Planning for your family's financial security can feel overwhelming, but with the right legal guidance, it doesn’t have to be. One of the most effective tools in estate planning is a special legal vehicle known as an Irrevocable Life Insurance Trust (ILIT).

Think of it as a dedicated, high-security vault you create specifically to own your life insurance policy. When the time comes, the payout goes into this vault instead of directly into your estate. This simple step keeps it safe from creditors, out of the public probate process, and ensures it’s used exactly how you intended, all while potentially saving your family a significant amount in estate taxes.

Understanding the Life Insurance Trust in Texas

So, what is a life insurance trust, really? It is a special legal arrangement you create to own and manage your life insurance policy. Instead of the death benefit being paid to an individual or getting lumped into your estate, it flows directly into this trust, managed by a person you choose.

This one move is a game-changer for many Texas families. It keeps the policy proceeds out of the lengthy and often public probate process and, crucially, can shield the entire amount from hefty federal estate taxes.

This structure gives you an incredible amount of control over how your legacy is handled. The trust acts as a responsible guardian for the policy proceeds, giving you peace of mind that your family will get the full benefit you planned for, without unnecessary delays or tax hits.

To see just how much of a difference this can make, let's compare the two scenarios side-by-side.

Life Insurance Payout With vs. Without a Trust

| Feature | Payout Directly to Beneficiary | Payout Through a Life Insurance Trust |

|---|---|---|

| Estate Tax Inclusion | Included in your taxable estate. | Not included in your taxable estate. |

| Probate Process | Bypasses probate, but the cash is vulnerable. | Bypasses probate and proceeds are protected by the trust. |

| Creditor Protection | Funds are exposed to the beneficiary's creditors. | Funds are protected from both your and the beneficiary's creditors. |

| Control Over Funds | Beneficiary receives a lump sum with no restrictions. | Funds are managed and distributed by the trustee based on your rules. |

| Minor Beneficiaries | Court appoints a guardian to manage the funds. | Trustee manages funds for the minor's benefit until they reach the age you specify. |

As you can see, using a trust offers layers of control and protection that simply aren't available when a policy pays out directly. It’s about more than just avoiding taxes; it’s about responsible stewardship of your assets for the people you care about most.

The Key Players in an ILIT

To understand how an ILIT works, you need to know who's involved. It’s a bit like a play with a few key roles:

- The Grantor: That’s you. You're the one who creates the trust and funds it, either by transferring an existing life insurance policy or giving the trust money to buy a new one.

- The Trustee: This is the person or institution you pick to manage the trust. Under the Texas Trust Code, the trustee has a legal (fiduciary) duty to follow your instructions, make sure the policy premiums are paid, and eventually distribute the money to your beneficiaries.

- The Beneficiaries: These are the people you want to benefit from the policy—your spouse, children, or grandchildren. They will receive the funds from the trust according to the specific rules you laid out.

It's important to know that an ILIT is, by definition, irrevocable. That means once you set it up, you cannot simply change your mind or tear it up. This permanence is exactly what gives it such powerful tax and asset protection benefits. A knowledgeable Texas estate planning attorney can help you integrate an ILIT into a resilient plan that protects your family and preserves your wealth for generations.

The Real-World Benefits of a Texas Life Insurance Trust

Setting up a trust for your life insurance might seem like an extra step, but the advantages it delivers are powerful and built to last. For many Texas families, an Irrevocable Life Insurance Trust (ILIT) is more than a legal document—it's a smart strategy for protecting their legacy.

The benefits boil down to three key areas: serious tax savings, solid asset protection, and having the final say on how your money is used. This isn't just about a simple payout; it's about making sure the assets you've worked so hard for reach your loved ones intact and are used in a way that aligns with your wishes.

Lowering or Eliminating Estate Taxes

One of the biggest reasons people turn to an ILIT is its incredible ability to slash or even eliminate federal estate taxes. It’s a common misconception, but when you personally own a life insurance policy, the death benefit is counted as part of your gross estate.

If your total estate’s value exceeds the federal exemption limit (which is generous now but can and does change), anything above that threshold could be taxed as high as 40%.

By moving ownership of the policy into an ILIT, the proceeds are no longer legally yours. That means the full death benefit can pass to your beneficiaries without being touched by federal estate tax. For families with significant assets, this single move can mean saving hundreds of thousands, or even millions, of dollars. The ILIT acts as its own financial entity, shielding the policy from the IRS and keeping more of your wealth with your family. To get a better feel for this, you can dig deeper into the various irrevocable trust tax benefits available under today's laws.

Ironclad Asset Protection for Your Beneficiaries

Beyond the tax perks, an ILIT acts like a fortress against creditors and lawsuits—for both you and the people you leave the money to. Once the trust owns that policy, the proceeds are generally off-limits to your personal creditors.

That protection extends to your beneficiaries, too. For example, if your adult child receives a large lump-sum payout directly, that cash is suddenly exposed to their potential problems—a business deal gone wrong, a future divorce, or a lawsuit. But when the funds are held safely inside the trust, they are insulated from those threats.

A well-drafted Texas trust can include what’s known as a "spendthrift" provision. This clever clause, recognized under the Texas Trust Code, stops beneficiaries from signing away their interest to creditors and prevents creditors from coming after trust assets to pay off a beneficiary's debts.

This is a critical layer of security that makes sure the inheritance you leave behind is actually used for what you intended: taking care of your loved ones. This is a core component of effective asset protection.

Maintaining Control Over Your Legacy

Perhaps the most personal benefit is the sheer control an ILIT gives you over your legacy. Instead of a beneficiary getting a massive, unrestricted check all at once—which can be overwhelming and sometimes unwise—you get to lay down the rules for how and when the money is paid out.

This feature is a game-changer in so many real-world scenarios. For instance, you could:

- Stagger distributions for a young adult, releasing funds for college tuition, then for a down payment on a home, and finally the rest when they're a bit older and wiser.

- Create a lifelong income stream for your spouse, ensuring they are always financially secure without being burdened by managing a large sum of money.

- Provide for a loved one with special needs without accidentally disqualifying them from crucial government benefits.

For families with young children, a life insurance trust is especially powerful. It expertly manages the money for your kids, sidestepping the legal headaches of naming minors as direct beneficiaries. To understand why a trust is often the best solution, you can learn more about the complexities of Can Minors Be Life Insurance Beneficiaries?. An experienced attorney can help you tailor these provisions to fit your family’s unique story perfectly.

Step-by-Step Guidance: Creating and Funding Your Life Insurance Trust

The idea of setting up a legal structure like an Irrevocable Life Insurance Trust (ILIT) can sound intimidating, but it is a logical, step-by-step process. With the right legal guidance, creating this powerful tool for your family’s future is more straightforward than you might think.

Think of it as building a secure house for your life insurance policy, one brick at a time. This roadmap will walk you through the process, from laying the foundation with a Texas estate planning attorney to keeping the policy funded.

Step 1: Draft the Trust Document

First, you’ll need to work with a qualified attorney to draft the trust agreement. This is the legal blueprint for your ILIT, the document where you lay out all the rules. It’s your voice, making sure your wishes are followed to the letter long after you're gone.

Inside this document, you'll specify the essentials:

- Name your beneficiaries: Get specific about who will receive the trust assets.

- Define distribution terms: Lay out exactly how and when the funds should be paid out. You might want payments staggered for a young adult or set up care for a spouse's lifetime.

- Appoint a trustee: Choose the person or institution who will be in charge of managing the trust.

This document must be carefully drafted to comply with both the Texas Trust Code and IRS regulations. Getting this right is what secures all the tax and asset protection benefits you're after, so professional legal help is non-negotiable.

Step 2: Select and Appoint a Trustee

Your trustee is the manager of the operation. This person or institution has fiduciary duties in Texas, meaning they are legally bound to act in the best interests of your beneficiaries and follow your instructions. A crucial point: you cannot be the trustee of your own ILIT. Doing so would pull the policy right back into your taxable estate, defeating a major purpose of the trust.

You need to pick someone who is responsible, organized, and absolutely trustworthy. People often choose a responsible family member, a close friend, or a corporate trustee like a bank’s trust department. Their job is a big one—they’ll handle everything from paying the policy premiums to eventually filing the death claim and managing the money for your loved ones.

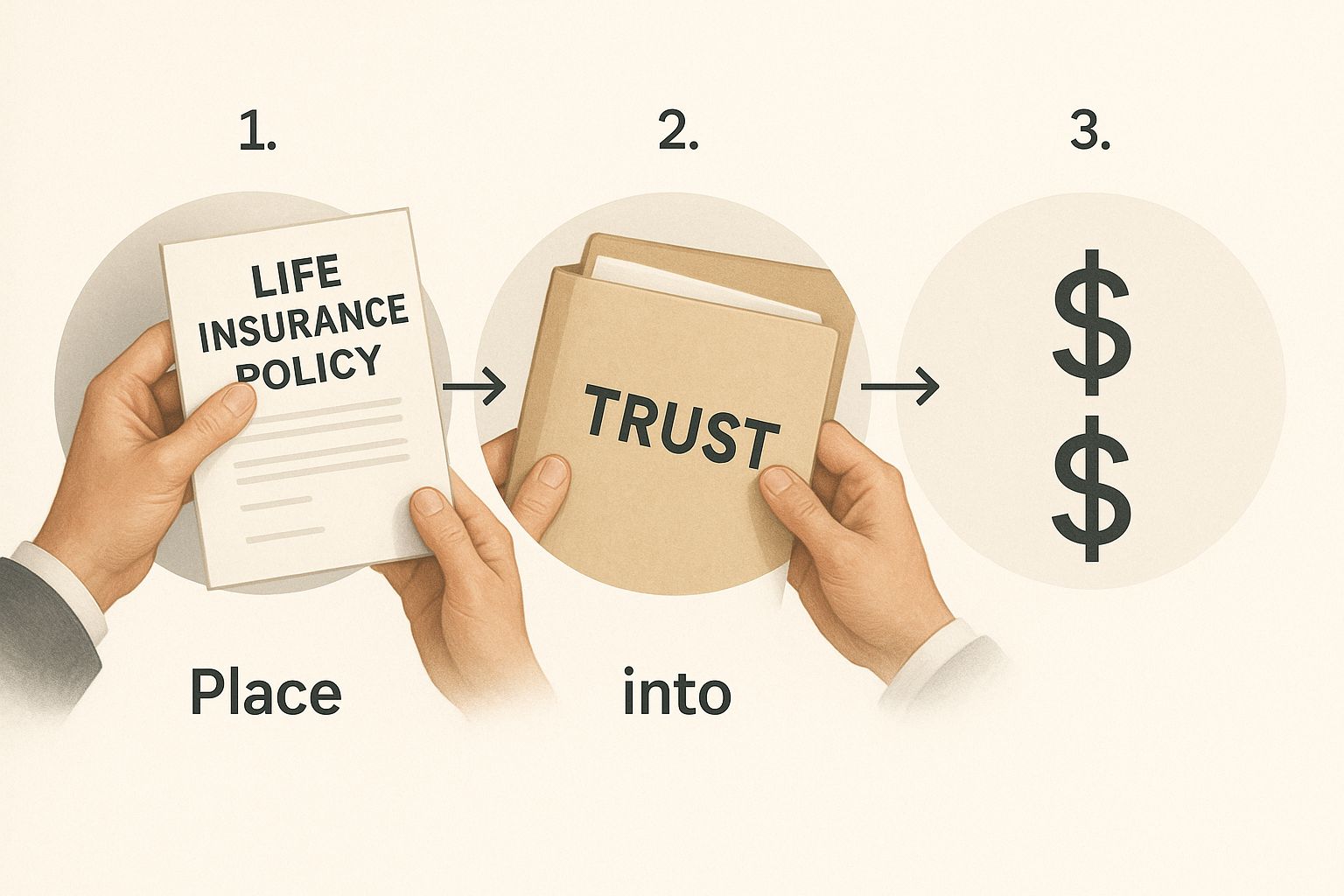

Step 3: Fund the Trust

Once the trust is created, it's time to place the life insurance policy inside it. You have two main ways to do this:

- Transfer an Existing Policy: If you already have a policy, you can sign ownership over to the trust. Just be mindful of the IRS’s three-year look-back rule. If you pass away within three years of making that transfer, the IRS can pull the proceeds right back into your taxable estate.

- The Trust Purchases a New Policy: This is the cleaner, and usually preferred, method. You gift money to the trust, and then the trustee uses those funds to apply for and buy a brand-new policy. This route completely sidesteps that tricky three-year look-back rule.

The infographic below shows this simple but vital step of putting the policy under the trust's ownership—the key move that unlocks all its benefits.

This visual captures that critical moment when the policy legally belongs to the trust, not to you. That's what gives it protected status.

Step 4: Handle Annual Premiums with Gifting and Crummey Letters

An ILIT is a legal shell; it doesn't earn its own money. To pay the annual insurance premiums, you (the grantor) will need to make annual gifts to the trust. To ensure these gifts fall under the annual gift tax exclusion (currently $18,000 per beneficiary per year for 2024), there's a specific legal process to follow.

Every time you put money into the trust for the premium, the trustee must send a special notice to each beneficiary. This is called a “Crummey letter,” and it gives them a short window of time to withdraw their share of the gift.

In reality, beneficiaries understand the money is meant for the premium, so they almost never withdraw it, and the trustee can pay the bill as planned. But sending these formal letters—and documenting it—is a critical yearly step to keep the trust's tax benefits intact. A Texas trust administration lawyer can make sure this routine is handled perfectly every single time.

Trustee Responsibilities Under Texas Law: Choosing the Right Manager

Setting up a life insurance trust is a brilliant move for your family's future, but that plan is only as solid as the person you pick to manage it. This person, the trustee, is the legal guardian of your trust. They will carry out your wishes and make the tough calls. Choosing your trustee is one of the most critical decisions in your entire estate plan.

So, who can you count on to handle this with responsibility and care? It’s a big question. You need to weigh the pros and cons of asking a family member versus hiring a professional corporate trustee. Getting this right means your trust will run smoothly and your family will be protected exactly as you intended.

Key Qualities of an Effective Trustee

No matter who you have in mind, a good trustee needs a specific set of skills. They are held to strict legal standards under the Texas Trust Code, and their performance directly affects your beneficiaries' financial security.

Here are the must-haves:

- Financial Savvy: Your trustee will manage a potentially large sum of money. They need to be comfortable with financial concepts, whether overseeing investments or calculating distributions.

- Impartiality: Family dynamics can be complicated. A great trustee can navigate any potential drama with fairness, always sticking to the rules you laid out in the trust.

- Longevity and Stability: This trust could exist for decades. Your trustee should be someone—or an institution—that you can count on to be there for the long haul.

- Understanding of Fiduciary Duties: This is non-negotiable. A trustee has a legal obligation, a fiduciary duty, to act only in the best interests of the beneficiaries. You can get a deeper look at these legal responsibilities in our guide on the duties and responsibilities of a trustee in Texas.

Family Member vs. Corporate Trustee: A Comparison

Many people first think of naming a trusted relative. That can work, but it’s smart to look at the whole picture.

Family Member as Trustee:

- Pros: They know your family personally, probably won't charge a fee, and understand your values.

- Cons: They might not have the financial expertise, could get pulled into family disagreements, and the responsibility can become a huge burden.

Corporate Trustee (like a bank's trust department):

- Pros: You get professional expertise, guaranteed impartiality, and long-term stability with regulatory oversight.

- Cons: They charge fees for their services and won’t have a personal connection to your family.

The right choice depends on your family’s unique situation. A Texas estate planning attorney can help you sort through these factors and pick a trustee who’s a perfect fit for your goals.

Trustee Responsibilities for an ILIT

A trustee's job starts before the life insurance policy ever pays out. Once you're gone, their role kicks into high gear.

Here’s what they’ll be handling:

- Collecting the Death Benefit: The trustee files the claim with the insurance company to get the proceeds.

- Managing and Investing Assets: Following Texas law, they must prudently invest the funds to protect their value.

- Distributing Funds: The trustee pays out money to the beneficiaries based on the exact instructions in the trust document.

- Tax and Administrative Duties: They’re also responsible for filing any necessary tax returns for the trust and keeping meticulous records of everything.

Navigating Texas Law to Ensure Your Trust is Secure

While an Irrevocable Life Insurance Trust (ILIT) gets attention for its federal tax perks, its day-to-day operation is governed by state law. For Texans, that means you must understand how our local rules can make or break your trust. Getting these details right is the difference between leaving a secure legacy and a plan that crumbles when your family needs it most.

From our unique community property rules to specific trustee duties, Texas law adds another layer to your ILIT strategy. This is your guide to avoiding common legal traps and building an estate plan that’s not just effective, but built for Texas.

The Texas Trust Code and Fiduciary Duties

The foundation for any trust in our state is the Texas Trust Code. This is the rulebook that lays out exactly what a trustee is responsible for. When you pick someone to manage your ILIT, they aren't just doing you a favor—they're taking on legally binding fiduciary duties in Texas.

Here’s what that really means:

- Duty of Loyalty: The trustee must act only in the best interests of the beneficiaries. No self-dealing or conflicts of interest are allowed.

- Duty of Prudence: They must manage the trust's assets—first the policy, then the payout—with the skill and care of a reasonable person.

- Duty to Account: Your trustee must keep meticulous records of every transaction and be ready to provide a full accounting to the beneficiaries if requested.

If a trustee fails in these duties, they can be held personally liable and spark ugly legal fights. That's why choosing a trustee who understands and respects these obligations is so critical.

Community Property: A Key Consideration for Married Texans

Texas is a community property state, which has a huge impact on how you fund an ILIT. If you use community funds—money earned by either spouse during the marriage—to pay life insurance premiums, the policy itself could be tagged as community property.

That’s a problem. To ensure the policy is treated as separate property and stays completely out of your taxable estate, you have to be deliberate. This usually involves a formal agreement between you and your spouse to "partition" the money used for premiums, legally making it the separate property of the insured spouse. You absolutely need a knowledgeable Texas estate planning attorney to get this done correctly.

Sidestepping Common Mistakes in Texas

Even the best-laid plans can be tripped up by simple mistakes. Two of the biggest pitfalls involve federal rules that are closely monitored.

Watch out for the IRS's three-year look-back rule. If you move an existing life insurance policy into your ILIT and then pass away within three years of that transfer, the IRS will pull the full death benefit right back into your taxable estate, defeating one of the main reasons for setting up the trust.

Another common error is messing up the annual gifting process. Every year, when you gift money to the trust for the premiums, the trustee must send out Crummey notices to the beneficiaries. These formal letters are what qualify your gifts for the annual gift tax exclusion. Skipping this step can put the trust’s tax-saving power at risk.

The life insurance world is constantly changing, especially with technology. This shift underscores the need for clear, personalized planning, which is what a well-built trust delivers. You can discover more insights on these industry changes on weforum.org to see how the industry is adapting. Properly managing your trust ensures your plan stays solid, no matter how things change.

Answering Your Top Questions About Texas Life Insurance Trusts

Planning for your family’s future is a big responsibility, and when you start exploring powerful tools like an Irrevocable Life Insurance Trust (ILIT), it’s natural to have questions. At The Law Office of Bryan Fagan, PLLC, we believe the best decisions are the ones you feel confident about.

This section provides clear, straightforward answers to the most common questions we hear from Texas families. Our goal is to remove the legal jargon and empower you with the knowledge needed to protect what you’ve built.

When to Modify or Terminate a Trust: Can I Change an "Irrevocable" Trust?

That word "irrevocable" sounds final for a reason. The point of an ILIT is that it’s permanent. As the grantor, you cannot wake up one day and decide to rewrite the rules. This permanence is what gives the trust its power for tax savings and asset protection.

But, life happens, and Texas law understands that. While you can't just change it on a whim, there are specific legal avenues for making adjustments when circumstances truly demand it.

- Court Modification: A trustee or beneficiary can ask a Texas court to modify the trust if a significant and unforeseen event has occurred since the trust was created.

- Beneficiary Agreement: Under the Texas Trust Code, if all beneficiaries agree, they can sign a binding agreement to change certain administrative parts of the trust without going to court.

- Trust Protector: Many modern trusts include a "trust protector." This is an independent person you name with specific, limited powers, like the ability to replace a trustee or update administrative terms.

Knowing how to modify a trust in Texas requires careful legal analysis. One wrong move could accidentally destroy the trust's tax benefits. This is a job for a seasoned Texas trust administration lawyer.

What Happens if the Life Insurance Premiums Don’t Get Paid?

An ILIT is essentially a special box designed to hold a life insurance policy. If the annual premiums stop being paid, the life insurance policy will lapse—it’s as simple as that.

When the policy lapses, the trust becomes an empty box. There are no assets left to give to your beneficiaries, defeating the entire purpose of setting it up. The system is designed for you, the grantor, to make consistent annual gifts to the trust, which the trustee then uses to pay the policy premiums.

It's critical to have a realistic plan for funding those premiums year after year. If your financial situation changes, the trustee might have options, like using the policy's cash value to cover premiums for a while, but this is often a temporary fix. This is a red-alert situation that calls for immediate advice from your legal and financial team.

Who Should I Choose to Be the Trustee?

Choosing a trustee is one of the most important decisions you'll make. This person or institution has a fiduciary duty to manage the trust exactly as you intended and in line with Texas law.

Here's the one rule you can't break: you, the grantor, cannot be the trustee. If you are, the IRS will say you still have "incidents of ownership" over the policy, and the death benefit gets pulled right back into your taxable estate, wiping out the main tax advantage.

So, who are the typical choices?

- A Trusted Family Member or Friend: They know you and your family, and probably won't charge a fee. The downside? They might lack financial expertise and could get caught in family drama.

- A Professional Corporate Trustee: A bank or a dedicated trust company brings impartiality, deep expertise, and stability. They live and breathe the fiduciary duties in Texas but charge for their services.

There's no single right answer. It depends on your family, your finances, and who you trust to carry out your wishes. A Texas estate planning attorney can help you talk through the pros and cons to find the perfect fit.

Do I Still Need an ILIT if My Estate Is Under the Tax Exemption Limit?

That's a fantastic question. While ILITs are famous for helping families sidestep federal estate taxes, their usefulness goes far beyond that. Even if your net worth is comfortably below the current federal exemption, an ILIT can still be a game-changer.

For one thing, tax laws are not permanent. The federal estate tax exemption has changed dramatically over the years. What seems safe today could be different in the future. An ILIT acts as a permanent shield, protecting your legacy from whatever changes Congress might make down the road.

Even more importantly, an ILIT offers powerful benefits that have nothing to do with taxes, especially asset protection.

An ILIT creates a protective bubble around the inheritance. It shields the money from your beneficiaries' potential future problems—like creditors, a lawsuit, or even a divorce. By putting the funds into a trust with a spendthrift clause, you ensure the money is there for their well-being, not to pay off someone else's claim.

On top of that, the trust gives you total control over how the money is paid out. This is a lifesaver for beneficiaries who might be young, have special needs, or are not ready to handle a large sum of money responsibly. You can design the trust to pay for college, help with a down payment on a house, or provide a steady stream of income for life.

If you’re managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process. Visit us at https://texastrustadministration.com to learn more.