Managing a loved one’s trust can feel overwhelming when the trustee stops answering questions or refuses to share records. For many Texas families, that silence is more than frustrating. It creates real fear about whether the trust is being handled properly.

If you are dealing with a trustee refusing to provide accounting texas, the good news is that Texas law does not treat an accounting as a courtesy. It treats it as part of the trustee’s job. Beneficiaries have enforceable rights, and courts have tools to make trustees comply.

The practical question is not whether you should keep asking informally. It is how to move from uncertainty to a clear, documented process that protects your inheritance and puts the burden where it belongs, on the trustee.

Your Rights as a Beneficiary to a Trust Accounting in Texas

A trustee holds property for someone else’s benefit. That role comes with fiduciary duties in Texas, including the duty to keep accurate records and disclose information that beneficiaries are entitled to receive.

A proper trust accounting is not a vague summary. It should show what came into the trust, what went out, what the trust owns, what it owes, and what compensation the trustee has taken.

What Texas law requires

Under Texas Property Code § 113.152, trustees must provide annual accountings beginning within 12 months of trust creation or acceptance, and those accountings must cover receipts, disbursements, assets, liabilities, and trustee compensation, as discussed in this Texas trust accounting overview and described in the Texas CPA discussion of trustee accounting duties.

That matters for two reasons.

First, it means the trustee should be maintaining records in a form that can be produced. Second, refusal can have consequences beyond a court order. The same source explains that refusal upon demand can expose a trustee to remedies under § 114.008(a), including personal liability for trust losses or denial of compensation.

What beneficiaries are entitled to see

In plain English, beneficiaries want answers to a short list of practical questions:

- What assets are in the trust now

- What income has the trust received

- What expenses have been paid

- What distributions have been made and to whom

- What fees the trustee has taken

- Whether trust property has been sold, transferred, or retitled

Those details matter because many trust disputes begin with small warning signs. A trustee delays. Explanations get shorter. Financial details become harder to pin down. By the time a beneficiary realizes there is a serious issue, records may already be incomplete.

If a trustee responds with broad assurances but no numbers, no transaction history, and no supporting records, that is usually not a meaningful accounting.

What works and what does not

Informal requests can be useful at the start, particularly in a family trust where everyone is trying to stay civil. A polite email sometimes solves the problem.

But informal requests fail for a simple reason. They create no clean deadline and no strong proof. If the trustee is disorganized, evasive, or hiding mistakes, a casual request gives them room to stall.

A beneficiary should think in terms of documentation, not emotion. You do not need to accuse the trustee of theft to insist on transparency. You only need to know that Texas law expects trustees to account for their administration.

A common real-world example

A daughter is a beneficiary of her late father’s trust. Her uncle is trustee. At first, he says he is “still getting the paperwork together.” Months pass. Then he says the trust is “too complicated” and that she should just trust him.

That response misses the point. Trustees are chosen to do the work. Beneficiaries are not required to accept silence because the administration is uncomfortable, time-consuming, or family-sensitive.

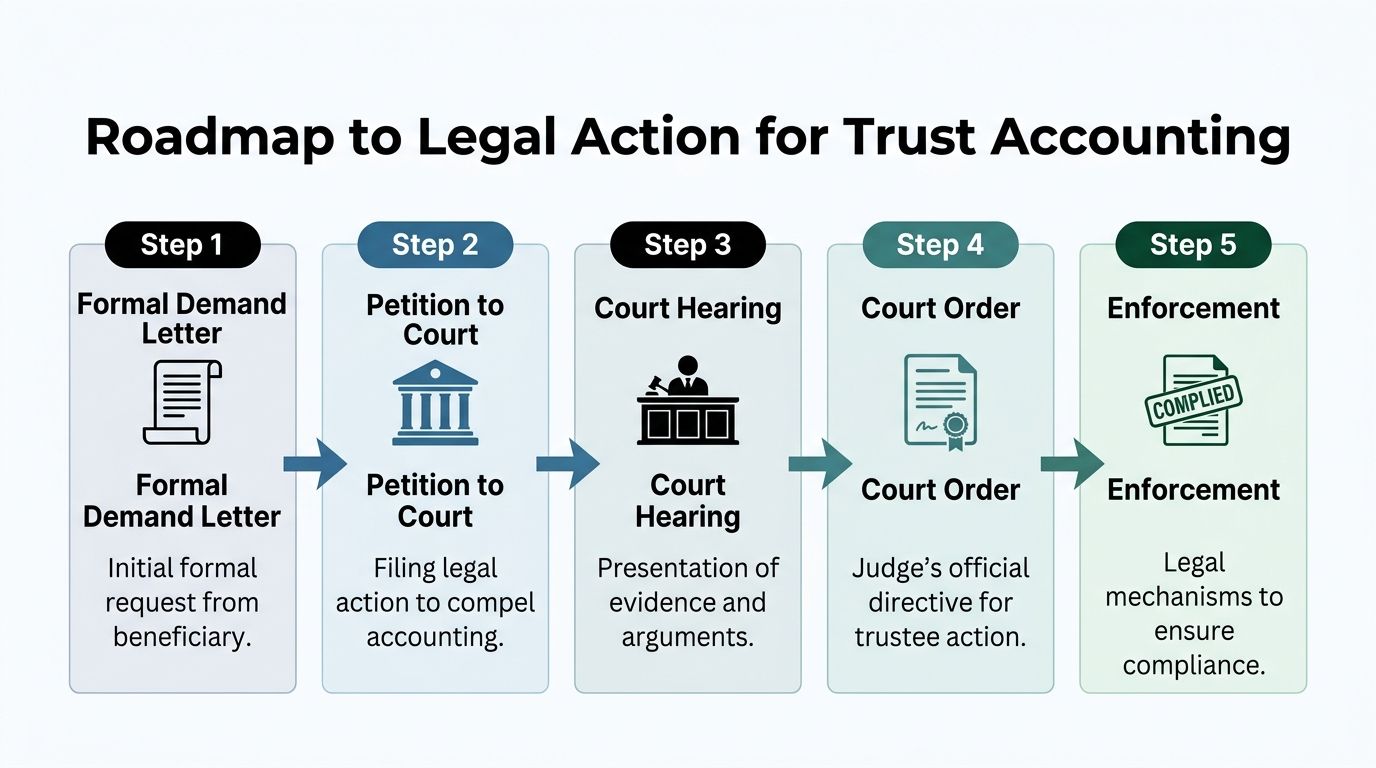

How to Formally Demand a Trust Accounting

Once a trustee stops cooperating, the next move should be deliberate. A proper demand letter changes the situation from a family disagreement into a legal record.

Under Texas Property Code § 113.151(a), a beneficiary can make a written demand for an accounting, and the trustee must deliver it on or before the 90th day after receiving the demand. If the trustee does not comply within that window, the beneficiary may file suit to compel delivery, as stated in Texas Property Code § 113.151.

Send a demand that can be proven

The biggest mistake beneficiaries make is relying on phone calls or loose email chains. If the matter ends up in court, the judge will care about proof.

Use a written demand that clearly identifies:

- Your status as beneficiary

- The trust’s name, if known

- A direct request for a full accounting

- The date of the request

- A delivery method that shows receipt

Certified mail is the safest practical choice because it creates a paper trail. If you also send the letter by email, keep that copy too. The goal is simple. Remove any later argument that the trustee never received your demand.

Sample language for a demand letter

You do not need dramatic language. Precision works better than outrage.

Dear Trustee,

I am a beneficiary of the trust and hereby demand a full written accounting of the trust under Texas Property Code § 113.151. Please provide a detailed accounting of all trust transactions since the last accounting, or since the creation of the trust if no prior accounting has been provided. This accounting should include trust assets, liabilities, receipts, disbursements, distributions, and trustee compensation. Please deliver the accounting within the time required by Texas law.

That kind of letter does three things well. It identifies the legal basis, defines the scope, and avoids unnecessary accusations.

Keep a clean file from the start

Create a folder, digital or paper, and keep every relevant item in it.

Include:

- The demand letter with the date you signed it

- Certified mail receipt and delivery confirmation

- Emails or texts from the trustee

- Prior account statements or partial reports

- A timeline of missed responses or shifting explanations

This file becomes important if you later ask a probate court to intervene.

What helps and what hurts

A demand letter works best when it is calm and exact. It works poorly when it becomes a running argument about family history.

A few practical tips:

- Do not overload the letter: A long complaint about old grievances can distract from the request.

- Do not threaten everything at once: Demanding removal, damages, and criminal consequences in the first letter produces more resistance, not more disclosure.

- Do not guess at wrongdoing: Ask for records first. Let the accounting tell the story.

A strong demand letter is not the loudest letter. It is the one a judge can read later and immediately understand.

If the trustee offers a partial response

A trustee sometimes sends a spreadsheet with a few balances and expects that to end the issue. They sometimes provide bank statements but no explanation of distributions, fees, or asset transfers.

That may not be enough. An accounting should be detailed enough to let a beneficiary evaluate administration, not just glance at a balance. If the response is incomplete, preserve it and assess whether it answers the actual request.

Many beneficiaries pause too long at this stage. They assume any response counts as compliance. In practice, an evasive half-answer can be another form of refusal.

Taking Legal Action When a Trustee Ignores Your Demand

When the deadline passes and the trustee still has not produced a real accounting, the dispute enters a different phase. At that point, the issue is no longer whether the trustee “needs more time.” The issue is whether the court should compel compliance.

A beneficiary’s most direct tool is a court petition or motion to compel an accounting. In many cases, this is the cleanest way to force the matter into a formal process with deadlines, evidence, and consequences.

What a motion to compel does

The phrase sounds technical, but the concept is straightforward. You ask the court to order the trustee to produce the accounting the law requires.

The judge is not being asked to speculate about trust mismanagement at that stage. The immediate issue is narrower. Did the beneficiary make a proper demand, and did the trustee fail to comply?

That narrow focus is useful. It lets beneficiaries move forward without having to prove every underlying problem before seeing the records.

The evidence that matters most

In these cases, clean documentation matters more than emotional testimony. Courts want to see an orderly sequence.

A strong file includes:

- The written demand

- Proof of receipt

- The trustee’s response, if any

- A copy of the trust, if available

- Any prior accountings or missing records

- A short chronology of events

If you walk into court with that record, the issue becomes much easier to present. If you walk in with only verbal complaints, the trustee has more room to argue.

Why recordkeeping failures hurt trustees

When a trustee fails to maintain proper records after a demand, the Restatement (Third) of Trusts allows courts to resolve doubts against the trustee, shifting the burden to the trustee to prove legitimacy, and Texas Property Code § 114.008(a) authorizes courts to order a trustee’s estate to bear the costs of corrective accounting procedures, as discussed in this analysis of trustee duties when records are missing or a trustee dies or becomes incapacitated.

That is an important practical point. Trustees assume that if records are messy enough, beneficiaries will give up. Texas trust law points the other direction. Poor records can become the trustee’s problem, not the beneficiary’s.

If the trustee cannot explain the money because the trustee failed to keep records, that does not help the trustee in court.

What court intervention looks like in practice

In a typical case, the beneficiary files in the appropriate court, serves the trustee, and asks for an order compelling an accounting. The trustee then has to respond in a forum where delay is harder to sustain.

The filing itself can change the dynamic. A trustee who ignored months of requests hires counsel and produces documents. That does not mean the case was unnecessary. It means the legal pressure worked.

Other times, the trustee fights. That happens when the missing accounting would reveal self-dealing, poor investment oversight, improper distributions, or simple neglect.

What beneficiaries get wrong at this stage

Three mistakes show up.

One is waiting too long after the deadline. Delay can give the trustee more time to reshape records or transfer blame.

Another is filing without a focused request. If the petition tries to cover every possible complaint before the accounting is obtained, the case can become more complicated than it needs to be.

The third is treating the accounting dispute as only a paperwork issue. It is sometimes. It is sometimes the first visible sign of deeper fiduciary problems. A careful legal review can help decide whether to keep the request narrow or seek broader relief.

A short decision guide

| Situation | Practical next step |

|---|---|

| Trustee ignores the written demand entirely | File to compel accounting |

| Trustee sends a vague summary only | Evaluate whether the response is incomplete and seek court relief if needed |

| Trustee claims records are unavailable | Preserve that statement and prepare for a stronger court response |

| Trustee becomes hostile after demand | Shift communication to writing and involve counsel |

In larger metro courts such as Houston, Dallas, and Austin, judges expect trust disputes to be presented clearly and efficiently. A concise filing backed by organized exhibits works better than a broad, emotional attack.

Advanced Remedies Trustee Removal and Surcharge Actions

Some cases start with missing paperwork and end with evidence of real harm to the trust. When that happens, asking only for an accounting may not be enough. The court can do more.

A trustee who refuses to account may also face a surcharge, removal, loss of compensation, or an order shifting fees and costs. Those remedies exist because an accounting is not just a reporting duty. It is one way the law checks misuse of another person’s property.

When removal becomes the right remedy

Removal is a serious request. Courts do not remove trustees just because communication has been unpleasant.

But removal becomes a strong option when the refusal to account is part of a broader pattern, such as:

- Using trust funds for personal expenses

- Ignoring beneficiary rights for extended periods

- Failing to separate trust property from personal property

- Blocking disclosure while making unexplained transfers

- Creating conflict that makes administration unworkable

In those situations, leaving the trustee in place can expose the trust to further risk. Beneficiaries hesitate because the trustee is a parent, sibling, or family friend. That is understandable. Still, the court’s concern is administration, not family title.

What a surcharge action means

A surcharge is a claim that the trustee should personally restore losses caused by breach of duty. If trust money went missing, if assets were mishandled, or if avoidable expenses piled up because the trustee ignored obligations, a surcharge can put financial responsibility where it belongs.

The accounting often matters most in this situation. Once records are finally produced, they may reveal transactions that should never have happened. Or they may confirm that the trustee cannot document what happened at all.

That is also why early record requests matter. The accounting is often the doorway to proving the larger case.

For readers dealing with a trustee whose conduct appears to go beyond delay, this overview of a petition to remove trustee in Texas is a useful starting point.

Why these remedies change settlement posture

Once the case includes possible removal, surcharge, denied compensation, and fee exposure, the dynamic changes.

That shift matters in negotiations. A trustee who was dismissive during informal family discussions may become more realistic when faced with personal consequences.

This discussion gives a practical overview of how courts look at trustee accountability:

A practical caution for beneficiaries

Advanced remedies are powerful, but they should be pursued with discipline. Overreaching can distract from a strong claim. If the primary issue is incomplete reporting, lead with that. If the records then show self-dealing or loss, expand the case based on evidence, not suspicion.

The best removal and surcharge cases are built from documents, timelines, and transactions. They are not built from guesswork.

Handling Common Defenses and Complex Scenarios

Trustees who refuse to account rely on familiar explanations. Some are based on confusion. Some are delay tactics. Some are attempts to make beneficiaries doubt themselves.

The challenge is that trust disputes rarely stay simple. One trustee may die. A successor trustee may step in with little information. Co-trustees may blame each other. Families in Houston, Dallas, Austin, or The Woodlands may also be trying to manage business interests, real estate, and strained relationships at the same time.

The trust waived accountings

A trustee may say, “The trust says I do not have to provide an accounting.”

That argument is overstated. Texas law protects core fiduciary duties, and accounting disputes do not disappear just because the trust uses broad waiver language. If facts suggest a breach of trust, courts can still be asked to intervene.

The practical takeaway is simple. Do not accept “the document says I do not have to tell you anything” at face value. That statement needs legal review.

It is too complicated or too expensive

This comes up in trusts holding rental property, family businesses, mineral interests, or mixed investment accounts.

Complexity is not a defense to silence. It may explain why a careful accounting takes work, but trustees accept the job with its burdens. If the accounting requires a CPA, bookkeeping cleanup, or legal support, the trustee is expected to deal with that responsibly.

A court is less sympathetic when the trustee uses complexity as a reason to provide nothing.

I already gave you enough information

Consider a mini-scenario.

A beneficiary in Dallas receives two years of bank statements and a short note from the trustee saying, “This should answer your questions.” It does not show who received distributions, why certain checks were written, whether compensation was taken, or what assets remain.

That is the point where disputes deepen. The trustee frames the beneficiary as unreasonable, but a core problem is that raw records without explanation may not function as a proper accounting.

When the trustee has died or become incapacitated

This is one of the most misunderstood situations.

If the acting trustee dies or becomes incapacitated without providing an accounting, the problem does not vanish. Under Texas Property Code § 113.151(b), interested parties such as beneficiaries or successor trustees may petition the court directly for an accounting from the former trustee, and courts may order the former trustee’s estate to prepare it at the estate’s expense under § 114.008(a), as discussed in this analysis of who has the duty to prepare an accounting when the trustee dies or becomes incapacitated.

That matters because successor trustees inherit a mess they did not create.

The successor trustee problem

A successor trustee may know little about prior transactions. Beneficiaries then look to the new trustee for answers, while the new trustee lacks records, passwords, statements, or tax support.

In practice, the successor trustee needs to do several things quickly:

- Secure current trust assets

- Identify what records exist and what is missing

- Request records from banks, advisors, and prior professionals

- Assess whether a court petition is needed against the former trustee or estate

- Avoid guessing in communications with beneficiaries

A successor trustee should not cover for a predecessor’s failures. That can create new liability.

If you become successor trustee and discover missing records, document the gap immediately and act to obtain the prior accounting. Silence can become your problem next.

Co-trustee disputes are different

Now consider another scenario.

Two brothers serve as co-trustees in Austin. One wants to provide a full accounting. The other refuses and says no records should leave his office. Beneficiaries get mixed messages and assume both are hiding something.

Co-trustee disputes are harder because responsibility is shared, but not always equally in practice. One co-trustee may be controlling the books, the mail, the tax returns, or the relationship with the financial advisor. The other may be passive, overwhelmed, or conflict-averse.

That does not make the problem smaller. It usually means the record has to be built more carefully.

Useful steps include:

- Review the trust document for any special co-trustee procedures.

- Demand the accounting in writing from all serving co-trustees.

- Preserve separate responses if one cooperates and the other obstructs.

- Avoid relying on informal family meetings to resolve a deadlock that affects legal duties.

Self-help in co-trustee cases can backfire. A rushed filing that does not identify who controls the records, who failed to act, and what relief is sought can weaken an otherwise valid complaint.

Local practice realities

In larger Texas courts, judges tend to respond well to organized facts and poorly to family drama presented as a substitute for evidence. That is especially true when multiple fiduciaries are involved.

If the case includes a deceased trustee, a successor trustee, and disputed records across several institutions, careful pleading matters. These are not cases to improvise.

Why You Need a Texas Trust Administration Lawyer

The legal rights are clear on paper. The hard part is converting those rights into action when a trustee resists, delays, or turns the dispute into a family battle.

That is where a Texas trust administration lawyer adds value. The job is not just filing paperwork. It is building a record, choosing the right remedy, and avoiding missteps that give the trustee room to escape accountability.

The point where self-help usually stops working

A beneficiary can send the initial written demand without counsel. After that, the risks rise quickly.

If the trustee ignores the demand, produces a partial response, claims the trust waives disclosure, or suggests records are unavailable, the dispute has become legal, not clerical. The same is true when the trust owns closely held business interests, real property in multiple counties, or accounts that require subpoenas and coordinated follow-up.

In those situations, a lawyer helps decide whether to seek only an accounting or to combine that request with removal, surcharge, fee recovery, or other relief.

Why local court practice matters

Houston, Dallas, and Austin courts all apply Texas law, but judges and clerks expect trust disputes to be presented in a disciplined way. Pleadings, service issues, exhibit organization, and hearing preparation all affect momentum.

A lawyer who regularly handles trust disputes can spot problems early, including:

- Missing proof of demand receipt

- An incomplete trust document

- Confusion over who the current trustee is

- A need to involve a former trustee or estate

- A co-trustee structure that changes the strategy

For families already dealing with probate, incapacity issues, or elder care concerns, it also helps to work with counsel who understands related areas like estate planning, guardianship, and asset protection.

Good legal work is also operational work

Modern trust litigation is document-heavy. Lawyers now rely on organized workflows, secure client communication, and technology tools that help review records more efficiently. For readers interested in how the profession is adapting, this overview of AI tools for lawyers offers helpful context on the kinds of systems legal teams use to manage large document sets and recurring analysis.

That does not replace judgment. It supports it.

When the dispute is active, what matters most is legal strategy, evidentiary discipline, and a clear understanding of fiduciary duties in Texas. If you are at the point where a trustee is refusing transparency, this resource on working with a trust administration attorney in Texas is a practical next read.

Take Control of Your Legacy with Trusted Legal Guidance

When a trustee withholds an accounting, beneficiaries feel stuck between patience and confrontation. Texas law gives you a better path. You can demand transparency, document noncompliance, and ask the court to step in when necessary.

The key is acting with structure. Keep the demand formal. Preserve proof. Treat missing records as a legal issue, not a family misunderstanding that will somehow fix itself.

This is especially important when the case involves a successor trustee, a deceased trustee, co-trustees in conflict, or signs of deeper financial misconduct. In those cases, prompt legal guidance can protect both the trust and the people it was meant to help.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.