Planning for your family's future can feel overwhelming, especially when faced with complex legal terms. Two of the most important terms you'll encounter in Texas estate planning are per stirpes and per capita. These aren't just technical jargon; they are specific instructions that determine how your legacy is distributed, particularly if a beneficiary passes away before you do. Making an informed choice is a critical step toward building a plan that honors your intentions and protects your loved ones.

The choice you make is governed by the Texas Estates Code and can significantly impact your family's future. With the right legal guidance, you can navigate these decisions with confidence and clarity.

Understanding Your Legacy Distribution Options

At its heart, the difference between per stirpes ("by the branch") and per capita ("by the head") comes down to one question: what happens if one of your children dies before you?

With a per stirpes distribution, your deceased child’s share is not lost. Instead, it flows down to their own children (your grandchildren), preserving that entire family "branch." In contrast, per capita divides the assets equally among only the living members of a specific group, which can sometimes leave grandchildren with a different share than they might expect—or even leave them out entirely if their parent is no longer alive.

Thinking through these scenarios is especially vital if you have complex assets, like a family business. For a deeper look at those unique challenges, this guide on Estate Planning for Business Owners is a great resource.

Here’s a practical side-by-side look to make the difference clear.

| Feature | Per Stirpes (By the Branch) | Per Capita (By the Head) |

|---|---|---|

| Primary Goal | Preserves an equal share for each family line or "branch." | Promotes equal distribution among living individuals in a group. |

| Deceased Beneficiary | Their share automatically passes down to their direct descendants. | Their share gets redistributed among the other living beneficiaries. |

| Grandchildren's Share | Grandchildren inherit only if their parent (your child) is deceased. | Grandchildren may inherit nothing or an equal share, depending on the wording. |

A well-crafted Texas estate plan ensures your legacy is protected and your intentions are crystal clear, preventing potential family disputes before they can begin.

Understanding Per Stirpes Distribution by the Branch

Per stirpes, a Latin term that translates to "by the branch," is a traditional and powerful method for distributing your assets that honors each distinct line of your family. The easiest way to think about it is to picture your family tree—this approach treats each of your children as a primary "branch."

Here is the core principle: if one of your children passes away before you, their intended share of the inheritance isn’t lost or split among your surviving children. Instead, that share flows directly down to their own children—your grandchildren—in equal portions. This method is often the default in Texas precisely because it helps prevent the unintentional disinheritance of grandchildren, which can be a common and painful source of family conflict.

This approach is especially favored by families looking to preserve generational wealth within specific family lines. It ensures the legacy you intended for one child is passed to their direct descendants, keeping that family branch financially secure.

How Per Stirpes Works in a Texas Scenario

To see this principle in action, let's walk through a clear, real-world scenario.

Imagine you are a Texas grandparent with a $1 million estate. Your will, drafted by a Texas estate planning attorney, states that your two adult children will each inherit 50%, with the distribution to be made "per stirpes." Tragically, one of your children predeceases you, leaving behind two of their own children—your grandchildren.

Under the per stirpes rule, your surviving child still receives their full 50% share, or $500,000. The other 50% that was intended for your deceased child is then split equally between their two children. This means each of your grandchildren would receive 25% of the total estate, or $250,000.

This outcome is exactly why per stirpes is the default in over 70% of life insurance policies nationwide—it prevents grandchildren from being accidentally cut out, a situation affecting an estimated 22% of U.S. estates. Under the Texas Estates Code, this method is designed to preserve family branches, which is particularly vital for high-net-worth families. You can find more insights on these trends in this 2023 report on life insurance beneficiaries.

Key Takeaway: Per stirpes ensures that if a beneficiary dies before you do, their share automatically passes down to their own heirs. It respects the "branch" of the family, not just the individual people.

Without this specific instruction in your will or trust, those grandchildren might end up with nothing. That kind of oversight can spark painful legal disputes that tie up a significant portion of an estate's value in litigation. Proper asset protection strategies always begin with crystal-clear distribution language.

A Closer Look at Per Capita Distribution

While per stirpes focuses on preserving the shares of family branches, per capita—which means "by the head"—offers a different approach. It is a more modern method that prioritizes equal distribution among individuals at the same generational level. In its simplest form, this method divides the estate equally only among the living members of a specific group, such as your children.

Here is the critical distinction: if a child passes away before you, their own children (your grandchildren) would receive nothing under a strict "per capita to my children" clause. This detail can completely reshape your family’s financial future and demonstrates how vital precise wording is in your will or trust.

However, a more common and equitable version is called per capita at each generation. This approach pools the shares of any deceased heirs and then divides that pool equally among their children. The result is that every grandchild receives the exact same share, regardless of how many siblings their parent had.

How Per Capita Plays Out in a Texas Scenario

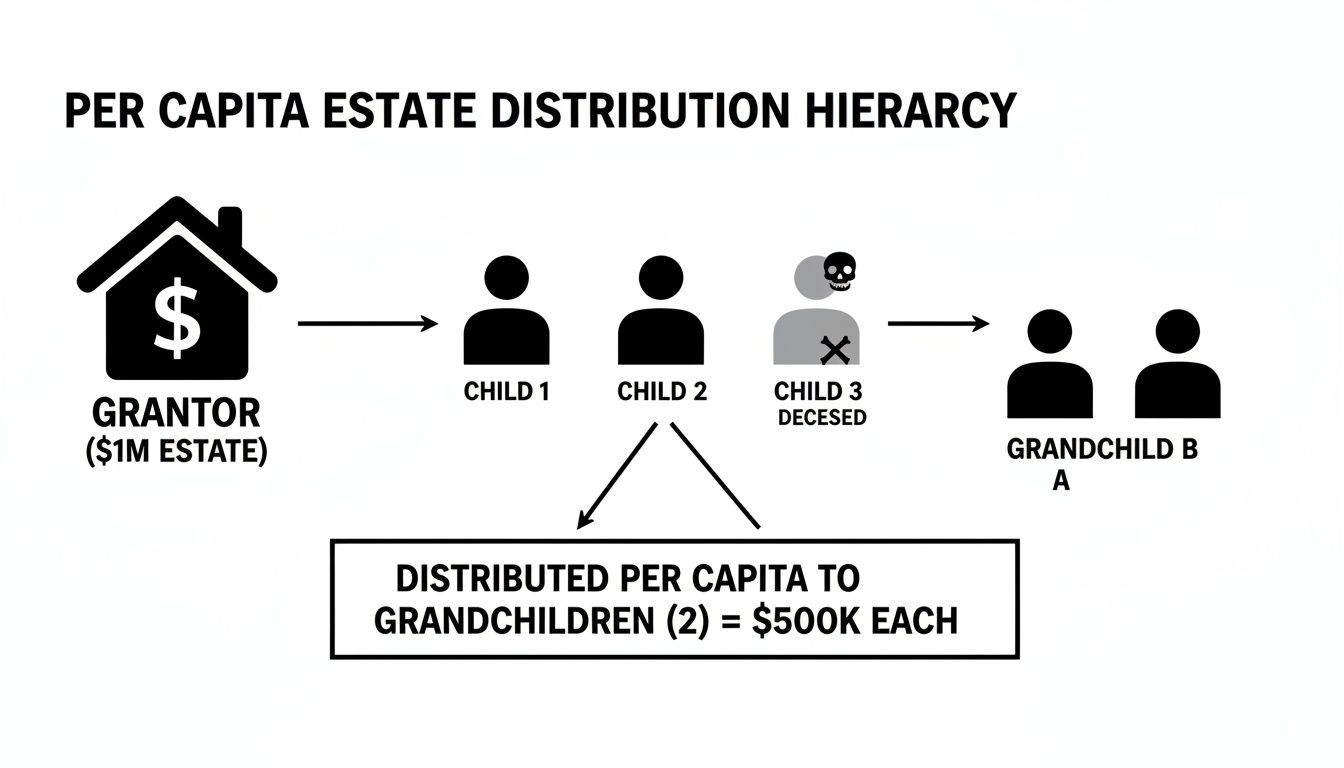

Let’s imagine a family in Texas with an $800,000 estate. The will directs that the assets be distributed "per capita" to the descendants. The person who made the will had three children, but one of them died before they did, leaving three grandchildren behind.

Under a strict "per capita to my children" instruction, the outcome is stark. Only the two surviving children would inherit. They would split the estate, each taking 50% ($400,000), and the three grandchildren would be left with nothing.

However, if the will simply says "to my descendants, per capita," the probate process looks very different. The court would likely interpret this to include all descendants equally. That means the two living children and three grandchildren—five people in total—would each receive an equal 20% share, or $160,000.

Key Takeaway: Per capita is all about creating equal shares for living individuals in a defined group. The difference between naming "children" versus "descendants" is massive and can change everything. Precision is non-negotiable.

This method often feels fairer by ensuring equal shares across a generation. But it can also spark conflict, especially if grandchildren were expecting to inherit what would have been their parent's full share. Here in Texas, where our firm handles trust administration under the Texas Trust Code, we often see per capita used for nuclear or blended families. With U.S. divorce rates hovering between 40-50%, many people choose this method to avoid unintentionally favoring one side of the family over another.

You can dive deeper into how these distribution choices affect estates by reading these findings on estate planning trends. A skilled Texas estate planning attorney can sit down with you and determine if this modern approach truly aligns with your wishes for your family.

Comparing Distribution Outcomes in a Texas Estate

The legal theory behind per stirpes and per capita is one thing; seeing the real-world financial impact on your family is another. The difference between these two methods becomes clear when you run the numbers for a typical Texas family, showing just how much your choice can alter who inherits your legacy. This isn't just about abstract legal definitions—it's about tangible consequences for your loved ones.

To see what this means in practice, let’s walk through a common Texas family scenario.

A Practical Texas Estate Scenario

Imagine you have a $1.2 million estate and three adult children: Alice, Ben, and Clara.

- Alice is alive and well.

- Ben has passed away, leaving behind his two children (your grandchildren), David and Emily.

- Clara has also passed away, but she left behind only one child (your grandchild), Frank.

This kind of scenario, with a mix of living and deceased children and a different number of grandchildren in each family line, is exactly where the distinction between per stirpes and per capita becomes so important.

Distribution Outcome: Per Stirpes

Under a per stirpes (by the branch) distribution, your estate is first split into three equal shares—one for each of your children's family lines.

- Alice's Share: Since Alice is still living, she receives her full one-third share, which is $400,000.

- Ben's Share: Ben’s one-third share ($400,000) doesn't disappear. Instead, it flows down to his two children, David and Emily. They split their father's portion equally, each receiving $200,000.

- Clara's Share: Clara’s one-third share ($400,000) passes directly to her only child, Frank. He receives the entire $400,000.

With per stirpes, what each grandchild inherits is tied directly to their parent's original share. Notice how Frank receives double what David and Emily each receive.

Distribution Outcome: Per Capita at Each Generation

Now, let's see how a per capita at each generation approach completely changes the outcome for the grandchildren. This method is all about treating everyone at the same generational level equally.

- Alice's Share: Alice is in the first generation of beneficiaries, so she still receives her one-third share of $400,000. No change there.

- The Grandchildren's Pool: Here's the big difference. The remaining two-thirds of the estate ($800,000)—the parts that would have gone to Ben and Clara—is pooled together into a single pot.

- Equal Split for Grandchildren: This $800,000 pool is then divided equally among all three grandchildren (David, Emily, and Frank). Each grandchild now receives approximately $266,667.

The infographic below helps visualize how per capita distribution pools assets and divides them equally among the next generation.

This perfectly illustrates the core principle of per capita at each generation—it prioritizes equality among beneficiaries at the same level, regardless of their family branch.

A Critical Insight: In major U.S. markets like Texas, the choice between per stirpes and per capita profoundly sways multi-generational wealth. An analysis of over 5,000 estate plans found that using per stirpes can cut the risk of litigation by 22%, a vital consideration as nearly one in three U.S. wills faces a beneficiary dispute. You can explore more data on these legacy planning decisions from Sandhill Global Advisors.

A solid grasp of these outcomes is the first step toward effective asset protection and making sure your estate plan does what you intend.

Per Stirpes vs Per Capita: A Head-to-Head Comparison

To make it even clearer, this table breaks down the core philosophies and financial results of each approach using our Texas family scenario. It’s a quick way to see the fundamental differences side-by-side.

| Feature | Per Stirpes (By the Branch) | Per Capita (By the Head) |

|---|---|---|

| Core Philosophy | Preserves the share of each family line, treating each branch equally. | Promotes equality among individuals in the same generation, regardless of their branch. |

| Grandchild Inheritance | Varies based on their parent's share and how many siblings they have to split it with. | All grandchildren receive an identical amount because their shares are pooled. |

| Common Use Case | Best when you want to ensure each of your children's families benefits as a whole. | Ideal when you want to treat all of your grandchildren the same, no matter what. |

Seeing the numbers laid out like this highlights how your decision impacts the next generation. Whether you are navigating the complexities of probate or planning your own estate, a Texas trust administration lawyer can provide the clarity you need to make the right choice for your family.

Picking the Right Path for Your Family

Choosing how your assets are divided is not just a legal checkbox; it's a profoundly personal decision that reflects your values and vision for your family's future. The choice between per stirpes and per capita depends on your unique family structure, your relationships, and what you hope to achieve with your legacy. There is no single "right" answer—only the one that truly reflects your intentions.

Making this call means taking an honest look at your family's dynamics and considering how things might change. A seasoned Texas estate planning attorney is invaluable here, helping you think through the "what-ifs" to ensure your will or trust is a perfect reflection of your goals.

When Per Stirpes Makes the Most Sense

Per stirpes is the ideal choice for people who see their family in terms of distinct branches. If your primary goal is to ensure each of your children's family lines receives an equal share of your estate, no matter what happens, then per stirpes is almost certainly your best fit.

This traditional method is particularly well-suited for a few common scenarios:

- Protecting Generational Lines: You want a guarantee that your grandchildren will inherit their parent's portion if that parent passes away before you do. This approach prevents an entire branch of your family from being accidentally disinherited.

- Balancing Uneven Grandchild Numbers: Perhaps one of your children has more children than another. Per stirpes keeps things fair by giving each child's family unit the same foundational share. The focus is on equity between your children's lines, not necessarily giving every single grandchild the same amount.

- Passing Down Legacy Assets: When you have a specific asset—like a family business or a beloved vacation home—that is meant to stay within one side of the family, per stirpes is the legal tool that directs that inheritance down the correct branch.

The Core Idea: Think of per stirpes as a promise you're making to each of your children's families. It's like saying, "The share I've set aside for your branch of the family will stay with your branch, passing to your kids if you're not here to receive it."

This method offers a predictable, classic structure that honors the traditional family tree. It's the default in Texas for a good reason—it aligns with the common desire to provide for a child's descendants if that child is no longer with us.

When to Consider a Per Capita Approach

On the other hand, per capita is for those who prioritize equality among individuals in the same generation. If you are more focused on treating all your beneficiaries at a certain level—especially all your grandchildren—in the exact same way, then a per capita distribution might be what you're looking for.

You should seriously consider per capita if your family situation looks like this:

- A Drive for Grandchild Equality: If your heartfelt wish is for every single one of your grandchildren to receive the exact same inheritance, "per capita at each generation" is the only way to make that happen. It pools the shares of any children who have passed away and divides that portion equally among all the grandchildren.

- Navigating Blended Families: In families with step-children and step-grandchildren, per capita can be a powerful tool for creating fairness. It allows you to name every beneficiary you want to include individually and distribute your assets "by the head," making sure everyone you've named gets an equal share, regardless of bloodline.

- Smaller, Tightly-Knit Families: If your family is small and you feel a closer bond to all your descendants as individuals rather than as members of separate branches, per capita can better reflect that modern, close-knit family view.

Making this choice demands a serious look at your family's specific needs. For example, if you're planning for a guardianship for a minor who might inherit, the way they inherit matters a great deal. Talking through these details with a lawyer who understands fiduciary duties in Texas is essential for protecting vulnerable loved ones. The right strategy ensures your legacy is a source of support, not conflict. For particularly complex situations, a well-drafted trust is often the best vehicle for true asset protection.

How to Draft Your Will to Prevent Ambiguity

A strong estate plan lives and dies by its clarity. Ambiguous language in a will or trust can open the door to costly probate fights and painful family feuds that undermine your intentions. Simply deciding between per stirpes and per capita isn't enough; that choice must be captured in precise, legally sound language that leaves zero room for misinterpretation by an executor or a Texas court.

This is where expert legal drafting becomes critical. The difference between a smooth trust administration and a bitterly contested will often comes down to a few carefully chosen words.

The Dangers of Vague Language

One of the most common pitfalls is the use of broad, undefined terms. Phrases like "to my descendants" or "to be divided among my issue" might seem straightforward, but under the Texas Estates Code, they can create a legal hornet's nest.

Without explicit instructions, a court must fall back on default state rules. While Texas law typically defaults to a per stirpes distribution to prevent accidentally disinheriting a family line, that's not a guarantee. Relying on defaults means surrendering control and can lead to outcomes you never intended.

Beyond the distribution method, the overall clarity of the document is paramount. Applying the principles of mastering structure in writing can be a game-changer in creating a will that is airtight and easy to follow.

Sample Clauses for Clarity

A qualified Texas estate planning attorney will use specific, battle-tested language to translate your wishes into an ironclad document. The simplified examples below give you a sense of the detail required.

Example Per Stirpes Clause

"I give the residue of my estate in equal shares to my then-living children; provided, however, that if any child of mine should predecease me, that deceased child's share shall be distributed, per stirpes, to his or her then-living descendants."

This clause accomplishes two critical things: it clearly names the primary beneficiaries (your living children) and then explicitly directs that a deceased child's share flows down to their own children by representation. No guesswork is needed.

Example Per Capita at Each Generation Clause

"I give the residue of my estate to my then-living descendants, to be divided among them per capita at each generation. The initial division shall be made at the level of my children, and the shares of any deceased child shall be combined and distributed equally among the next generation of my descendants."

This language is more complex, but it is the only way to create the "pooling" effect that guarantees every grandchild receives an identical share, regardless of how many siblings they have.

Why DIY Wills Are a Risk

These examples highlight why drafting a will is not a do-it-yourself project. The subtle but powerful differences between terms like "descendants," "children," and "issue," combined with the specific instructions for "per stirpes" or "per capita," are critical. An experienced attorney knows how Texas courts interpret these words and can steer you clear of common blunders. You can learn more in our guide on preventing will contests by drafting airtight wills.

A Fiduciary's Perspective: An executor or trustee has a legal fiduciary duty to follow the will's instructions to the letter. Vague language puts them in an impossible position, often forcing them to ask a court for guidance (a process called a declaratory judgment). This drains estate assets and creates frustrating delays for all beneficiaries.

Investing in professional legal drafting is a form of asset protection. It safeguards not only your wealth but, more importantly, your family's harmony. A knowledgeable Texas trust administration lawyer can provide the precise language needed to lock in your intentions.

Your Top Questions About Texas Distribution Answered

Navigating the details of estate distribution can feel overwhelming, but you are not alone in your questions. Many Texas families weigh these same concerns. Our attorneys have provided clear, straightforward answers to the most common questions we hear about per stirpes and per capita distributions to help you move forward with confidence.

What Happens in Texas If My Will Doesn't Specify a Method?

This is an excellent question. If your will is vague or simply leaves assets "to my descendants" without specifying per stirpes or per capita, Texas law provides a default. The Texas Estates Code generally defaults to a per stirpes distribution.

This default rule exists to prevent a deceased child's entire family line from being accidentally disinherited, which is a common source of estate disputes.

However, relying on default rules is a gamble. A court might still need to interpret what you really wanted, and that process can consume time and money that belongs to your beneficiaries. The best course of action is always to work with a Texas estate planning attorney to explicitly state your chosen method in your will or trust.

Can I Use a Combination of Both Methods in My Estate Plan?

Yes, you can create a custom or hybrid distribution plan, but this requires the expertise of an experienced estate planning lawyer. This approach demands extremely precise drafting to avoid ambiguity. When done correctly, it can be a fantastic tool for achieving specific family goals.

For example, you might decide that the family business passes per stirpes to ensure it stays within a particular branch of the family. At the same time, you could distribute your cash and stocks per capita to all of your grandchildren equally.

While these hybrid plans can solve complex family dynamics, they also increase the risk of ambiguity if not drafted perfectly. A thorough consultation is essential to ensure the language is ironclad and accurately reflects your wishes without creating unintended conflicts. You can get a better sense of why precision is so important by reviewing the official will requirements in Texas.

How Do Blended Families Affect This Decision?

Blended families make the per stirpes vs. per capita choice even more critical. At its core, per stirpes is about bloodlines. It typically excludes step-children unless you have legally adopted them. Without careful planning, this can lead to heartache and confusion.

If your goal is to treat all your children and step-children equally, a per capita distribution is often a better fit. However, you must explicitly name the step-children as beneficiaries in the document.

A Critical Point for Blended Families: If you do not clearly define who you mean by "children" or "descendants," you could unintentionally disinherit your step-children. For blended families, a customized trust is often the most effective tool for ensuring everyone you intend to provide for is included.

Does My Choice Affect the Generation-Skipping Transfer Tax?

Absolutely. Your choice can have significant tax implications, especially for larger estates subject to federal tax rules. The Generation-Skipping Transfer (GST) tax is a federal tax on assets transferred to individuals two or more generations below you, such as your grandchildren.

A per capita distribution that sends assets directly to your grandchildren while their parent (your child) is still alive can easily trigger the GST tax if the amount exceeds the federal exemption. A per stirpes distribution is less likely to cause this issue unexpectedly, since assets typically only go to grandchildren if their parent has already passed away. A knowledgeable Texas estate planning attorney can structure your plan to maximize your GST tax exemption and minimize your family's tax burden.

If you’re managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.