When a parent, grandparent, or other loved one leaves assets in trust, many families expect the process to feel orderly and calm. Instead, it often feels uncertain. You may know a trust exists, you may know someone is acting as trustee, and you may have no clear picture of what has happened to the money, property, or investments.

That uncertainty can become heavy very quickly. A beneficiary may worry that asking questions will spark conflict. A trustee may feel accused the moment a family member asks for records. In Texas, both sides need the same thing first. Clear information.

Your Guide to Financial Clarity in Texas Trusts

A common situation looks like this. A daughter knows her late father created a trust. Her uncle is now serving as trustee. Months pass. Then longer. She receives occasional updates like “everything is being handled,” but no financial details, no list of assets, and no explanation for why distributions have or have not been made.

That kind of silence makes people anxious. It also creates room for misunderstandings that could have been avoided with better communication.

In Texas, a demand for trust accounting texas is one of the most practical tools a beneficiary can use to get answers. It is not just a complaint. It is a formal request for a written accounting that shows how the trustee has managed trust property.

For many families, the accounting process brings the temperature down. Documents replace assumptions. Dates replace rumors. Transactions replace vague explanations. That is one reason basic accounting best practices for financial clarity matter so much in any setting involving fiduciary responsibility.

Why this right matters

A trust accounting can help answer the questions beneficiaries ask most often:

- What assets are in the trust

- What money came in

- What money went out

- What distributions were made

- What the trustee paid himself or herself, if anything

For trustees, the same process can be protective. Good records show that decisions were made carefully and in line with the trust terms.

A request for an accounting is not automatically an accusation of wrongdoing. In many Texas families, it is the first constructive step toward restoring confidence.

A calmer way to approach the issue

The strongest starting point is usually respectful and direct. A beneficiary can say, “I want to understand how the trust is being administered and would like a formal accounting.” That language focuses on transparency, not blame.

If you are the trustee, a measured response helps. Even when family relationships are strained, prompt and organized communication often prevents a much larger dispute later.

Understanding Your Right to a Trust Accounting

Texas trust law treats a trustee as a fiduciary. That means the trustee must act in the interests of the beneficiaries, manage trust property responsibly, and keep proper records. A fiduciary role is not casual. It carries legal duties.

One of the most important practical effects of that duty is the beneficiary’s right to ask for information. Under Texas law, that right is broad. Every beneficiary is entitled to demand a trust accounting, although trustees are generally not required to provide one more often than once every 12 months, as discussed in this explanation of beneficiary rights under Texas trust administration and the related discussion at Ford + Bergner on when you are entitled to a trust accounting.

What fiduciary duty means in plain English

A fiduciary duty usually includes a few basic expectations:

- Loyalty: The trustee should act for the trust’s benefit, not personal convenience.

- Prudence: The trustee should manage assets with care.

- Honesty in records: The trustee should keep accurate financial information.

- Fair dealing: The trustee should treat beneficiaries according to the trust terms.

When beneficiaries do not receive information for a long period, they often start to wonder whether those duties are being met. Sometimes the trustee is doing everything properly but communicating badly. Sometimes there is a real problem. The accounting helps separate one from the other.

Who can ask for an accounting

In most discussions, the person making the request is a beneficiary. That may include someone currently receiving distributions or someone with a future interest under the trust. Families often get confused here because not every person connected to the trust has the same rights at the same time.

A few examples help:

- A son named in the trust as a remainder beneficiary may have standing to ask for an accounting.

- A current income beneficiary usually has a strong reason to ask for one if distributions affect monthly support.

- A family member who only suspects the trust exists, but cannot show a legal interest, may need legal help first to confirm status.

When people usually make the request

Many accounting demands arise after a shift in family or trust administration. For example:

A new trustee takes over

If one trustee resigns, dies, or is removed, beneficiaries often want a financial snapshot. That request is reasonable. It helps everyone understand what the new trustee received and what condition the trust was in at the time of transition.

Communication has gone quiet

Long periods without reports, calls, or explanations often trigger concern. A beneficiary may not know whether trust real estate was sold, whether investments changed, or whether expenses were paid from trust funds.

A major life event changes the stakes

A beneficiary may face medical costs, job loss, disability, divorce, or another financial disruption. That can increase the urgency of understanding whether the trust permits distributions and whether funds are available.

Beneficiaries often hesitate because they do not want to look ungrateful or aggressive. Texas law does not require silence. It recognizes that transparency is part of trust administration.

The 12 month rule causes real confusion

Many people get tripped up here. Texas law gives beneficiaries a broad right to demand an accounting, but trustees generally do not have to produce one more often than once in a 12 month period.

That does not mean a trustee can ignore legitimate concerns forever. It means timing matters. If a trustee provided a proper accounting recently, another formal demand too soon may be refused on that ground.

For that reason, a beneficiary should pause before sending a letter in anger. First ask:

- When was the last formal accounting provided?

- Was it complete, or just an informal summary?

- Do the trust terms require more frequent reporting?

- Are there urgent concerns that might justify seeking court involvement?

A careful request made at the right time is much more effective than a rushed one.

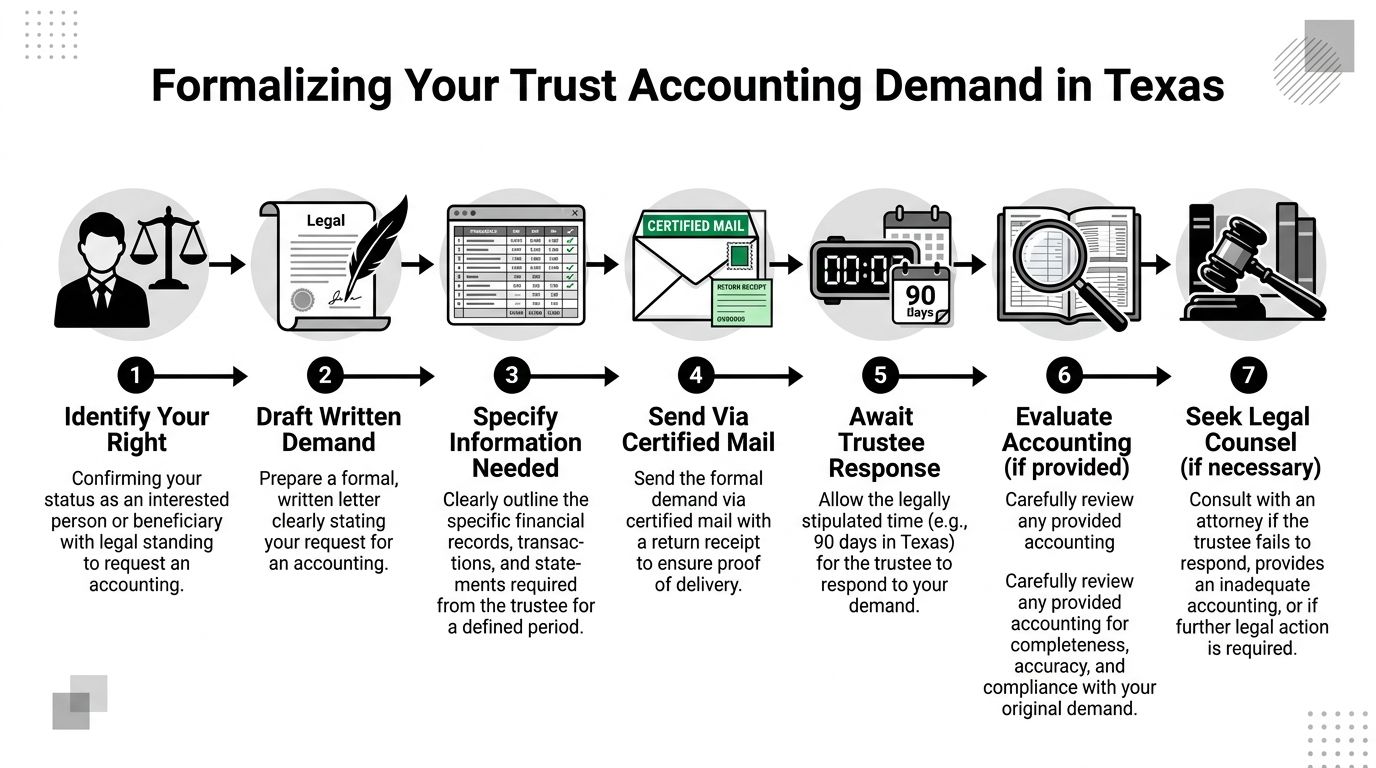

How to Formally Demand an Accounting in Texas

A phone call can help open the door. It does not create the same legal record as a written demand. If you are serious about a demand for trust accounting texas, put it in writing.

Texas law gives this step real force. Texas Trust Code Section 113.151 establishes a 90 day deadline for trustee compliance with a beneficiary’s accounting demand. If the trustee does not comply within that period, the beneficiary gains the right to file suit to compel the accounting, as described in this trust accounting analysis.

Start with a written letter, not a casual message

Email may be useful, but a formal letter is stronger. Certified mail with return receipt requested creates proof of delivery. That matters if the trustee later says, “I never received it.”

A good written demand usually includes:

- Your full name and contact information

- Your relationship to the trust

- Enough information to identify the trust

- A clear statement that you are requesting a formal trust accounting

- The period you want covered, if appropriate

- A polite request for delivery in writing

- The date and your signature

Keep the tone firm but not hostile

Some letters fail because the writer turns the request into a list of accusations. That often causes the trustee to become defensive, and it may distract from the central issue.

A better approach sounds like this:

“I am a beneficiary of the trust and request a formal written accounting of the trust’s administration. Please provide the accounting in writing for the appropriate period under Texas law. I would also appreciate confirmation that you received this request.”

That wording is clear. It preserves your position without escalating the conflict.

A sample demand letter

You can adapt language like this:

[Your Name]

[Your Address]

[City, State, Zip]

[Date]

Via Certified Mail

[Trustee Name]

[Trustee Address]

Re: Request for Trust Accounting

Dear [Trustee Name],

I am a beneficiary of the [name of trust, if known]. I am writing to formally request a written trust accounting under Texas law.

Please provide a formal accounting for the trust administration covering the period that is appropriate based on the last accounting provided, if any. If you believe a prior accounting affects the period covered by this request, please identify the date of that accounting in your response.

Please send the accounting to me at the address listed above. If you prefer, you may also send a copy by email to [your email].

Thank you for your attention to this matter. I hope we can address this request cooperatively and with full transparency.

Sincerely,

[Your Name]

Practical choices that reduce conflict

A beneficiary can make the process smoother by adding a short note like, “My goal is to understand the trust records and avoid unnecessary conflict.” That simple sentence sometimes changes the trustee’s response.

Trustees can also respond strategically. If full production will take time, acknowledge receipt promptly and give a reasonable timeline. Silence is usually the worst option.

What beneficiaries should do before sending the letter

- Check prior records: Look for old accountings, letters, or trust summaries.

- Confirm trustee details: Use the correct legal name and mailing address.

- Save copies: Keep a signed copy of the letter and mailing receipt.

- Stay specific: Ask for a formal accounting, not “everything related to the trust.”

What trustees should do after receiving the letter

- Preserve records: Gather statements, ledgers, receipts, and trust documents.

- Review timing: Determine whether the request falls within the usual 12 month limitation.

- Avoid informal shortcuts: A loose spreadsheet or vague summary may not solve the problem.

- Consult counsel early: If there is confusion about scope, timing, or content, legal advice can help before positions harden.

The moment a written demand arrives, treat it as a legal event, not a family squabble. That mindset alone prevents many mistakes.

Why certified mail still matters

People sometimes ask whether certified mail is old-fashioned. Maybe. It is also effective. It gives you a paper trail that can be shown to a court if necessary.

In trust disputes, memory is unreliable. Records are better.

What a Proper Texas Trust Accounting Includes

Not every packet of documents counts as a proper accounting. Beneficiaries often receive a few bank statements, a one-page summary, or a short email that says the trust is “in good shape.” That may be information, but it is not always a legally sufficient accounting.

Some analyses note that informal summaries rarely satisfy a trustee’s full duty to inform and account, which is one reason accounting disputes arise so often. That issue is discussed in this review of Texas trust and estate accounting disputes.

The difference between a summary and an accounting

A summary tends to be broad and reassuring. A proper accounting should be detailed enough that a beneficiary can follow what happened with trust property.

If you receive records and still cannot answer basic questions like “What assets started in the trust?” or “Why was this payment made?” the accounting may be incomplete.

Required components of a formal Texas trust accounting

For a fuller discussion of trust accounting concepts, this resource on what is trust accounting can help.

| Component | What It Shows |

|---|---|

| Statement of trust property | What the trust owns or owned during the accounting period |

| Receipts | Money or property that came into the trust |

| Disbursements | Money paid out by the trust |

| Distributions to beneficiaries | What beneficiaries received and when |

| Liabilities and expenses | Debts, obligations, or costs charged to the trust |

| Trustee compensation | Fees or compensation paid to the trustee |

How to review the accounting like a careful reader

You do not need to be an accountant to spot issues. Start with common-sense questions.

Look at the opening and closing picture

Does the accounting show what the trust had at the beginning and what it had at the end? If not, it is hard to tell whether assets disappeared, were sold, or were transferred appropriately.

Follow the money in and out

Read the receipts and disbursements carefully. Ask yourself:

- Does each entry have enough detail to make sense?

- Are there large expenses with no explanation?

- Are repeated payments going to the same person or business?

- Do any payments appear personal rather than trust-related?

Check distributions against the trust terms

If beneficiaries were supposed to receive support, health, education, or maintenance distributions, do the records reflect that? If one beneficiary received funds and another did not, there may be a valid reason, but the records should support it.

Review trustee compensation closely

Trustees are often entitled to compensation, but beneficiaries should still review those entries. Questions to ask include whether the fee appears documented, consistent, and tied to actual administration.

A clean accounting should allow a reasonable beneficiary to understand what happened without guessing at missing pieces.

Red flags that deserve a second look

Some warning signs show up again and again:

- Missing asset details

- Unexplained transfers

- Large cash withdrawals

- Expenses labeled too vaguely to understand

- Trustee fees without backup

- Sales of property with little supporting information

- Transactions that appear to benefit the trustee personally

One unusual entry does not automatically prove misconduct. But a pattern of vague entries, missing support, and resistance to questions should not be ignored.

If the accounting is detailed, organized, and supported by records, that often helps everyone move forward. If it is confusing, selective, or incomplete, more follow-up may be necessary.

Navigating Common Hurdles and Trustee Responses

Even when a beneficiary makes a careful request, the response is not always simple. Trustees may delay, push back, or send something that looks official but answers very little.

One of the biggest sticking points is timing. Texas Property Code § 113.151(a) states that trustees are not obligated to account more frequently than once every 12 months, which can leave beneficiaries frustrated when they have urgent concerns. You can review that rule directly in Texas Property Code section 113.151 and see related practical discussion in this page about a trustee refusing to provide accounting in Texas.

When the trustee says no because of the 12 month rule

This is not always bad faith. Sometimes the trustee recently gave a proper accounting and is within the legal protection against repeated demands.

Still, beneficiaries should look carefully at what was provided. A trustee may call something an accounting when it was really just a summary or update. The label matters less than the content.

A useful response can be:

“If you are declining my request based on a prior accounting, please identify the date of that accounting and provide a copy if I do not already have it.”

That keeps the conversation factual.

When the trustee ignores the request

Silence creates more tension than almost any other response. If the trustee does not acknowledge the letter, a follow-up should be short and professional.

For example:

- First follow-up: Confirm the date the written demand was delivered and request acknowledgment.

- Second follow-up: Ask whether the trustee intends to provide a formal accounting.

- Final pre-lawyer message: State that you are trying to resolve the matter without court involvement.

This sequence shows patience without giving up your rights.

When the accounting is confusing

Some accountings are technically large but practically useless. They may contain stacks of statements with no organization. Or they may omit explanation for major items.

A beneficiary should avoid sending an emotional list of grievances. A better method is to ask numbered questions tied to specific entries:

- Please explain the payment made on [date] to [payee].

- Please identify the property sold during the period and provide sale details.

- Please explain the basis for trustee compensation shown on [entry].

That style is easier to answer and harder to dismiss.

Communication strategies that calm conflict

The way you ask can affect the outcome. In many trust disputes, the issue is not only law. It is family history, grief, and suspicion.

Use neutral words

Instead of “You stole money,” say, “I do not understand this transaction and need documentation.”

Instead of “You are hiding things,” say, “The records provided do not fully answer these questions.”

Focus on documents, not motives

You may strongly suspect misconduct. Even so, accusations made too early can shut down productive communication. Lead with the records.

Keep a timeline

Create a simple list of dates:

| Date | Event |

|---|---|

| [Date] | Written demand sent |

| [Date] | Certified mail delivered |

| [Date] | Trustee responded or failed to respond |

| [Date] | Follow-up sent |

This helps if the matter later goes to counsel or court.

What trustees can do to lower the temperature

Trustees are often family members with little formal training. If you are serving in that role, do not assume that defensiveness will protect you.

Helpful responses include:

- Acknowledging the request promptly

- Explaining whether a prior accounting affects timing

- Producing organized records rather than piecemeal messages

- Asking counsel to help prepare a formal response if needed

The more complete and orderly the disclosure, the more likely the matter can be resolved without a judge deciding what happens next.

When to Escalate and Hire a Texas Trust Attorney

Some trust accounting disputes can be resolved with one well-written letter and a professional response. Others cannot. When key warning signs appear, legal help becomes less of an option and more of a safeguard.

One reason is practical. Benchmarks from fiduciary litigators indicate that about 70% of trust accounting disputes are resolved before litigation when beneficiaries and trustees engage in proactive, detailed disclosures, often with legal counsel involved. That means a lawyer often helps the parties resolve the issue before a courtroom fight becomes necessary.

Red flags that justify immediate legal advice

A beneficiary should strongly consider speaking with a Texas trust administration lawyer if any of these are happening:

- The trustee does not respond in a meaningful way after a formal demand

- The accounting contains transactions that look like self-dealing

- Required distributions appear to be withheld without explanation

- Records are missing, contradictory, or obviously incomplete

- The trustee becomes hostile and refuses reasonable questions

- Trust property appears to have been transferred for the trustee’s personal benefit

A trustee should also seek counsel if the records are disorganized, the trust terms are unclear, or family conflict is making communication difficult. Waiting usually makes things harder.

What it means to compel an accounting

A lawsuit to compel an accounting asks the court to order the trustee to produce the information required by law. In some cases, that is the only relief sought at the beginning. In others, the accounting becomes the doorway to larger claims involving breach of trust, improper distributions, or removal of the trustee.

Legal analysis matters here. A lawyer can review the trust document, evaluate whether the accounting is sufficient, and determine whether the problem is delay, poor recordkeeping, or actual misconduct.

Why counsel changes the dynamic

When a lawyer gets involved, the conversation often becomes more disciplined. Deadlines are tracked. Requests are narrowed. Responses are judged against legal requirements, not family narratives.

For some families, that structure is enough to stop the spiral. Options may include a trust accounting review, a demand letter from counsel, negotiation over supplemental records, or court action if needed. A Texas estate planning attorney or trust dispute lawyer can also coordinate with accountants or financial professionals when the paper trail is dense.

If you are trying to protect an inheritance, carry out fiduciary duties in Texas, or understand whether court action is necessary, legal guidance helps you make decisions from a position of clarity rather than stress.

Take the Next Step with Confidence

A trust accounting request is about clarity. For beneficiaries, it can answer long-standing questions and protect against hidden problems. For trustees, it can document good faith administration and reduce suspicion.

The most effective approach is usually steady and organized. Make the request in writing. Keep your tone professional. Review the response carefully. If the process breaks down, do not ignore the warning signs.

Trust administration does not happen in a vacuum. It often overlaps with probate, estate planning, guardianship concerns, and asset protection decisions for the wider family. If you need broader guidance on trust administration, probate, guardianship, estate planning, or how to protect family assets in Texas, those issues should be evaluated together rather than one at a time.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.