agree—holding you personally liable for the lost potential growth.

Liability for Contracts and Business Debts

A quick signature on paper can become a personal financial nightmare if you're not careful. Whenever you sign a contract for the trust—whether hiring a roofer or taking out a loan—you must make it clear you're acting as the trustee.

The Texas Trust Code offers you protection, but only if you properly disclose your role.

The only correct way to sign a contract is: "[Your Name], Trustee".

Simply signing your name without adding "Trustee" is a catastrophic error. The other party can claim they had a deal with you personally, not the trust. If the trust can't pay its bill, creditors will have a clear path to your personal savings, car, and home.

Improper Distributions to Beneficiaries

Handing out money seems easy, but it’s a field riddled with traps. The trust document is your bible; you must follow its instructions for distributions to the letter.

Picture this: A trust states that three beneficiaries get their shares when the youngest turns 25. One beneficiary is eager to buy a house, so you, trying to be helpful, give them their share two years early. But then the market tanks, and the trust's investments lose value. The other two beneficiaries can now sue you, arguing the early payout shrunk their inheritance. A court could order you to personally make up for the shortfall.

- Never give out money based on a verbal plea if it goes against the trust document.

- Always double-check a beneficiary's age or other milestones before cutting a check.

- Stay impartial. Don't give one beneficiary an advance if it could disadvantage the others.

When facing a tricky distribution, the smartest move is to talk to a Texas trust administration lawyer. It's a simple step that provides bulletproof protection.

Failure to Properly Manage Trust Taxes

The IRS and the Texas Comptroller expect tax returns to be filed and payments made on time. If you drop the ball on filing the trust's income tax return (Form 1041) or forget to pay property taxes on a house the trust owns, the penalties and interest can pile up fast.

Worse, that liability can jump from the trust to you. If your failure to pay taxes is seen as a willful act, tax authorities can hold you personally responsible for the entire debt. Getting your accounting right and hiring a professional for tax help isn't a luxury—it's essential self-preservation. Our team can help you build asset protection strategies that address these complex duties.

Common Triggers for Trustee Personal Liability

To help you keep these risks top-of-mind, here is a quick-reference table.

| Liability Trigger | Governing Principle (Texas Trust Code) | How to Prevent It |

|---|---|---|

| Hiring your own business for trust work | Duty of Loyalty (No Self-Dealing) | Always use independent, third-party vendors for all trust-related services. |

| Leaving assets in a low-yield account | Duty of Prudence (Prudent Investor Rule) | Regularly review and manage trust investments, diversifying to balance risk and growth. |

| Signing a contract as an individual | Contractual Liability (Sec. 114.084) | Always sign documents with your name followed by ", Trustee" to clarify your role. |

| Distributing funds too early | Duty to Follow Trust Terms | Adhere strictly to the distribution schedule and conditions outlined in the trust document. |

| Missing a tax filing deadline | Duty to Administer the Trust | Hire a qualified CPA to handle all trust tax filings and payments. |

Understanding these triggers is about empowering you to act confidently. By recognizing these common mistakes, you can take proactive steps to protect both the trust and your own financial well-being.

The Critical Risk of Unpaid Trust Taxes

Of all the duties a trustee juggles, managing taxes is where the personal stakes get incredibly high. This is one area where a mistake can pierce the veil separating the trust’s finances from your own, exposing you to trustee personal liability in Texas.

Failing to file and pay all required taxes—income, capital gains, or property—isn't just a slip-up. It's a direct threat to your personal assets. Both the IRS and the Texas Comptroller have long memories and little patience for non-compliance.

While many trustees worry about a beneficiary lawsuit, it's just as easy—if not easier—to get into hot water by failing to meet these external obligations.

The Texas Pig Stands Case: A Sobering Precedent

If you think this is just theoretical talk, a major Texas case serves as a stark warning.

In Texas, a trustee's failure to pay taxes can be considered a "willful" act, which gives tax authorities the green light to come after the trustee's personal bank accounts for the entire debt.

The 2013 case of Texas Pig Stands, Inc. is a perfect example. The Fifth Circuit Court of Appeals held a bankruptcy trustee personally liable for more than $100,000 in state sales taxes he "willfully" failed to pay. After taking control of the company’s assets in 2007, he used money from sales to pay other bills instead of remitting the required taxes. The court's decision sent a clear message: under Texas Tax Code section 111.016, trustees who knowingly mismanage tax funds cannot hide behind the trust—their personal assets are fair game.

What Does "Willful" Really Mean?

This is where many well-intentioned trustees get tripped up. In this context, "willful" doesn't require malicious intent. It can simply mean you knew a tax bill was due and either consciously chose to pay another expense first or acted with reckless disregard for whether the taxes got paid.

Actions that could be considered "willful" include:

- Using trust funds for distributions or other expenses when you know taxes are outstanding.

- Failing to set aside enough cash to cover future tax liabilities you should have anticipated.

- Ignoring notices from the IRS or the Texas Comptroller.

- Simply not filing the trust’s tax returns at all.

To protect yourself, engaging expert Tax Accountants is not a luxury; it’s a necessity. Impeccable record-keeping is your first line of defense. You can learn more about how to maintain transparent financial records in our guide on what is trust accounting. Think of professional tax help as an essential shield for your personal assets.

Legal Defenses and Protections for Texas Trustees

Taking on the role of a trustee can feel like walking a tightrope, but the good news is that Texas law doesn't expect you to perform this act without a safety net. When it comes to trustee personal liability in Texas, you have duties, but you also have defenses. Both the trust document and the Texas Trust Code provide powerful shields for trustees acting in good faith.

The Power of an Exculpatory Clause

Think of an exculpatory clause as a suit of armor built into the trust document. It's the creator's way of saying, "I trust you to do your best, and I don't want you on the hook for an honest mistake."

This clause is designed to shield you from personal liability for errors or simple negligence. However, this armor has its limits. The Texas Trust Code is clear that an exculpatory clause is legally worthless if it tries to excuse:

- Any breach of trust committed in bad faith.

- Actions taken with intentional or reckless indifference to a beneficiary's interests.

- Any personal profit a trustee makes from a breach of trust.

So, while it can save you from a genuine oversight, it offers zero protection against gross negligence or intentional misconduct.

Understanding Indemnification Rights

Another critical layer of protection is indemnification. This is a legal way of saying that the trust should pay for its own business expenses, not you personally.

If you are sued by a vendor for something related to the trust's administration—say, a "slip and fall" on trust property—you can use trust funds to cover legal bills and any settlement, assuming you weren't personally at fault.

Your right to indemnification is a cornerstone of trustee protection. It reinforces the principle that you are acting on behalf of the trust, and the trust itself should bear the financial burdens of its administration.

Seeking Guidance from the Court

When you're truly stuck between a rock and a hard place, you can petition a court for instructions. If the trust language is confusing about a distribution or beneficiaries are at war over selling a family property, getting a court order that blesses your plan of action provides a nearly bulletproof defense against future claims about that decision. It’s a proactive move that shows you're taking your duty of care seriously.

A deep understanding of your legal rights is crucial. For more information on what happens when these duties are challenged, you can learn about what constitutes a trustee breach of fiduciary duty in our detailed guide.

Your Trustee Survival Guide: Practical Steps to Avoid Liability

Being a trustee doesn't have to keep you up at night. With proactive organization, you can manage the trust effectively and keep your personal assets safe from the threat of trustee personal liability in Texas. Think of this as your personal playbook for administering a trust with confidence.

Keep a Flawless Paper Trail

Your best defense is a meticulous paper trail. Document every decision, transaction, and conversation about the trust. This isn't just about good accounting; it's about building an ironclad record that shows you did your job right.

Your records should be thorough enough to tell the whole story:

- A Decision Log: Jot down why you made certain choices, like selling a particular stock or choosing one contractor over another.

- Transaction Receipts: Keep every invoice, payment confirmation, and bank statement.

- Communication History: Save emails, letters, and summaries of important phone calls with beneficiaries and advisors.

Communicate Early and Often

Many trust disputes arise from simple misunderstandings. When you keep beneficiaries in the loop, you build trust and stop suspicion from growing into a lawsuit. Send regular, easy-to-understand updates on the trust's performance, expenses, and distribution timelines.

An ounce of proactive communication is worth a pound of legal defense. By answering questions and addressing concerns head-on, you can put out small fires before they become a wildfire.

Get a Trustee Bond or Insurance

A trustee bond is like an insurance policy for the trust. It guarantees that if you cause a financial loss through an honest mistake or misconduct, the bond will cover the damages up to a set amount. Many trusts require one, but even if yours doesn't, it’s a smart investment for your peace of mind. For another layer of protection, you can look into errors and omissions (E&O) insurance, which specifically covers you against claims of negligence.

Know When to Call in the Professionals

The smartest move any trustee can make is knowing their own limits. You're not expected to be a legal eagle, financial wizard, and tax guru all at once. Bringing in professionals isn't a sign of weakness; it's the mark of a prudent trustee.

- Consult a Texas trust administration lawyer for legal guidance, especially when interpreting the trust or navigating a dispute.

- Hire a CPA who specializes in fiduciary accounting and tax preparation.

- Work with a financial advisor to ensure the trust's investments are managed according to the prudent investor rule.

Getting professional support from firms that live and breathe probate and estate planning is the best risk-management strategy there is. It's how you ensure you're protecting not just the trust, but also yourself.

Your Trustee Liability Questions, Answered

Stepping into the role of a trustee can feel like navigating a legal minefield. It’s natural to have questions. Here are straightforward answers to the most common concerns we hear from trustees in Texas.

Can I be held liable for a co-trustee’s mistake in Texas?

Yes, absolutely. It’s a common misconception that you're only responsible for your own actions. Under the Texas Trust Code, if you stand by while a co-trustee makes a mistake, you could be held personally liable right alongside them. This can happen if you participate in their error, improperly delegate authority, or simply approve of their wrongful act. You have a duty to use reasonable care to prevent a co-trustee from committing a breach, which is why clear communication and defined roles are so critical.

How long does a beneficiary have to sue a trustee in Texas?

Generally, a beneficiary has four years to bring a lawsuit for a breach of fiduciary duty. However, Texas follows the "discovery rule," which means the four-year clock may not start until the beneficiary either knew or reasonably should have known about the breach. This can extend the timeline considerably, which is why transparent record-keeping and proactive communication with beneficiaries are your best defense.

Does an exculpatory clause in the trust shield me from all liability?

No, it does not. While many trusts include an "exculpatory clause" designed to protect a trustee from honest mistakes, Texas law draws a firm line.

An exculpatory clause is legally void if it attempts to protect a trustee from a breach of trust committed in bad faith, with intentional disregard for the trust’s purpose, or with reckless indifference to a beneficiary's interests.

Simply put, you cannot hide behind a clause if you have acted with gross negligence or engaged in willful misconduct. A Texas estate planning attorney can help you understand the specific protections and limitations within your trust document.

If you’re managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.