Planning for your family's financial future can feel overwhelming, especially when navigating complex legal tools. A credit shelter trust is one of those instruments that may sound like dense legal jargon but is actually a powerful way to protect your legacy. You might also hear it called a bypass trust or an A/B trust, but the goal is the same: ensuring the wealth you've worked so hard for goes to your loved ones, not to estate taxes.

Think of it like a financial "shelter." When the first spouse passes away, assets up to the federal estate tax exemption limit are moved into this trust. This strategic move shields those assets from being taxed when the surviving spouse eventually passes away. It's a savvy strategy that allows a married couple to effectively use both of their individual estate tax exemptions to the fullest, preserving more for the next generation.

Understanding the Credit Shelter Trust Under Texas Law

At its core, a credit shelter trust is about smart wealth preservation. Upon the death of the first spouse, the trust springs into existence as a separate, irrevocable legal entity, governed by the terms you set and the Texas Trust Code. Assets are then transferred into it, officially "using" the deceased spouse's lifetime estate tax exemption.

So, what does this mean for the surviving spouse? They are not left without support. They can still benefit from the assets in the trust, often receiving all the income it generates. They can also typically access the principal for important needs like healthcare, education, or general support. The crucial distinction is that they do not own the assets outright. This legal separation keeps the trust's value out of their estate for tax purposes down the road.

Key Features and Purpose for Texas Families

Setting up this kind of trust offers significant advantages that go beyond just minimizing taxes. An experienced Texas estate planning attorney can walk you through whether this approach fits your family's unique situation.

Here's a look at what a credit shelter trust brings to the table:

- Maximizing Tax Exemptions: This is the primary benefit. It allows a married couple to use both of their federal estate tax exemptions, potentially protecting millions from estate taxes.

- Sheltering Asset Growth: It's not just the initial amount that's protected. Any growth or appreciation of the assets inside the trust is also sheltered from future estate taxes. This can result in substantial savings over several years.

- Protecting Your Legacy: It ensures the assets ultimately land where the first spouse intended. This is incredibly valuable for blended families, guaranteeing children from a previous marriage receive their intended inheritance.

- Providing Asset Protection: Since the assets are held in an irrevocable trust, they are generally shielded from the surviving spouse's future creditors or legal troubles.

By creating this financial shelter, you're not just providing for your spouse; you're building a secure bridge for your inheritance to pass to your children or other heirs. It's a foundational piece in any robust asset protection and estate planning strategy.

Credit Shelter Trust at a Glance

For those who prefer a quick summary, here’s the essential information about what a Credit Shelter (or Bypass) Trust does.

| Feature | Description |

|---|---|

| Primary Goal | Minimize or eliminate federal estate taxes for married couples. |

| How It Works | Upon the first spouse's death, assets up to the exemption limit are placed in an irrevocable trust. |

| Benefit for Survivor | The surviving spouse can receive income and access principal for specific needs (like health and education). |

| Tax Advantage | The trust's assets (and their growth) are excluded from the surviving spouse's taxable estate. |

| Legacy Protection | Ensures assets ultimately pass to beneficiaries designated by the first spouse to die. |

| Common Names | Also known as a Bypass Trust, AB Trust, or Family Trust. |

This structure is a time-tested method for preserving wealth across generations, especially for families with significant assets.

How a Credit Shelter Trust Works: A Step-by-Step Guide

On the surface, a "credit shelter trust" sounds like something cooked up in a high-rise accounting firm. But in reality, it's a straightforward and powerful tool that comes to life within a couple's estate plan right after one spouse passes away. Let's walk through a real-world scenario to see how it protects your family's legacy.

Imagine a Texas couple, Sarah and Tom. Over the years, they've built a comfortable life and a sizable estate. They worked with a Texas estate planning attorney to include a credit shelter trust in their plan. Their main goal? To ensure their assets—from their family home in The Woodlands to their investment portfolio—get to their children with as little interference from estate taxes as possible.

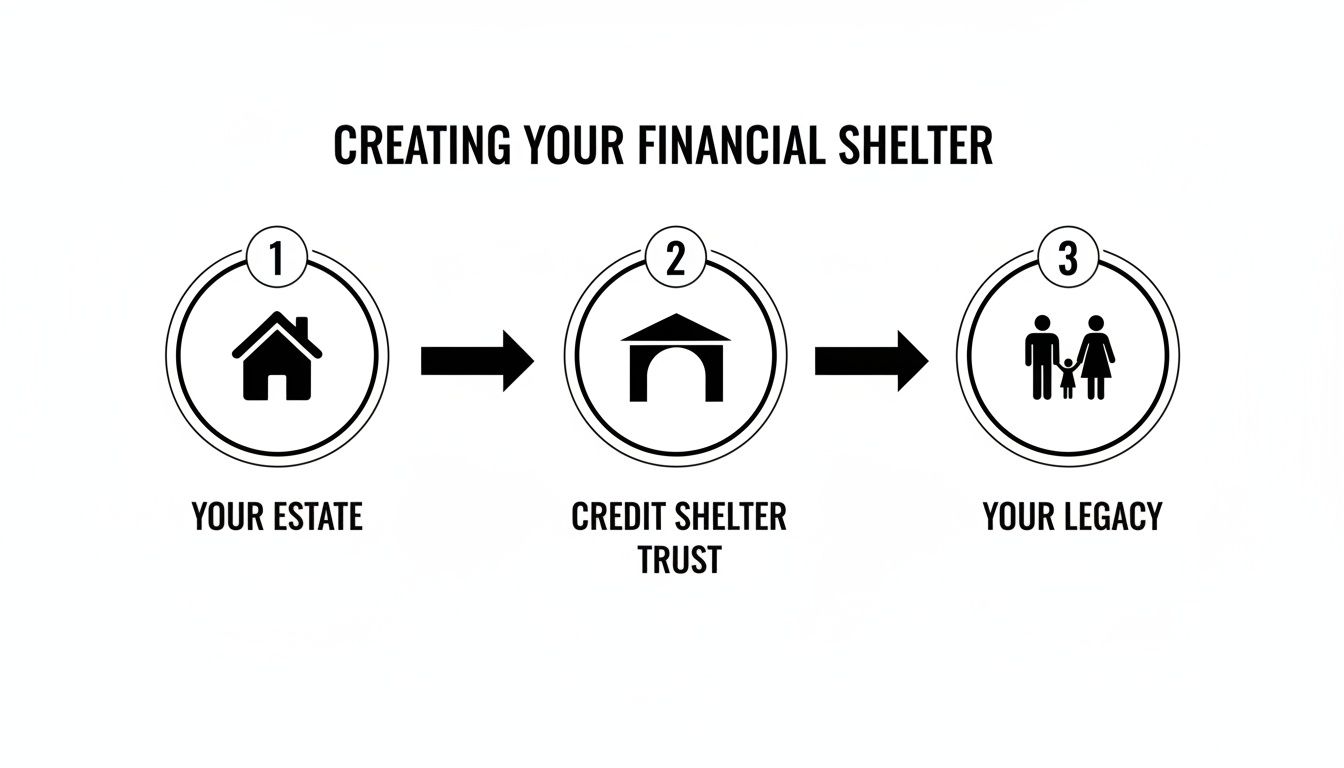

The basic idea is to create a protective container for a portion of your estate, preserving it for the next generation. This diagram shows the general flow:

Think of it as setting aside a portion of the family wealth in a secure vault that benefits the surviving spouse but ultimately belongs to the children.

Step 1: Creation and Initial Planning

First, Sarah and Tom sit down with their attorney to create an estate plan that specifically includes the language for a credit shelter trust. This document is the blueprint. It spells out all the critical details: who the beneficiaries are (their children), who will serve as trustee (often the surviving spouse), and the rules for managing and distributing the trust's assets.

Step 2: The First Spouse Passes Away

Years down the road, Tom passes away. This is the moment the credit shelter trust officially springs into existence and becomes irrevocable—its terms are now locked in. The process of funding the trust can now begin.

Here's where the tax strategy shines. For 2024, the federal estate tax exemption is a substantial $13.61 million per person. When Tom dies, an amount up to this exemption limit is carved out from his share of the estate and moved into the trust. This move officially "uses" Tom's exemption, shielding those assets (and all their future growth!) from being counted in Sarah's taxable estate later on. It’s the key to letting a couple shield up to $27.22 million combined from the steep 40% federal estate tax.

Step 3: Funding the Trust and Managing Assets

The executor of Tom's estate, following the rules in the trust document and the Texas Estates Code, will transfer specific assets into the trust. It's often a smart move to fund it with assets that are likely to appreciate, like stocks or real estate, because all that future growth is also sheltered from estate tax.

Sarah, as the surviving spouse and trustee, takes the reins. She now has fiduciary duties under Texas law to manage these assets in the best interests of the trust's beneficiaries—their children. This means she must invest prudently, handle tax filings, and keep meticulous records.

Key Takeaway: Sarah doesn't "own" the assets in the credit shelter trust. She's the manager, the steward. This legal separation is precisely what gives the trust its powerful tax protection.

Step 4: The Surviving Spouse's Benefit

Now, just because the assets are legally separate doesn't mean Sarah is left without support. The trust is designed to support her. She is entitled to all the income the trust generates, like stock dividends or rent from a property.

On top of that, the trust document usually allows her to tap into the principal for certain defined needs, often referred to by the acronym "HEMS"—Health, Education, Maintenance, and Support. This gives her financial flexibility while keeping the trust's tax-sheltered status intact.

Step 5: Final Distribution to Heirs

When Sarah eventually passes away, her own estate is valued and taxed using her own separate estate tax exemption. But the assets inside the credit shelter trust? They aren't part of her estate at all. They completely bypass her estate, avoiding probate and another round of estate taxes. The assets pass directly to their children, exactly as Tom had planned years before.

This step-by-step process is a cornerstone of smart estate planning. It ensures a couple can make full use of both of their tax exemptions, preserving millions in family wealth that might have otherwise gone to the IRS.

Credit Shelter Trust vs Portability Explained for Texas Couples

When Texas couples sit down to plan their estate, the conversation often turns to one big question: how do we handle the federal estate tax? Two paths usually emerge: setting up a credit shelter trust or simply relying on portability. On the surface, portability sounds like the easy route. But that simplicity can come with a multi-million-dollar price tag for your family down the road.

Portability lets a surviving spouse use their deceased spouse’s leftover federal estate tax exemption. It’s a straightforward concept, but it has a massive blind spot. It does absolutely nothing to protect the future growth of those inherited assets from being taxed. This is exactly where the credit shelter trust shines.

Understanding the Key Difference: Asset Growth

The most important distinction between these two strategies boils down to how they handle the appreciation of assets after the first spouse passes away. This is a game-changer.

With a Credit Shelter Trust: Assets up to the federal exemption limit are placed into an irrevocable trust. From that point on, all the growth, dividends, and appreciation on those assets happen inside the trust, totally shielded from any future estate taxes.

With Portability: The surviving spouse inherits everything directly. Sure, they also get to "port" the deceased's unused tax exemption, but here’s the catch: every penny of growth on those inherited assets now becomes part of the surviving spouse's own taxable estate.

When you consider the power of compounding over ten, fifteen, or even twenty years, the difference isn't just significant—it can be staggering. The money in a credit shelter trust can multiply without ever increasing the surviving spouse’s tax burden. With portability, every dollar of growth is another dollar that could be subject to estate tax later.

A Tale of Two Strategies: A Practical Example

Let's bring this to life with a real Texas scenario. Meet David and Emily, a Houston couple with a combined estate worth $20 million. David passes away when the federal estate tax exemption is $13 million.

Scenario 1: They Rely on Portability

Emily inherits David’s $10 million share outright, bringing her total estate to $20 million. She files the right paperwork to "port" David's unused $13 million exemption and adds it to her own. Over the next 15 years, her assets grow from $20 million to $30 million. When she passes, her total exemption is $26 million (David's $13M + her own $13M). Her estate is now taxed on the $4 million that spills over this limit, triggering a significant tax bill.

Scenario 2: They Use a Credit Shelter Trust

When David dies, $10 million of his assets are transferred into a credit shelter trust. Emily is the beneficiary, so she can receive income and, depending on the terms, principal from the trust. Over the next 15 years, the assets inside the trust grow to $15 million. Meanwhile, Emily’s personal $10 million grows to $15 million. When she passes away, the $15 million inside the credit shelter trust is completely excluded from her estate for tax purposes. Her taxable estate is just her personal $15 million, which is mostly covered by her own $13 million exemption. The tax liability is dramatically reduced, or perhaps even eliminated entirely.

The numbers don't lie. Credit shelter trusts are masters at shielding post-death asset growth. If you fund a trust with nearly $14 million and see an average annual return of 7-8%, it could easily swell to $20 million in a decade. That $6 million in pure growth is completely sheltered from the 40% federal estate tax. That’s a savings of up to $2.4 million compared to portability, where every cent of that growth would remain exposed.

To see how these two powerful tools stack up, let's compare them side-by-side.

Comparing Credit Shelter Trust vs. Estate Tax Portability

| Feature | Credit Shelter Trust | Portability |

|---|---|---|

| Asset Growth | All future appreciation is sheltered from estate tax. | All future growth on inherited assets is part of the surviving spouse's taxable estate. |

| Control | The first spouse to die determines the ultimate beneficiaries (e.g., children). | The surviving spouse has total control and can change beneficiaries or disinherit children. |

| Asset Protection | Assets are protected from the surviving spouse's creditors, lawsuits, or a future divorce. | Assets are vulnerable to creditors, lawsuits, and claims from a subsequent spouse. |

| Generation-Skipping | Can be structured to include grandchildren, maximizing tax savings across generations. | Does not offer any generation-skipping tax benefits. |

| State Estate Tax | Can provide protection against state-level estate taxes, if applicable. | Offers no protection against state estate taxes. |

| Remarriage Risk | The deceased spouse's exemption is locked in and protected. | The deceased spouse's exemption can be lost if the survivor remarries and their new spouse dies first. |

This table clearly shows that while portability might seem like the simpler option, a credit shelter trust offers far more robust protection and control for your legacy.

Why Portability Can Fall Short

Simplicity isn't always best, especially in estate planning. A skilled Texas estate planning attorney will point out several risks that come with relying solely on portability.

- Loss of Exemption: The deceased spouse’s exemption isn't permanently yours. If the surviving spouse remarries and their new spouse also passes away, the first spouse's exemption is lost forever.

- No Asset Protection: Assets inherited through portability are wide open to attack from the surviving spouse’s creditors, lawsuits, or even a messy divorce down the line.

- No Control Over Legacy: The first spouse to pass away gives up all say in where their assets ultimately land. The surviving spouse could remarry and decide to leave everything to their new family, unintentionally disinheriting the children from the first marriage.

Ultimately, choosing between a credit shelter trust and portability is a critical decision with financial consequences that will ripple through generations. For Texas families with significant assets, a trust almost always delivers superior, long-term protection for what you've worked so hard to build. You can learn more about how portability and estate tax intersect in our detailed guide.

The Enduring Power of Credit Shelter Trusts in Today's Estate Planning

Tax laws have a habit of changing. But one thing that never changes is the desire to protect your family's financial future. Credit shelter trusts, long a staple for high-net-worth families, have proven remarkably adaptable and remain a powerful tool, especially with potential tax law changes on the horizon. Understanding their modern role is the first step to building an estate plan that can weather any legislative storm.

You might have heard them called AB trusts. Before the concept of "portability" came along, they were absolutely essential. While their role has shifted with the rise and fall of federal estate tax exemption amounts, their core mission—saving on taxes, protecting assets, and controlling your legacy—is as important as ever. For Texas families looking to lock in their wealth for the next generation, being proactive is key.

More Than Just a Tax Play: The "Other" Benefits

The main reason people historically set up a credit shelter trust was to reduce their federal estate tax bill. But to think that's all they do is to miss the bigger picture. These trusts offer critical protections that portability simply can't touch, making them an incredibly versatile tool for total family security.

In Texas and across the country, families are using these trusts for some very smart, non-tax reasons:

- Ironclad Creditor Protection: Once assets are in an irrevocable credit shelter trust, they're generally off-limits to the surviving spouse's future creditors, unexpected lawsuits, or even a bankruptcy. It's like creating a financial fortress for your family.

- Securing Your Legacy: This is a game-changer for blended families. A credit shelter trust ensures that assets will eventually go to the children from a previous marriage, just as the first spouse intended. It’s a straightforward way to prevent an unintentional disinheritance down the road.

- Managing Inherited Wealth: Not every beneficiary is ready to handle a large inheritance. The trust provides professional management, making sure the funds are preserved and used wisely, not squandered.

Why They're Still a Hot Topic in a Shifting Tax World

The estate planning field is never static; tax laws are always in flux. The high federal estate tax exemptions we have today might not be here tomorrow, which makes locking in today's benefits more critical than ever. No matter the strategy, a key piece of the puzzle is always determining the fair market value of the assets involved.

There’s a renewed focus on credit shelter trusts because those high exemptions could be coming to an end. The Tax Cuts and Jobs Act (TCJA) is set to expire at the end of 2025, which could cut current exemptions in half. This change could suddenly make these trusts a must-have for many families. It's a return to the pre-2010 era when these trusts were essential for automatically preserving a spouse's full exemption—a far more certain approach than modern portability, which requires filing a timely estate tax return with the IRS.

Think of a credit shelter trust as a permanent safeguard. It locks in the deceased spouse's exemption at today's generous levels, shielding the family from any future laws that might shrink the amount of wealth they can pass on tax-free.

This kind of forward-thinking is precisely why so many families partner with a Texas estate planning attorney. They want to build a plan with both flexibility and certainty. A credit shelter trust delivers that certainty, ensuring your legacy is protected and your wishes are followed, no matter what happens in Washington, D.C.

Trustee Responsibilities Under Texas Law

Managing a loved one’s trust can feel overwhelming—but with the right legal guidance, it doesn’t have to be. Setting up a credit shelter trust is a fantastic first step, but the real work begins once it's in action. When the first spouse passes away, the trust becomes irrevocable, and from that moment on, the roles of the trustee and the beneficiaries are absolutely critical.

Understanding what's expected of everyone involved, as laid out by the Texas Trust Code, is the key to making sure the trust runs smoothly and achieves its intended purpose. The trustee, who is often the surviving spouse or a professional, takes on a role of immense responsibility. This isn't just about managing money; it's about honoring the final wishes of the person who passed and always acting in the best interests of the beneficiaries.

The Trustee’s Core Fiduciary Duties

Under Texas law, a trustee is held to a very high standard known as a fiduciary duty. This is a legal and ethical promise to act with complete loyalty, good judgment, and fairness. Failing to meet these duties can lead to personal liability and, unfortunately, deep family rifts. A Texas trust administration lawyer can provide essential guidance on these responsibilities.

Here are the key jobs on a trustee's plate:

- Prudent Asset Management: The trustee must invest and manage the trust’s assets as a "prudent investor" would. This means striking a careful balance between risk and return to preserve the principal while generating income. It’s a job that often requires collaboration with financial advisors.

- Loyalty to Beneficiaries: A trustee's number one loyalty is to the beneficiaries. They must avoid any self-dealing or conflicts of interest where they might benefit at the expense of the people the trust was meant to protect. These are core fiduciary duties in Texas.

- Detailed Record-Keeping and Accounting: Keeping meticulous records is non-negotiable. Every transaction, distribution, and expense must be documented. The trustee is also required to provide regular accountings to the beneficiaries so everyone stays informed.

- Tax Compliance: The trustee is responsible for filing the trust's annual income tax returns (Form 1041) and making sure all tax obligations are handled correctly and on time.

- Communication: A good trustee keeps the beneficiaries reasonably informed. This includes sharing important information about how the trust is being managed and any material facts they need to know to protect their interests.

The specific trustee responsibilities after death can be complex, and knowing them is crucial for anyone stepping into this role.

Understanding Beneficiary Rights in Texas

While trustees have duties, beneficiaries have rights. In a typical credit shelter trust, the surviving spouse is the primary income beneficiary, with the children or other heirs as the "remainder" beneficiaries who will receive the assets after the surviving spouse passes away.

Beneficiaries generally have the right to:

- Receive timely distributions as spelled out in the trust document.

- Be kept informed about the trust and how it’s being administered.

- Request an accounting to get a clear view of how the assets are being handled.

- Hold the trustee accountable if they fail to uphold their fiduciary duties.

A very common setup in a credit shelter trust gives the surviving spouse all the income the trust generates. They might also be able to access the principal for certain needs, often defined by a standard known as Health, Education, Maintenance, and Support (HEMS). This provides helpful flexibility while keeping the trust's tax advantages intact.

Successfully navigating these roles requires a solid grasp of both Texas law and the specific terms of the trust document. Whether you’re a trustee seeking direction or a beneficiary trying to understand your rights, working with a Texas trust administration lawyer is the best way to prevent misunderstandings and ensure the trust is managed exactly as intended. You can learn more about these specific legal obligations in our deep dive into trustee duties and responsibilities in Texas.

Setting Up Your Credit Shelter Trust in Texas

Deciding to set up a credit shelter trust is a proactive step toward protecting your family’s financial future. While it may seem complex, with an experienced attorney to guide you, it is a clear and manageable process. Think of it as building a financial fortress for your legacy, brick by legal brick, in full compliance with Texas law.

The first step isn't signing documents; it's a conversation. A thorough discussion with a Texas estate planning attorney is where it all begins. This is how you'll determine if this powerful tool is genuinely the right fit for your family's circumstances.

A Step-by-Step Guide for Texas Families

Putting a credit shelter trust in place involves a series of deliberate moves, all designed to ensure your wishes are legally sound and your assets are shielded. Here’s a breakdown of what that journey typically looks like:

- Initial Consultation and Strategy: This is where you’ll lay out your family dynamics, your financial picture, and your long-term goals. Your attorney will analyze everything to determine if a credit shelter trust is the best way to minimize potential estate taxes and achieve your legacy objectives.

- Drafting the Trust Document: Next, your attorney will craft the legal document that serves as the trust’s rulebook. This is where you'll name beneficiaries, appoint a trustee (and successors), and spell out exactly how the surviving spouse can access the trust's funds.

- Selecting Your Trustee: Choosing the right trustee is a critical decision. This person or institution will be in charge of managing the trust's assets, and they have a legal obligation to follow your instructions and uphold their fiduciary duties in Texas.

- Funding the Trust: While the trust is typically funded after the first spouse passes away, your estate plan needs to specify which assets will be used. This often means coordinating asset titles and beneficiary designations to align with the trust's design.

Crucial Insight: A credit shelter trust isn't an off-the-shelf product. To be effective, it must be custom-built for your life—whether that means navigating a blended family, handling unique assets like a family business, or planning for future growth.

Why You Shouldn't Go It Alone

Attempting to create a trust without professional guidance can lead to costly mistakes, family disputes, and unforeseen tax consequences. An experienced attorney ensures every detail is handled correctly. If you're wondering about foundational steps, questions like "how to modify a trust in Texas" highlight the complexities where professional advice is essential.

Working with an experienced firm provides more than just a legal document. It's an investment in peace of mind, ensuring your trust is compliant with the Texas Trust Code, built for maximum tax efficiency, and is a true reflection of what you want for your loved ones.

Got Questions About Credit Shelter Trusts? We've Got Answers.

Jumping into the world of estate planning can feel like learning a new language. It's only natural to have questions. To help you feel more confident, we've gathered some of the most common questions we hear about credit shelter trusts in Texas.

Can My Spouse Be the Trustee?

Absolutely. In Texas, it's quite common for the surviving spouse to serve as trustee for the credit shelter trust. This setup puts them in control of managing the assets and handling distributions.

However, there’s a crucial rule: the spouse's power to distribute trust principal to themselves must be limited by what's called an "ascertainable standard." This legal term means the funds should only be for their Health, Education, Maintenance, and Support—or HEMS. Adhering to this HEMS standard is non-negotiable; it's what prevents the IRS from including the trust's assets in the surviving spouse's estate later on.

What Kind of Assets Should Go into the Trust?

Deciding what to put in the trust is a strategic move that can dramatically boost its long-term value.

You want to think about growth potential. The best assets for a credit shelter trust are the ones you expect to appreciate over time. This includes:

- Stocks and investment portfolios

- Real estate that’s likely to increase in value

- Interests in a family business

By funding the trust with these high-growth assets, you're maximizing its tax-saving power. Every dollar of growth that occurs inside the trust is shielded from future federal estate taxes, preserving more wealth for your heirs.

Can We Change the Trust After It's Set Up?

Once the first spouse passes away, a credit shelter trust becomes irrevocable. This means its terms are set in stone and cannot be changed or canceled.

This permanence is a key feature, not a flaw. It serves two important purposes:

- It acts as a shield, protecting the assets from the surviving spouse's future creditors or legal troubles.

- It guarantees the assets eventually go to the beneficiaries designated by the first spouse. This is especially important for blended families, ensuring children from a previous marriage receive their intended inheritance.

Is This Trust Only for the Very Wealthy?

While the primary benefit is avoiding the federal estate tax—which currently applies to very large estates—this trust offers valuable perks even for families with more modest wealth.

For one, it provides excellent creditor protection and gives you certainty that your assets will end up with the right people. Furthermore, tax laws are always changing. The federal estate tax exemption could be much lower in the future. Establishing a trust now can act as an insurance policy against future tax law changes, protecting your family from an unexpected tax burden.

If you’re managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.