Starting a business with partners is an exhilarating journey, built on a shared vision and mutual trust. But planning for the future can feel overwhelming, especially when considering life's unexpected turns. What happens if a co-owner suddenly passes away, becomes disabled, or goes through a divorce? This is where a buy sell agreement template becomes essential—think of it as a 'business prenup.' It’s a foundational document that provides a clear, legally binding roadmap for handling ownership transitions, ensuring your business and your family are protected.

Why Your Texas Business Needs a Buy Sell Agreement Now

For any business owner in Texas, operating without a clear plan for ownership transitions is a significant risk. With the right legal guidance, however, creating this plan doesn't have to be overwhelming.

Consider this common scenario: one of your partners dies unexpectedly. Under Texas law, their ownership stake could pass to a spouse or child who knows nothing about the business—or worse, has no interest in its success. This situation can quickly lead to operational gridlock, bitter family disputes, and crippling financial uncertainty for the remaining partners.

A well-crafted buy-sell agreement, grounded in Texas law, prevents this chaos by establishing the rules while everyone is on good terms. It is a non-negotiable part of responsible business ownership and a critical tool for asset protection.

The Cost of Inaction

Without an agreement in place, you and the remaining partners could find yourselves forced into business with an heir you’ve never met. You might face a drawn-out, expensive legal battle just to determine the value of the departing owner's shares. I have seen situations where businesses had to liquidate valuable assets just to buy out a deceased partner's family, putting the company's financial health on life support.

This is precisely why you cannot afford to wait. Surveys of private U.S. companies show that somewhere between 60% and 80% already have a buy-sell or succession plan. They understand these agreements are vital for preventing fights over valuation and keeping the business running smoothly after a triggering event. For additional insights, you can find more information about buy-sell agreements on deloitte.com.

Protecting Your Legacy and Your Partners Under Texas Law

A buy-sell agreement brings peace of mind by answering the tough questions ahead of time. While a template is a useful starting point, tailoring it to your specific business and Texas legal requirements is what truly matters.

A thoughtful agreement accomplishes several key objectives:

- Creates a Guaranteed Market: It ensures a departing owner (or their estate) has a ready buyer for their shares at a predetermined, fair price.

- Maintains Control: It prevents ownership from falling into the hands of outsiders, competitors, or family members who aren't equipped to be partners.

- Establishes a Fair Valuation: The agreement locks in a clear method for valuing the business, which sidesteps emotional and costly disputes down the road.

- Provides Liquidity: It is often paired with funding mechanisms, like life insurance policies, to ensure cash is available for the buyout when needed.

Ultimately, this document is a testament to the respect and commitment you have for your partners. It aligns your business objectives with your personal estate planning to protect your family, your business, and the legacy you're all building together.

Getting to the Heart of Your Agreement

A generic, fill-in-the-blank template you find online is not sufficient when your Texas business is on the line. To turn a basic document into a true legal shield, you must define its core mechanics. These clauses eliminate ambiguity and ensure the agreement functions as intended during stressful times.

The real strength of your agreement lies in the details. Vague terms or unaddressed scenarios can spark the very disputes you are trying to prevent. Let's break down the essential components you need to define for an effective agreement built on solid Texas law.

Defining Your Triggering Events

The engine of any buy-sell agreement is its list of triggering events—the specific situations that initiate the buyout process. Simply listing "death" or "retirement" is insufficient and risky. You must plan for every potential event that could disrupt your ownership structure.

Here’s a real-world scenario we often see: a partner in a thriving Austin tech startup gets divorced. If the buy-sell agreement lacks a specific divorce clause, their ex-spouse could be awarded half their shares in the settlement. Suddenly, you have a new co-owner you never intended. This is why you must be explicit.

Common triggering events you must define clearly include:

- Death or Long-Term Disability: Do not just say "disability." Define it clearly, for instance, as the inability to perform key duties for 180 consecutive days.

- Voluntary Retirement: Specify the required notice period and the exact terms of the exit.

- Divorce: This is critical. Add a clause stating that business shares involved in a divorce settlement automatically trigger a buyout option for the remaining partners.

- Personal Bankruptcy: This prevents a bankruptcy trustee from seizing the owner's shares and selling them to the highest bidder to pay creditors.

- Termination of Employment: What happens if a partner is fired for cause? What if they simply resign? Plan for both scenarios.

Meticulously detailing these events removes guesswork during a crisis. It creates a clear, automatic path forward, which is a cornerstone of any effective family business succession planning.

Transfer Restrictions and the Right of First Refusal

Another vital function of the agreement is to act as a gatekeeper, controlling who can own a piece of your company. Transfer restrictions are the legal guardrails that prevent a business partner from selling or transferring their shares to an unknown third party without the other owners' consent.

The most common tool for this is the Right of First Refusal (ROFR). It’s simple yet powerful. If an owner receives a legitimate offer for their shares from an outsider, the ROFR requires them to first offer those shares to the company or the other owners on the exact same terms. This gives the remaining partners the first opportunity to keep ownership within the trusted circle.

The Heart of the Matter: Valuation Mechanisms

Determining a fair price is almost always the most contentious part of a buyout. A vague valuation clause is a lawsuit waiting to happen. Your agreement must state, in no uncertain terms, how the business will be valued when a trigger event occurs.

There are generally three ways to do this:

- Fixed Price: The owners agree on a set value—for example, $1 million—and commit to updating it annually. While simple, owners often forget to update it, and an outdated valuation can be disastrously inaccurate.

- Formula-Based Value: The price is set by a formula, such as a multiple of earnings (EBITDA) or revenue. It is more dynamic than a fixed price, but a rigid formula can easily miss the company's true current worth.

- Third-Party Appraisal: A qualified, independent appraiser determines the value when the buyout is triggered. This is often the fairest and most legally sound method.

To ensure a fair and accurate price, it is wise to write the use of professional business valuation services directly into your agreement. The "fair market value" standard is preferred by courts and appraisers, but getting it wrong is a significant risk. I have seen formulas under- or overstate a company's value by 10%–30%. For a multi-million dollar business, that mistake can shift a fortune from one party to another.

Key Takeaway: Do not rush the valuation clause. It is the financial bedrock of the entire agreement. A clear, well-defined method protects not only the departing owner's family but also the financial health of the business you've worked so hard to build.

How to Fund Your Business Buyout

A buy-sell agreement that outlines triggering events and valuation is a great start. But without a clear funding mechanism, it’s merely an empty promise.

When a buyout is triggered, the question isn't if the departing owner or their family gets paid—it's how. A solid funding plan ensures the cash is available when needed, preventing the business from having to sell assets or take on crushing debt during an already stressful time.

This is where your legal strategy and financial planning must align. Your agreement is only as good as the funding you have to back it.

Using Insurance to Secure the Buyout

For the most common and disruptive buyout triggers—death or permanent disability—life and disability insurance are the gold standard for funding. These policies provide a predictable, immediate, and often tax-advantaged source of cash right when it’s needed most.

Imagine two partners running a successful construction company in Houston. If one partner tragically passes away, a life insurance policy pays a death benefit directly to the surviving partner or the company. That cash is then used to purchase the deceased partner's shares from their estate. This creates a clean break: the family receives immediate liquidity, and the business continues with a seamless ownership transition.

Without that policy, the surviving partner would be forced to scramble, perhaps draining the company's cash reserves or seeking a bank loan, putting the entire operation at risk.

This is why a Texas trust administration lawyer often recommends life insurance policies owned by either the company (for a redemption agreement) or the individual owners (for a cross-purchase agreement). Getting the ownership and beneficiary details right is crucial to avoid denied payouts or unexpected tax consequences. For a deeper dive, aafcpa.com explains how buy-sell agreements and life insurance intersect.

Common Funding Methods Compared

Insurance is a powerful tool, but it doesn’t cover every situation, such as retirement or a voluntary exit. Texas business owners should have several funding options available to build a resilient buyout plan.

| Funding Method | How It Works | Best For | Potential Downsides |

|---|---|---|---|

| Life/Disability Insurance | Policies are taken out on each owner, with proceeds earmarked for a buyout. | Death, long-term disability. | Doesn't cover retirement, divorce, or voluntary exits. |

| Cash Reserves | The business uses its accumulated cash on hand to fund the buyout. | Smaller buyouts; highly profitable, cash-rich businesses. | Can drain working capital needed for operations and growth. |

| Sinking Fund | The company sets aside money regularly into a dedicated investment account. | Planned exits like retirement. | Funds may not be sufficient if a trigger event happens early. |

| Installment Plan | The company pays the departing owner or their estate in installments over time. | Situations where immediate cash is unavailable. | Places a long-term financial burden on the business. |

| Third-Party Loan | The business or remaining owners secure a bank loan to fund the buyout. | Large buyouts when other options aren't feasible. | Adds debt and interest payments; loan approval isn't guaranteed. |

Structuring Installment Plans and Seller Financing

When a large lump-sum payment is not feasible, an installment plan—also known as seller financing—can be a practical solution. In this arrangement, the departing owner (or their estate) effectively acts as the lender. The business buys their shares and pays them back over an agreed-upon timeline, with interest.

This plan must be meticulously detailed in your buy-sell agreement. You need to define:

- The total purchase price.

- The down payment amount.

- The interest rate on the outstanding balance.

- The payment schedule (e.g., monthly or quarterly).

- The collateral securing the note (often the shares themselves).

This approach can be a lifeline for a business without deep cash reserves, but it requires trust and a rock-solid legal framework to protect both parties. The remaining owners are under a microscope here—their fiduciary duties in Texas are heightened because they must manage the company effectively to make those payments. For more on business transitions, this practical guide on how to purchase a small business offers insights that complement buyout funding strategies.

Plan for the Unexpected: The smartest strategies often use a hybrid approach. You might use insurance for death and disability while creating a clear plan for using cash reserves or an installment sale for events like retirement. An experienced Texas estate planning attorney can help you model these scenarios and build a funding plan that protects your business from every angle.

Choosing Your Agreement Structure

Deciding on the structure for your buy-sell agreement is one of the most critical decisions you and your partners will make. This choice impacts future tax liabilities, administrative burdens, and ultimately, who controls the company's future. It requires careful consideration of both immediate convenience and long-term financial reality.

The two primary structures for a buy sell agreement template are the Cross-Purchase Agreement and the Redemption Agreement. Both achieve a clean transfer of ownership, but they take different paths. Understanding the difference is essential for protecting your interests and ensuring the agreement works for your business.

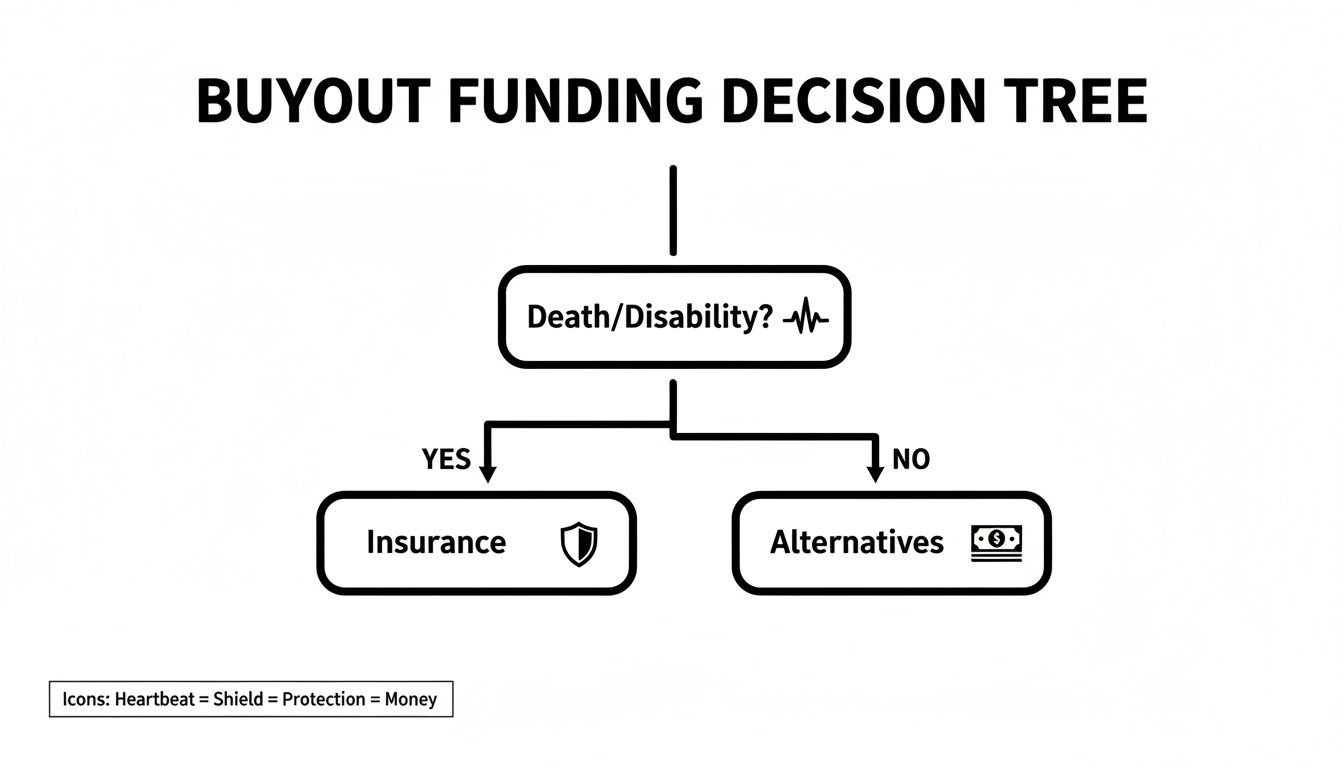

This decision tree provides a high-level overview of how the process often begins, with the funding source determined by the triggering event.

As you can see, events like death or disability often point toward an insurance-funded buyout, while other triggers require different financial plans. This initial funding question is a major factor in determining which agreement structure is most suitable for you and your partners.

The Cross-Purchase Agreement Explained

In a cross-purchase agreement, the owners themselves agree to personally buy a departing partner's shares. The business is not a party to the transaction; it is a direct deal between the partners.

For example, in a three-partner business valued at $1.5 million, each partner holds a $500,000 stake. If one partner leaves, the two remaining partners would each purchase half of that person’s shares. This structure is popular for one significant reason: taxes.

- The Tax Advantage (Step-Up in Basis): The surviving owners receive a "step-up" in their cost basis for the shares they purchase. This is a huge benefit, as it means their capital gains tax liability will be significantly lower when they eventually sell their own shares. It's a powerful tool for long-term wealth preservation.

- The Funding Complexity: When funded with life insurance, this structure can become complicated. Each partner must own a policy on every other partner. With two partners, this means two policies. With five partners, it requires 20 separate policies (5 partners x 4 policies each). The administrative burden can become overwhelming.

Understanding the Redemption Agreement

Conversely, a redemption agreement (or entity-purchase agreement) puts the business itself in the buyer's role. When a trigger event occurs, the company buys back—or "redeems"—the departing owner's shares. These redeemed shares are typically retired, which automatically increases the ownership percentage of the remaining partners.

This approach prioritizes simplicity, especially for funding.

- Administrative Simplicity: The company only needs to own one life insurance policy on each owner. For a five-partner firm, that’s just five policies instead of the 20 required for a cross-purchase agreement. This is a massive administrative advantage.

- The Tax Disadvantage: The remaining owners do not receive a step-up in their cost basis. Their original investment amount remains the same, which could lead to a much larger capital gains tax liability when they eventually sell.

The Key Trade-Off: A cross-purchase agreement offers a significant tax advantage but can become administratively complex with more than two or three partners. A redemption agreement is far simpler to manage but forgoes these valuable tax benefits.

To help you visualize the differences, here’s a side-by-side comparison.

Comparing Cross-Purchase and Redemption Agreement Structures

This table breaks down the core differences between the two main buy-sell agreement structures. Use it to help you and your partners determine which approach is the better fit for your company.

| Feature | Cross-Purchase Agreement | Redemption (Entity-Purchase) Agreement |

|---|---|---|

| Buyer of Shares | The remaining individual business owners. | The business entity itself. |

| Tax Basis for Buyers | "Step-up" in basis. Remaining owners get a higher cost basis, reducing future capital gains tax. | No step-up in basis. The cost basis for remaining owners does not change. |

| Funding Complexity | High. Requires N x (N-1) life insurance policies, which becomes unmanageable for many partners. | Low. The company only needs one life insurance policy per owner. |

| Best For | Businesses with only two or three owners who want to maximize tax benefits. | Businesses with multiple owners where administrative simplicity is a top priority. |

| Potential Issues | Funding disparities if owners are of different ages/health; administrative burden. | Can create tax issues for C-corporations (accumulated earnings tax). |

Ultimately, there is no single "right" answer—only the right answer for your business.

Choosing the right structure is a foundational decision for your company's future. For a deeper dive into the legal mechanics, our guide on how to transfer business ownership offers more context. Discussing these trade-offs with an experienced Texas business attorney is the best way to ensure you choose the structure that protects both your company's financial health and your personal legacy.

Aligning Your Business Plan with Your Estate Plan

Your buy-sell agreement is more than just a business document; it is the critical bridge connecting your business life to your personal estate plan. Many Texas business owners treat these as two separate worlds, but they are deeply intertwined. When that connection is weak, the fallout can be devastating for both your family and the company you’ve worked so hard to build.

A well-crafted buy-sell agreement should work hand-in-glove with your will and trusts. This alignment ensures a smooth transition that protects everyone's interests. Without it, you risk a legal battle between your business partners and your heirs, leading to staggering legal bills and emotional heartbreak.

Providing Essential Liquidity for Your Estate

One of the most powerful functions of a buy-sell agreement is its ability to create instant liquidity for your estate when it is needed most—after your death. For example, if a business owner passes away, their estate may face a significant estate tax bill. If most of their wealth is tied up in the business, where will the cash to pay that bill come from?

This is where the agreement proves its worth. By guaranteeing a buyer for your business interest at a fair, pre-agreed price, the buy-sell agreement transforms an illiquid business asset into cash. This cash infusion provides your executor with the funds to pay taxes, settle debts, and provide for your family's immediate needs without being forced into a fire sale of business assets.

A properly funded buy-sell agreement is one of the most effective asset protection tools a business owner can have. It ensures your family receives the full value of your life's work, not just pennies on the dollar from a rushed sale.

Avoiding Conflicts Between Your Will and Your Business

Here is a scenario we have seen cause chaos: Your will states that your shares in the family business should pass to your eldest child. However, your buy-sell agreement mandates that upon your death, the remaining partners have the first right to purchase your shares. Which document prevails?

This classic conflict can bring both your estate and your business to a halt. The key to avoiding this is to ensure your estate planning documents, such as your will or revocable living trust, explicitly acknowledge and defer to the terms of the buy-sell agreement.

Your will should direct your executor to comply with the sale required by the buy-sell agreement. The cash from that sale then flows into your estate and is distributed to your beneficiaries according to your will's instructions. This creates a clear, legally enforceable path and prevents disputes before they can begin.

The Executor’s Fiduciary Duties in a Business Sale

When you name an executor in your will, you are appointing a fiduciary. Under the Texas Estates Code, that person has a strict legal duty to act in the best interests of the estate and its beneficiaries. Navigating a business buyout adds significant complexity to these responsibilities.

An executor's role in this situation includes:

- Enforcing the Agreement: They are legally required to ensure the surviving partners or the company adhere to the valuation and payment terms laid out in the buy-sell agreement.

- Prudent Management: Until the sale is complete, they are responsible for managing the estate's interest in the business.

- Transparent Communication: They must keep the beneficiaries informed about the progress of the buyout.

A buy-sell agreement with clear instructions makes the executor's job infinitely easier and reduces their personal liability. It provides a definitive roadmap for valuation, payment terms, and timelines, removing guesswork. An experienced Texas estate planning attorney is essential to help you draft these interlocking documents, ensuring every fiduciary duty is clearly defined and legally sound.

Making Your Agreement Legally Sound

You’ve worked through the key clauses and determined how to fund it, but that **buy sell agreement template** is still just a draft. How do you transform it into an ironclad legal document that will hold up when you need it most?

This is the final and most critical step: moving from a generic template to a customized agreement tailored to Texas law and the reality of your business. Professional legal guidance is not just a good idea—it is absolutely essential.

Viewing an attorney as just another cost is a common mistake. In reality, legal counsel is a vital investment in the long-term health of your business and your family's financial security. An experienced Texas business attorney is trained to pressure-test your plan, identifying gaps and vague language that could lead to costly disputes later.

The Attorney’s Role in Customization

A good attorney does far more than just fill in blanks on a form. Their job is to ensure your agreement is fully compliant with the Texas Business Organizations Code and, just as importantly, that it syncs perfectly with your personal estate plan. This connection is crucial for a smooth transfer of wealth.

An attorney will:

- Sharpen the definition of "disability" to remove any subjectivity that could be debated later.

- Confirm that your chosen valuation method is not just fair but also legally defensible.

- Explain the real-world tax consequences of choosing a cross-purchase versus a redemption structure.

They bring a level of scrutiny and experience that no template can offer, transforming a good plan into a bulletproof one. Selecting the right legal partner is a major decision, and our guide on choosing the right estate planning attorney can provide valuable pointers.

This Is a Living Document

Finally, remember that a buy-sell agreement is not a document you sign once and forget. It is a living document because your business is a living entity. Its value will fluctuate, partners may change, and major life events will shift everyone's personal circumstances.

Key Takeaway: Your agreement needs regular check-ups. A good rule of thumb is to review it at least every three to five years, or immediately after any significant event, such as a new partner joining, a large jump in valuation, or a key owner's divorce. An outdated agreement can be as dangerous as having no agreement at all. Regular reviews with your legal and financial team are what keep it sharp and effective.

Common Questions About Texas Buy-Sell Agreements

When preparing a buy-sell agreement template, many questions arise. This is completely normal. Getting clear answers is the only way to feel confident that you are making the right decisions for your company's future and building your plan on solid ground. Let's address some of the most common questions we hear from Texas business owners.

What Events Should Actually Trigger a Buyout?

A common mistake is to only plan for major events like a partner's death or retirement. To truly protect your business, your agreement must be specific and define a comprehensive range of triggers.

Think beyond the basics. You should cover events such as:

- Death or Permanent Disability: Be specific. A good starting point is defining disability as the inability to perform regular duties for 180 consecutive days.

- Divorce: This is crucial. This clause prevents a partner's ex-spouse from becoming your new business partner through a divorce settlement.

- Personal Bankruptcy: You need to prevent a partner's personal creditors from seizing their shares and forcing a liquidation.

- Loss of a Professional License: This is critical for businesses built on licensed professionals, such as medical practices, engineering firms, or law offices.

- Involuntary Termination: The agreement must clearly outline the exit process if a partner is fired for cause.

How Often Should We Review This Agreement?

A buy-sell agreement is not something you sign and file away forever. Your business evolves, people's lives change, and your agreement must adapt accordingly.

We advise all our clients to review their buy-sell agreement with their attorney at least every three to five years. You should also review it immediately after any major business or life event—a significant change in valuation, bringing on a new partner, or a partner getting married or divorced. An outdated agreement can be just as problematic as having none at all.

What Happens If We Can't Agree on the Price?

Disputes over valuation are the leading cause of conflict in a buyout. That is why your agreement must lock in the valuation method from the beginning.

The cleanest and most defensible approach is to mandate a third-party appraisal by a qualified, neutral expert. This removes emotion, guesswork, and ego from the process. The price is set based on objective data, which is what an executor needs to fulfill their fiduciary duties under the Texas Estates Code.

If you’re managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.

Find out more at https://texastrustadministration.com.