Skip to content

Skip to content Managing a loved one's trust can feel overwhelming, but with the right legal guidance, it doesn't have to be.

Many Texas couples are in the same position right now. They signed estate planning documents years ago, put them in a safe place, and assumed the plan would still fit their family when the time came. Then life changed. Tax laws changed. Their children became adults. Some families blended. Some built businesses. Others want less complexity for the spouse who may someday be left handling everything alone.

That's where the conversation about a bypass trust in Texas becomes so important. For some families, it still serves a real purpose. For many others, especially families with moderate wealth, an older bypass trust can create unnecessary restrictions, administration, and even income tax headaches.

Estate planning today isn't just about houses, bank accounts, and beneficiary forms. It also includes online accounts, passwords, cloud storage, and other important digital estate considerations that families often overlook until it's too late.

Securing Your Family's Future in Texas

A bypass trust grew out of a very specific estate tax problem. Years ago, married couples often needed a special structure to make sure both spouses' federal estate tax exemptions were used. Without that structure, a family could lose one spouse's exemption and expose more property to tax later.

That history matters because many Texans still have documents built for an older tax world.

Today, the better question usually isn't, “Can we create a bypass trust?” It's, “Should we still use one?” That's a different conversation, and it calls for a modern review of your will, trust, assets, and family goals.

Why families get confused

Most people hear the words “trust,” “tax savings,” and “asset protection” and assume more trust planning must be better. But a bypass trust is not a simple holding account. It becomes legally separate and far less flexible after the first spouse dies. That can be useful in the right case. It can also become a burden if the estate never had a realistic federal estate tax problem to begin with.

A common Texas example looks like this:

- A married couple signed an A/B trust years ago and haven't reviewed it since.

- Their estate is valuable but not ultra-high-net-worth, and their main goals are simplicity, family harmony, and avoiding probate delays.

- Their trust requires a bypass trust automatically at the first death, even if that structure no longer makes practical sense.

- The surviving spouse ends up with less flexibility than the couple intended.

A good estate plan should fit your family as it is now, not your family as it looked a decade or two ago.

Texas families also need to think beyond tax language. The Texas Trust Code, Texas Estates Code, and core fiduciary rules shape how trusts are administered after death, how trustees must behave, and what rights beneficiaries have to information and fair treatment. Those rules matter just as much as tax strategy.

What Is a Bypass Trust

A bypass trust, also called a credit shelter trust or B trust, is an irrevocable estate planning tool used to help married couples use both spouses' estate tax exclusions. According to this explanation of bypass trusts, as of 2026, the federal estate tax exemption is projected to be around $13.99 million per person, meaning a couple can potentially shield nearly $28 million from federal estate taxes using this and other strategies.

That's the legal definition. Here's the plain-English version.

Think of it as two tax buckets

Imagine a married couple has two large tax-free buckets. Federal law gives each spouse their own bucket. A bypass trust was designed to make sure the first spouse's bucket doesn't get wasted when that spouse dies.

Instead of leaving everything outright to the surviving spouse, part of the deceased spouse's property goes into a separate trust. That trust is no longer owned by the survivor in the usual sense. Because of that separation, those assets can stay outside the surviving spouse's taxable estate.

The basic idea is simple:

- First spouse dies

- Some assets move into the bypass trust

- The surviving spouse may still benefit from the trust

- The remaining trust property later passes to children or other beneficiaries

Why irrevocable matters

The word irrevocable is the key. Once funded, the bypass trust generally can't be changed the way a revocable living trust can. That loss of flexibility is what creates the legal separation that estate tax planning depends on.

For families trying to understand the broader range of trust options, this overview of types of trusts in Texas can help place bypass trusts in context.

A bypass trust also sits squarely in the world of trust administration, not just drafting. That means someone has to manage it, account for it, follow its terms, and communicate with beneficiaries. A practical resource such as Texas Trust Administration: A Trustee's Guide can help families understand what trust administration involves and how it differs from probate.

Practical rule: A bypass trust is powerful because it separates ownership. That same separation is also why it can feel restrictive to a surviving spouse.

For some Texas families, that tradeoff is worth it. For others, it isn't.

How a Bypass Trust Operates Step by Step

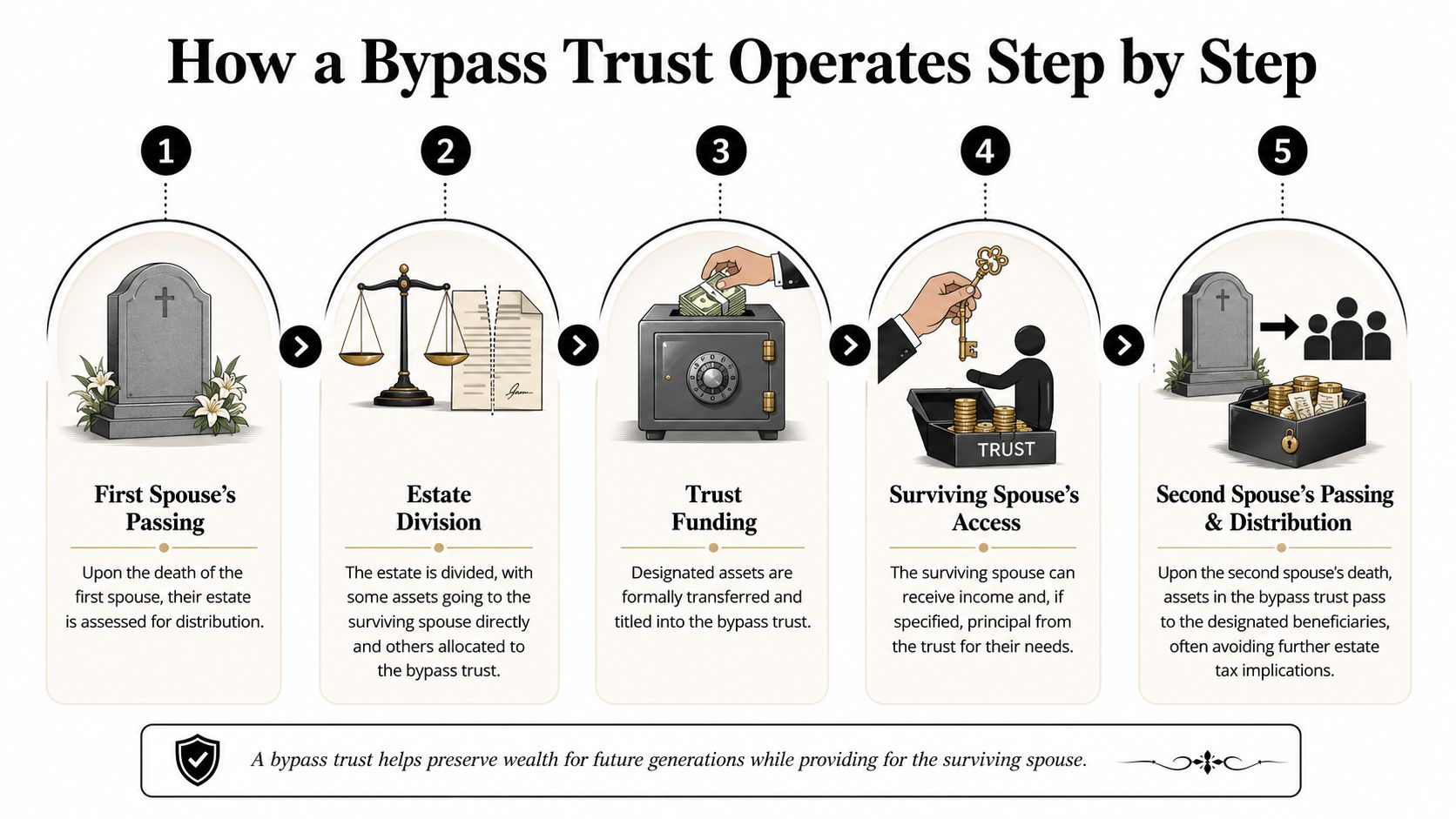

A bypass trust makes the most sense when you see it in motion. Consider a Texas couple, Maria and James. They created a joint estate plan years ago. James dies first. At that moment, the legal structure changes.

To visualize that process, this graphic helps:

Step one and step two

James's estate does not pass in one lump to Maria. Instead, the trust plan divides the property into separate shares. One portion may remain available to Maria more directly. Another portion is set aside in the bypass trust.

This split is the heart of the structure. The bypass trust becomes its own legal container, separate from Maria's personal property.

Step three and step four

Next, the trustee funds the bypass trust. That means assets must be transferred into it. Titles, account ownership, and records need to match the trust terms. If that step is handled poorly, the plan can fail in practice even if the documents look good on paper.

Maria may still receive income from the bypass trust, and sometimes principal, but her access must be limited. According to Texas trust guidance on bypass trusts, to ensure assets in a bypass trust are exempt from the surviving spouse's estate tax under IRC section 2041, their access to the principal must be limited to an "ascertainable standard," such as for "health, education, support, or maintenance." Unrestricted access would grant them a general power of appointment, causing the assets to be included in their estate at death.

That's why lawyers often use the shorthand HEMS:

- Health

- Education

- Maintenance

- Support

If the surviving spouse can take principal whenever they want, the tax protection can collapse.

Step five

When Maria later dies, the property still held in the bypass trust passes to the named remainder beneficiaries, often the couple's children. The trust document controls who receives what and when.

This video gives a useful overview of the structure and its moving parts:

Where administration often goes wrong

Families usually struggle in three places:

Funding mistakes

The documents call for a bypass trust, but no one retitles assets correctly.Distribution confusion

The surviving spouse assumes they can use trust principal freely, even though the trust limits access.Poor records

Trustees fail to keep separate books, track income, or explain distributions to beneficiaries.

Those problems are avoidable, but only if the trustee understands that a bypass trust is an active legal arrangement, not a passive form.

Bypass Trusts vs Portability Is a Bypass Trust Still Necessary

For many Texans, this is the most important part of the discussion.

A bypass trust used to be a standard answer for married couples. Today, it often isn't. Federal law now allows something called portability, which lets a surviving spouse preserve the unused federal estate tax exclusion of the spouse who died first by filing IRS Form 706.

That change matters because it can reduce the need for an automatic bypass trust in many estates.

The modern problem with old documents

According to this discussion of older bypass trust provisions, a critical misconception is that bypass trusts are essential for all married couples. With the 2026 federal exemption at $13.99 million and the availability of "portability" via IRS Form 706, many pre-2011 living trusts with mandatory bypass provisions may now be a liability for moderate-net-worth families who could benefit more from simpler, more flexible disclaimer trusts.

That's the issue many Texas families face. Their trust was drafted at a time when mandatory bypass funding was common. But now that same formula can force assets into an irrevocable structure when the family would be better served by flexibility.

Bypass trust vs portability at a glance

| Feature | Bypass Trust | Portability |

|---|---|---|

| How it works | Assets move into an irrevocable trust at the first death | Surviving spouse may preserve unused exclusion by filing Form 706 |

| Flexibility for survivor | Limited by trust terms and distribution standards | Generally simpler if assets pass more directly |

| Administration | Requires ongoing trust administration | Usually less complex than a separate continuing trust |

| Asset control | Trustee must follow trust language strictly | Surviving spouse often has broader direct control |

| Best fit | May help in blended families, creditor concerns, or control-focused planning | Often attractive for families prioritizing simplicity |

For a fuller discussion of this tax concept, see this overview of portability and estate tax planning.

When a bypass trust may be the wrong fit

A bypass trust may be outdated for a Texas family when:

- The estate is well below the federal exemption and the family's real goal is simplicity.

- The surviving spouse needs flexibility to sell, reinvest, move, or use assets without trustee-style restrictions.

- The existing trust is old and contains mandatory funding language that no longer reflects current law.

- Income tax basis planning matters more than estate tax planning because bypass trust assets do not receive a step-up in basis at the surviving spouse's death.

Many families don't need more complexity. They need a plan that still works under current law and current family realities.

When a bypass trust may still make sense

That doesn't mean bypass trusts are obsolete across the board. Some Texas families still benefit from them for reasons unrelated to pure estate tax savings.

Examples include:

- Blended families where the first spouse wants to provide for the survivor but protect the remainder for children from a prior relationship

- Creditor concerns where keeping assets legally separate may matter

- Spendthrift concerns where controlled distributions protect family wealth

- Long-term control goals involving family property or closely held business interests

The right analysis isn't ideological. It's practical. A Texas estate planning attorney should review the trust language, the asset mix, the family relationships, and the likely administrative burden before deciding whether to keep, amend, or move away from a bypass trust structure.

Key Steps for Drafting and Funding a Bypass Trust

If a bypass trust still fits your situation, it has to be drafted and funded carefully. Good language alone isn't enough. The trust must also be administered as a separate legal entity under Texas fiduciary rules.

This checklist graphic captures the main setup steps:

Drafting points that matter

A Texas bypass trust should clearly state:

- Who the trustee is and who will serve if the first choice can't act

- Who benefits during the surviving spouse's lifetime

- What the distribution standard is, especially the HEMS limitation

- Who receives the remainder after the surviving spouse dies

- How the trust is funded so there's less confusion after the first death

The funding language matters more than many families realize. If the document is vague about which assets flow into the trust, administration becomes harder and disputes become more likely.

Funding and administration checklist

According to guidance on maintaining bypass trust integrity, a bypass trust must have its own taxpayer identification number (TIN), and all financial accounts must be strictly segregated from the trustee's personal accounts. The same source also notes that assets held within the trust do not receive a step-up in basis upon the surviving spouse's death, which can lead to significant capital gains taxes for beneficiaries when the assets are sold.

That leads to a practical checklist:

Review the estate plan after the first death

Don't assume the trust funds itself automatically.Identify the assets that belong in the bypass trust

Deeds, account registrations, and beneficiary designations must be examined closely.Retitle the assets correctly

A trust that isn't properly funded may not deliver the intended protection.Obtain a separate TIN

The bypass trust must operate as its own tax entity.Open separate trust accounts

Personal and trust assets can't be mixed.Track basis and records carefully

This becomes important later if beneficiaries sell appreciated property.

Texas law and practical support

Texas trust administration also intersects with the Texas Estates Code when a death triggers probate issues, executor duties, or questions about how non-trust assets pass. That's why families often need coordinated advice from a Texas estate planning attorney and, in some cases, a Texas trust administration lawyer.

For some families, one option for understanding these administration issues is the educational material available through the Law Office of Bryan Fagan, PLLC, which addresses trust administration, estate planning, probate, guardianship, and asset protection under Texas law.

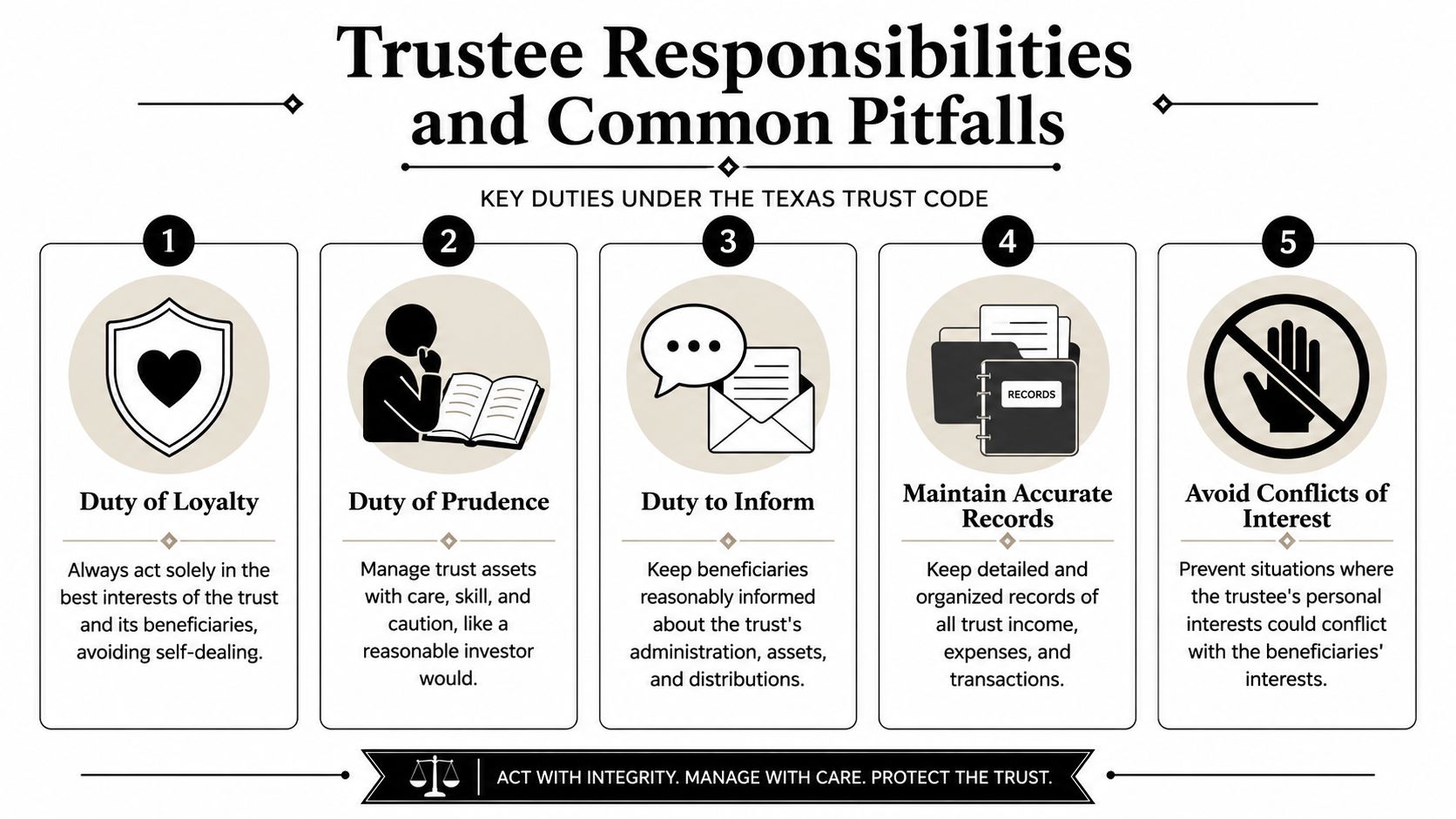

Trustee Responsibilities and Common Pitfalls

Serving as trustee is not an honorary title. It is a fiduciary job with legal duties, personal exposure, and ongoing administrative work.

Texas law expects a trustee to act carefully, fairly, and with integrity. Those duties come from the trust instrument, the Texas Trust Code, and general fiduciary principles. A trustee who misunderstands that role can create conflict with beneficiaries and personal liability for the trustee.

This visual highlights the main pressure points:

Duties that cannot be ignored

According to this discussion of Texas Trust Code section 111.0035(b), a trustee's core duties, such as the duty to administer the trust in good faith and act impartially among beneficiaries, cannot be waived. This ensures current beneficiaries receiving distributions are not unfairly prioritized over remainder beneficiaries.

That rule matters in bypass trusts because there are often two groups with different interests:

- The surviving spouse, who may receive income or principal distributions now

- Remainder beneficiaries, often children, who receive what is left later

A trustee cannot merely favor the person making the loudest request.

For a closer look at these obligations, this resource on trustee duties and responsibilities in Texas is helpful.

Common trustee mistakes

Some mistakes are legal. Others are practical. Both can be costly.

Commingling assets

The trustee mixes trust money with personal funds or uses the wrong account.Ignoring beneficiary communication

Beneficiaries aren't kept reasonably informed, which can trigger suspicion and disputes.Making unsupported distributions

The trustee pays out principal without tying the decision to the trust's stated standard.Acting as if trust property is family property

A trustee can't treat the bypass trust like a shared household account.Overlooking tax basis issues

Beneficiaries may later face avoidable problems if records are sloppy.

Trustees should document why each significant decision was made, what authority supported it, and how the decision treated all beneficiaries fairly.

Trustee authority and self-dealing risks

Texas law gives trustees real authority, but that authority has limits. Under Texas Property Code section 113.018(a), trustees may reasonably hire attorneys, accountants, investment agents, and brokers to help administer the trust. That's often the wise choice when the trust owns real estate, investment accounts, or a business interest.

At the same time, trustees must avoid self-dealing. Texas Property Code section 114.064 holds trustees accountable to beneficiaries for trust property and for profits arising from administration, which means a trustee can't benefit from the role without proper authority and full disclosure.

A practical example

Suppose a mother serves as trustee of a bypass trust after her husband dies. The trust benefits her during life, then passes to the children. One child asks for trust records. Another worries the trustee is taking too much from principal. The mother also wants to sell a trust-owned property and loan herself the proceeds.

That situation touches nearly every major fiduciary issue at once:

- impartiality between present and future beneficiaries

- accounting and disclosure

- distribution standards

- self-dealing concerns

- possible need for legal and tax professionals

A trustee in that position shouldn't guess. A Texas trust administration lawyer can help the trustee stay compliant, protect the trust, and reduce the risk of litigation. Related legal help may also involve probate administration, guardianship concerns where incapacity is an issue, and broader asset protection planning for the family.

Get Trusted Guidance for Your Texas Estate Plan

A bypass trust can still be a smart tool. But it isn't automatically the right tool.

For many Texas families, the more urgent issue is reviewing older estate plans and asking whether a mandatory bypass structure still serves the family's goals. Sometimes the answer is yes. Sometimes the better path is a disclaimer trust, a portability-focused plan, or an amendment that restores flexibility and avoids unnecessary complications.

If you're a trustee, executor, spouse, or beneficiary, don't assume the documents explain themselves. The Texas Trust Code, the Texas Estates Code, and basic fiduciary duties all shape what must happen after a death. The details matter. So do family dynamics, tax basis questions, beneficiary communication, and the practical burden of ongoing administration.

Careful planning can also prevent disputes later. That includes reviewing how to modify a trust in Texas, whether a trustee needs court guidance, and how probate, guardianship, and asset protection issues may intersect with the trust.

A current review with a Texas estate planning attorney can bring clarity quickly. It can also help you decide whether your existing bypass trust still protects your family, or whether it's time to simplify.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.