Planning for your family's future while also supporting a cause you hold dear can feel overwhelming. But with the right legal guidance, you can secure a reliable income stream, gain significant tax advantages, and leave a meaningful legacy—all at the same time. The primary charitable remainder trust benefits transform complex assets into clear, reliable support for both you and your chosen charity. This powerful tool, recognized under the Texas Trust Code and federal tax law, allows you to achieve financial security and philanthropic goals without compromise.

An Introduction to Philanthropic Estate Planning

Many Texas families want to strike a balance between their own financial security and their desire to make a lasting impact. A Charitable Remainder Trust (CRT) is a well-established estate planning tool, recognized by the Internal Revenue Code, that lets you achieve both goals. And it’s not just for the ultra-wealthy; it's an accessible strategy for anyone with appreciated assets like stocks, real estate, or a business.

Think of a CRT as a special container you create. You place a valuable asset into it, and in return, the container pays you (or someone you choose) a steady income for a set number of years or for life. When that period ends, whatever is left inside the container—the "remainder"—goes to a charity you love.

This approach offers several powerful advantages for Texas residents:

- Create a Lasting Legacy: You can support a church, university, or nonprofit that is important to you, ensuring your values live on long after you're gone.

- Secure Your Financial Future: The trust provides a predictable income stream, which can become a vital part of your retirement plan.

- Achieve Significant Tax Savings: Transferring assets into a CRT can unlock immediate income tax deductions and help you sidestep capital gains taxes.

Effective philanthropic planning often means understanding the legal and tax framework that governs charitable organizations. For instance, familiarity with church law and tax essentials can be crucial for ensuring compliance and maximizing the impact of your contributions.

While the concept is straightforward, putting it into practice correctly requires careful attention to the Texas Trust Code and federal tax laws. The structure has some things in common with other philanthropic tools, but it's important to understand the distinctions. For those interested, you can also learn about the differences in our article on Charitable Lead Trusts: https://texastrustadministration.com/what-is-a-charitable-lead-trust/

An experienced Texas estate planning attorney can help you structure the trust to meet your specific financial and philanthropic goals, providing clarity and confidence every step of the way.

Understanding How a Charitable Remainder Trust Works

Think of a charitable remainder trust (CRT) as a brilliant way to split the value of an asset between two important groups: the people you care about today and the causes you believe in for tomorrow. It’s like setting up a philanthropic retirement plan. You place an asset into the trust now, get an income stream for a number of years, and then leave a powerful gift for a charity once the trust’s term is up. This isn't some newfangled idea; it’s a strategy well-established and approved by the IRS under Internal Revenue Code §664, giving you both security and peace of mind.

To really get how it all fits together, you need to know the cast of characters involved in any CRT:

- The Grantor: That’s you. You're the one creating the trust and funding it with your assets.

- The Trustee: This is the manager—an individual or an institution that invests the trust's assets and makes sure payments go out on time. A trustee has strict fiduciary duties in Texas and must always act in the beneficiaries' best interests.

- The Income Beneficiary: This is who gets the regular income checks. It could be you, your spouse, your kids, or anyone else you decide to name.

- The Charitable Beneficiary: This is the qualified 501(c)(3) organization that receives whatever is left in the trust at the very end.

The Basic Steps of a CRT

The whole process is more straightforward than it sounds. You’ll start by working with a Texas estate planning attorney to draft the actual trust document, making sure it reflects your exact wishes. Then, you transfer a highly appreciated asset—think stocks, real estate, or even a piece of a business—into the trust.

Once the asset is in the trust, the trustee sells it. Here’s the magic: because the trust itself is tax-exempt, that sale typically doesn’t trigger an immediate capital gains tax bill. This leaves the asset's full value intact and ready for reinvestment. The trust then begins paying a steady income to you or your beneficiaries for the term you’ve set. When that period ends, the "remainder" of the assets passes to your chosen charity, locking in your philanthropic legacy.

A CRT allows you to convert a highly appreciated, non-income-producing asset into a reliable stream of cash flow for your family, while simultaneously preparing a significant future gift for a cause you believe in. It’s a true win-win scenario for strategic givers.

A Proven Tool with a Deep History

Charitable remainder trusts have been around for a while. They were officially codified with the Tax Reform Act of 1969 and really hit their stride in the following decades. The 1990s, in particular, saw their popularity explode thanks to a roaring stock market and higher capital gains tax rates.

In fact, IRS data shows that from 1999 to 2002 alone, the number of charitable remainder unitrusts (CRUTs) shot up by an incredible 38%. This wasn't an accident. It was driven by sharp donors who saw CRTs as the perfect tool for managing major gains in a tax-smart way. If you're interested in the backstory, you can explore the evolution of these powerful tools and why they remain relevant today.

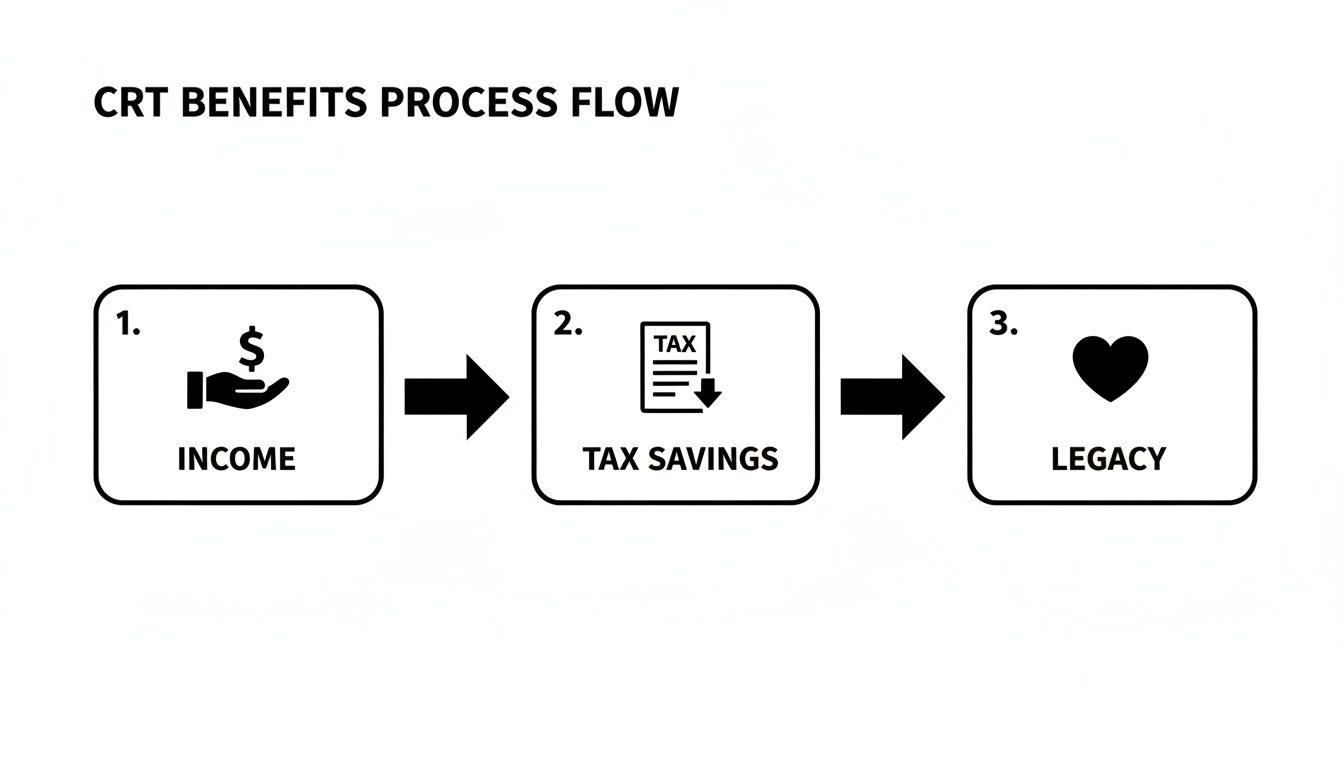

This simple graphic shows you just how powerful this flow of benefits can be.

As you can see, a single decision to establish a CRT branches out into immediate income for your family, major tax savings for you, and a lasting legacy for a cause you love. While the gears of this machine can seem intricate, a knowledgeable attorney will guide you through every turn. They'll ensure your trust is structured to comply with both federal tax law and the Texas Trust Code, giving you complete confidence in the plan you’ve built.

The Major Financial Benefits of a Charitable Remainder Trust

It’s one thing to feel good about supporting a cause you believe in. It’s another to realize that the very same tool can unlock a powerful suite of financial benefits for you and your family. A charitable remainder trust (CRT) isn't just about philanthropy; it's a strategic move that delivers tangible, calculable advantages. These benefits can profoundly enhance your financial security, slash your tax bill, and protect your wealth for the long haul.

Understanding how a CRT works for you financially is the first step toward a smarter, more impactful estate plan.

Gain an Immediate Income Tax Deduction

One of the most immediate and satisfying perks of a CRT is the tax break you get right away. The moment you fund the trust, you become eligible for a partial income tax deduction for that very same year. Why? Because the IRS recognizes that you’ve made a legally binding promise to make a future gift to charity.

The exact size of your deduction is a calculated figure, based on things like the trust’s payout rate, the age of the people receiving the income, and the federal interest rates at the time. A common deduction can be anywhere from 30% to 40% of the asset's value. To see it in action, one donor who funded a CRT that would pay out an initial $25,000 annually was able to claim an immediate $290,360 deduction. For someone in the 32% tax bracket, that translates to a real-world tax savings of $92,915—money that goes straight back into their pocket.

Avoid Capital Gains Taxes on Appreciated Assets

Many Texans are sitting on assets that have exploded in value—stocks, real estate, or a family business. If you were to sell those assets directly, you’d be hit with a massive capital gains tax bill, watching a huge chunk of your profits evaporate. This is where a CRT truly shines.

The strategy is elegant: you transfer the appreciated asset into the tax-exempt trust before you sell it. The trustee can then sell that asset for its full market value, and because the trust is tax-exempt, there’s no capital gains tax to pay. The entire sale proceeds can then be reinvested to generate income.

Example Scenario:

Picture a Dallas business owner with a commercial property bought years ago for $300,000. Today, it’s worth $1 million. A straight sale would create a $700,000 capital gain and a staggering tax liability. Instead, by placing it in a CRT first, the trust sells it tax-free. The full $1 million is now available to be invested, not the post-tax amount. That single move preserves hundreds of thousands of dollars.

A CRT allows you to unlock the full value of your most appreciated assets without taking a significant hit from capital gains tax. This is a cornerstone of tax-efficient charitable giving in estate planning.

To make these multi-faceted benefits easier to grasp, here’s a quick summary.

Key Tax Benefits of a Charitable Remainder Trust at a Glance

This table breaks down the primary ways a CRT can dramatically improve your tax situation, both now and in the future.

| Tax Benefit | How It Works | Example Impact |

|---|---|---|

| Income Tax Charitable Deduction | You receive a partial tax deduction in the year you fund the trust, based on the calculated future value of the gift to charity. | Funding a trust with a $1M asset could generate an immediate deduction of $300,000 or more, directly reducing your current year's tax bill. |

| Capital Gains Tax Avoidance | Transferring an appreciated asset to the trust before a sale allows the trust to sell it tax-free, preserving the full value for reinvestment. | Selling a $1M asset with a $700,000 gain inside a CRT avoids what could be a $140,000+ federal capital gains tax bill (at a 20% rate). |

| Estate Tax Reduction | Assets placed in a CRT are permanently removed from your taxable estate, lowering its total value for federal estate tax purposes. | Moving $2M into a CRT could shield that amount from a potential 40% federal estate tax, saving heirs up to $800,000 in taxes. |

As you can see, the tax advantages aren't just a side-effect; they are a core feature that can substantially increase your personal wealth while you support causes you care about.

Secure a Predictable Income Stream

For anyone planning their retirement or just looking to create another income source, financial stability is everything. A CRT is brilliant at converting a static, non-income-producing asset—like a piece of undeveloped land or a growth stock that doesn't pay dividends—into a dependable stream of payments for you or your family.

You get to choose how that income stream works:

- Fixed Payments: A Charitable Remainder Annuity Trust (CRAT) pays you a set dollar amount every year. This offers the highest level of predictability, perfect for budgeting.

- Variable Payments: A Charitable Remainder Unitrust (CRUT) pays a fixed percentage of the trust's value, which is recalculated each year. This means your income could grow if the trust's investments do well.

This structure provides a reliable cash flow for a specific number of years (up to 20) or for the entire lifetime of the income beneficiaries. It's a fantastic way to ensure your financial security is locked in.

Reduce Your Federal Taxable Estate

For Texas families with substantial wealth, the federal estate tax is a major hurdle. Any assets you leave to your heirs above the federal exemption threshold (currently over $13 million per person) get hit with a very steep tax. A CRT is one of the most effective strategies for shrinking the size of your taxable estate.

When you move assets into a CRT, they are officially no longer part of your estate. This means they won't be counted when it's time to calculate estate taxes. By methodically lowering the net value of your estate, you can significantly reduce—or even completely eliminate—your family's future estate tax bill. This isn't a loophole; it's a well-established strategy that benefits both charity and your heirs. An experienced Texas estate planning attorney can help you integrate a CRT into your broader plan to achieve the maximum effect.

Choosing Your Trust Structure: CRAT vs. CRUT

Once you’ve settled on creating a charitable remainder trust, you arrive at a critical fork in the road. This decision will define how you receive your income for years to come, and it comes down to two primary structures: the Charitable Remainder Annuity Trust (CRAT) and the Charitable Remainder Unitrust (CRUT).

While their names sound almost identical, their mechanics are worlds apart. Picking the right one is absolutely essential to aligning the trust with your personal financial goals. An experienced Texas estate planning attorney can model the specific outcomes, but your first step is to grasp the core differences.

Think of it this way: a CRAT is like a fixed pension, offering unwavering predictability. A CRUT, on the other hand, is more like an investment portfolio with a variable—but potentially growing—return.

The Charitable Remainder Annuity Trust (CRAT): Predictable and Stable

A CRAT is all about stability. When you establish a CRAT, it is built to pay you a fixed, unchanging dollar amount each year. This payment is calculated and set in stone the moment the trust is created, and it never changes, no matter how the trust's investments perform.

So, if you create a CRAT designed to pay you $50,000 annually, that is exactly what you will receive every single year for the life of the trust. This makes your financial planning incredibly straightforward.

Why a CRAT might be for you:

- Income Stability: You know precisely how much money is coming in each year. This is a massive plus for budgeting in retirement.

- Simplicity: The math is simple. There's no need for the trustee to revalue assets every year just to figure out your payment.

- Protection from Market Downturns: If the market takes a hit and the trust's investments dip, your income is shielded. Your payment remains the same.

Potential downsides of a CRAT:

- No Inflation Protection: That fixed $50,000 payment will have significantly less buying power 10 or 20 years from now.

- No Upside Potential: If the trust’s assets grow spectacularly, you won’t get to share in that success. Your payment is locked in.

- Inflexibility: You get one shot to fund it. After the initial contribution, you cannot add any more assets to a CRAT.

A CRAT is often the perfect fit for people at or near retirement who value a reliable, predictable income stream above all else.

The Charitable Remainder Unitrust (CRUT): Flexible with Growth Potential

By contrast, a CRUT is designed for flexibility and growth. Instead of a fixed dollar amount, a CRUT pays out a fixed percentage of the trust’s value each year. Because the trust's value can change, the payment is recalculated annually.

Let's say you set up a CRUT with a 5% payout rate and the assets are initially worth $1 million. Your first-year payment is $50,000. If strong investment performance grows the assets to $1.1 million the following year, your payment increases to $55,000. Of course, the reverse is also true; if the assets decline, so will your payment.

Why a CRUT might be a better fit:

- Potential for Income Growth: As the trust’s assets grow, your payments do too. This provides a natural hedge against inflation over the long term.

- Ability to Make Additional Contributions: Unlike a CRAT, you can add more assets to a CRUT down the road, which is a great feature for ongoing tax planning.

- Flexible Payout Structures: CRUTs have several variations that can be customized to meet specific needs, offering more advanced planning options.

Potential downsides of a CRUT:

- Variable Income: Your annual payments can go up or down, which makes precise budgeting more of a challenge.

- Exposure to Market Risk: If the trust’s investments have a bad year, your income for the next year will decrease accordingly.

- Administrative Complexity: The trustee must revalue the trust’s assets every single year to calculate the payment, adding an administrative task and cost.

A fiduciary in Texas acting as a trustee for a CRUT carries a heavy responsibility. They must have the expertise to prudently manage and accurately value the assets each year, a duty clearly defined in the Texas Trust Code. This makes your choice of trustee especially critical.

CRAT vs. CRUT: Which Charitable Trust Is Right for You?

So, how do you choose? The right answer depends entirely on your personal circumstances, your tolerance for risk, and what you want this trust to achieve. To help families in Austin, San Antonio, and The Woodlands weigh their options, here’s a direct comparison of the key features.

| Feature | Charitable Remainder Annuity Trust (CRAT) | Charitable Remainder Unitrust (CRUT) |

|---|---|---|

| Annual Payment | A fixed dollar amount set at the beginning. | A fixed percentage of the trust's annual value. |

| Payment Stability | High. Payments do not change. | Variable. Payments rise and fall with asset value. |

| Inflation Protection | None. The payment's value erodes over time. | Good. Payments can grow with the market. |

| Additional Contributions | Not allowed after initial funding. | Allowed at any time. |

| Best For | Those seeking maximum predictability and safety. | Those seeking growth potential and flexibility. |

Ultimately, this isn't a decision to tackle on your own. A knowledgeable Texas trust administration lawyer can run the numbers for you, projecting potential outcomes for both a CRAT and a CRUT based on your specific assets and goals. This expert analysis will help you select the structure that not only secures your financial future but also best fulfills your philanthropic vision.

Real-World Scenarios for Texas Families

The theory behind a charitable remainder trust is one thing, but seeing it in action is where the real understanding begins. Abstract ideas like tax deferral and income streams suddenly click when we ground them in the real problems facing Texas families. A CRT isn't just a stack of legal papers; it's a dynamic financial tool you can mold to fit specific goals, whether philanthropic or personal.

Let's walk through a few practical scenarios, from a Houston entrepreneur cashing out to a Dallas fiduciary navigating a complex estate.

The Houston Entrepreneur’s Smart Exit Strategy

Picture a Houston entrepreneur who has poured decades into her tech startup. Her initial investment has blossomed into a business worth $5 million. The catch? Her cost basis is a mere $500,000. She’s found a buyer and is ready to retire, but a straight sale means staring down a $4.5 million capital gain. That’s a tax bill so large it would claw back a huge portion of her life’s work.

So, how can she sell the company, sidestep that massive tax hit, and secure a comfortable retirement income?

This is where the CRT comes into play. Instead of selling the company herself, her Texas estate planning attorney helps her create a Charitable Remainder Unitrust (CRUT). She then transfers her company stock into this newly formed trust before the sale is finalized.

Here’s how it unfolds:

- A Tax-Free Sale: The trustee, bound by strict fiduciary duties in Texas, sells the company stock. Since the CRUT is a tax-exempt entity, the sale of the $5 million in stock triggers no immediate capital gains tax. The full amount is preserved inside the trust for reinvestment.

- A Lifetime Income Stream: She designs the trust to pay her 6% of its value every year for life. In the first year, that's a $300,000 payment. And because it's a unitrust, if the trust’s investments perform well and the principal grows, her future payments will grow right along with it.

- A Meaningful Legacy: When she passes away, the assets left in the trust will fund an endowment for a local STEM education program she's passionate about.

The result is a triple win. The entrepreneur turned an illiquid, highly appreciated asset into a growing stream of income for life. She legally bypassed an enormous capital gains tax, locked in her retirement, and funded a significant charitable gift. This is a textbook example of maximizing charitable remainder trust benefits.

The Austin Couple Downsizing Their Real Estate

Now, consider an older couple in Austin. They own a rental property they bought back in the 1980s, now worth $1.2 million. It’s become a constant headache to manage, and they’re ready to simplify their lives. They’d love to sell it to supplement their Social Security, but the looming capital gains tax has them stuck. They also have a lifelong dream of giving back to their alma mater.

Their challenge is clear: how to unlock the property's value without handing a huge slice to the IRS, all while funding their retirement and charitable goals.

Working with an attorney who specializes in asset protection, they transfer the property into a Charitable Remainder Annuity Trust (CRAT).

- The CRAT sells the property completely tax-free, allowing the full $1.2 million to be invested.

- They specifically chose a CRAT for its predictability. They set a fixed annual payout of $72,000 (a 6% annuity) for the rest of their lives.

- This fixed, reliable payment gives them tremendous peace of mind and makes retirement budgeting simple.

- After the second spouse passes, the remaining trust assets will go to their university.

By using the CRAT, the couple transformed a burdensome asset into a predictable, worry-free income they can't outlive. They also received a sizable income tax deduction upfront and fulfilled their wish to support their university—all while completely avoiding capital gains taxes on the sale.

These scenarios reveal a core strength of the CRT: it allows you to un-trap wealth locked in appreciated assets, turning it into a powerful tool for both personal financial security and leaving a lasting charitable impact.

The Dallas Fiduciary Fulfilling an Estate’s Wishes

A man in Dallas finds himself named trustee of his late aunt's estate. The estate's main asset is a large, inherited IRA. Under the SECURE Act, the IRA must be fully paid out to the non-spouse beneficiaries—her nieces and nephews—within 10 years. This would push them into higher tax brackets during their peak earning years, creating a major tax problem. His aunt also had a deep desire to support her church.

As trustee, how can he honor his aunt's charitable wishes while also managing the tax fallout for the family, all while upholding his fiduciary duty under the Texas Trust Code?

He consults a Texas trust administration lawyer and, following the will's instructions, establishes a Testamentary CRUT funded by the IRA.

- The IRA assets roll directly into the CRUT, deferring the income tax.

- The CRUT is set up to pay the nieces and nephews an annual income for 20 years—double the mandatory 10-year IRA payout window.

- This structure effectively spreads their income tax liability over two decades, making it far more manageable.

- At the end of the 20-year term, the remaining balance in the trust is distributed to the church, fulfilling his aunt's final wish.

The trustee masterfully navigated a complex situation. He honored his aunt's charitable intent, provided a tax-advantaged income stream for the family over the long term, and prudently managed the estate in full compliance with Texas law. It’s a perfect illustration of how a CRT can solve thorny issues in probate and estate settlement.

Navigating Trustee Duties and Common Pitfalls in Texas

Taking on the role of a trustee for a charitable remainder trust is no small commitment. It's a serious responsibility, one that comes with legal duties you must follow with precision and care. Whether you're a family member, a professional, or a bank, your actions are bound by the Texas Trust Code—a set of strict fiduciary principles designed to protect everyone involved.

Understanding these obligations isn't just a good idea; it's the first step toward managing the trust successfully and steering clear of costly missteps.

At the heart of a trustee's role is the duty of loyalty. This principle is non-negotiable. You must always act solely in the best interests of the trust's beneficiaries, which includes both the people receiving income now and the charity that will receive the remainder later.

This duty strictly forbids self-dealing. You can't sell trust assets to yourself or lend trust funds to your own business. Any action that even hints at a conflict of interest is off the table.

Core Fiduciary Responsibilities Under the Texas Trust Code

Beyond loyalty, the Texas Trust Code expects you to manage the trust's assets with skill and good judgment. This breaks down into several key responsibilities that a Texas trust administration lawyer can help you handle.

Your duties include:

- The Duty of Prudent Investment: You are legally required to invest and manage the trust’s money as a prudent, or sensible, investor would. This means balancing the need to generate income for the current beneficiaries with the goal of preserving the principal for the charity. A diversified portfolio is key; overly risky or speculative bets are not.

- The Duty to Account: You must keep meticulous records of every single transaction. It’s also your job to provide regular, clear financial statements to the beneficiaries. This transparency is a legal requirement that builds essential trust.

- The Duty to Make Timely Distributions: You have to make sure income payments go out to the beneficiaries on time and in the correct amount, exactly as laid out in the trust document.

Falling short on any of these duties can make a trustee personally liable for losses. To get a complete picture of the legal requirements, take a look at our detailed guide on Trustee Duties and Responsibilities in Texas.

Common Pitfalls and How to Avoid Them

Even trustees with the best intentions can find themselves in a tight spot. A major pitfall is simply not understanding the complex tax rules that govern CRTs. These trusts are incredibly tax-efficient—often sidestepping capital gains, income, and estate taxes—but those benefits hinge on strict compliance with IRC §664.

A trustee, whether in The Woodlands or San Antonio, must ensure every action upholds these rules. One wrong move could jeopardize the trust’s tax-exempt status entirely.

Another frequent mistake is improper asset management. A trustee has to perform a delicate balancing act, satisfying income beneficiaries who might want high-yield investments while also protecting the principal for the charity. This requires a solid investment strategy and a firm grasp of your fiduciary duties.

Finally, poor communication is a recipe for disaster. Keeping beneficiaries in the loop about the trust’s performance and your administrative decisions can head off misunderstandings and legal fights down the road.

Serving as a trustee is a demanding job, but with proactive legal guidance, you can fulfill your duties with confidence and make sure the trust works exactly as it was meant to.

Frequently Asked Questions About CRTs

When Texas families start exploring the world of trusts, a lot of practical questions come up. It’s a complex area, and it's only natural to want clear answers. We’ve put together some of the most common questions we hear about Charitable Remainder Trusts to help you get started.

What Is the Minimum Amount to Start a CRT in Texas?

While Texas law doesn't stamp a specific dollar amount on CRTs, practical reality sets the floor. Most financial and legal advisors will tell you a starting point of at least $100,000 to $250,000 makes sense.

Why so high? It comes down to setup and management costs. The legal fees and ongoing administrative work can quickly eat into the benefits of a smaller trust. The goal is to make sure the advantages you get from the charitable remainder trust benefits are well worth the expense.

Can I Change the Charitable Beneficiary Later?

Absolutely, and this is one of the most powerful features of a CRT. A well-drafted trust document gives the person creating it—the grantor—the right to change their mind about which charity ultimately receives the funds.

This flexibility is a huge plus. It means your philanthropic goals can evolve over time without forcing you to jump through complex legal hoops or figure out how to modify a trust in Texas through a more difficult process.

What Are the Best Assets to Fund a CRT?

The sweet spot for funding a CRT is highly appreciated assets—things that have grown significantly in value since you first acquired them. Think of assets like:

- Publicly traded stocks

- Real estate, whether it's a rental property or commercial building

- Shares in a privately held business

By placing these assets into the trust, you sidestep the immediate capital gains tax you’d otherwise face upon selling them. This keeps the full value of the asset working for you, generating income and ultimately providing a larger gift for your chosen charity.

What Happens if an Income Beneficiary Passes Away Early?

This is a crucial detail that depends entirely on how the trust was designed from the outset. If an income beneficiary dies before the trust's term is up, the document will dictate what happens next.

Typically, there are two common paths:

- Payments continue to a designated secondary beneficiary, such as a surviving spouse.

- The trust terminates ahead of schedule, and all the remaining assets are immediately passed on to the charity.

This is exactly the kind of "what if" scenario you'll want to map out carefully with your Texas estate planning attorney when you're crafting the trust.

If you’re managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process. Visit us at https://texastrustadministration.com to get started.