Skip to content

Skip to content Managing a loved one's trust can feel overwhelming, especially when you're grieving and family members are already asking what happens next. Most first-time trustees don't step into this role because they wanted a new administrative job. They step into it because someone they loved trusted them to finish important work.

That's the right way to think about how to settle a trust after death in Texas. This process is legal and technical, but it's also personal. You're protecting assets, following written instructions, and honoring a legacy. When trustees understand the reasons behind each step, they make better decisions and avoid the mistakes that turn a manageable administration into a family dispute.

Texas law gives you authority, but it also gives you duties. The Texas Trust Code defines your role as a fiduciary. The Texas Estates Code often matters too, especially when an asset was never transferred into the trust and may still require probate. Good trust administration also depends on old-fashioned fiduciary principles: loyalty, prudence, transparency, and careful recordkeeping. If you keep those principles in view, the work becomes much easier to organize.

An Introduction to Your Role as Successor Trustee

If you've just learned that you're the successor trustee, you're probably balancing two pressures at once. One is emotional. The other is practical. You may be sorting through funeral arrangements, house keys, bank statements, and worried questions from beneficiaries, all at the same time.

Under Texas law, a major legal shift happens at death. A revocable living trust becomes irrevocable when the grantor dies, which means the terms are locked and no one may change them. That transition also activates the successor trustee's authority and gives beneficiaries enforceable rights to information, accounting, and accountability under the Texas Trust Code rules discussed here.

That change matters because your job is no longer to assist the person who created the trust. Your job is to administer the trust exactly as written. You don't get to rewrite the plan because circumstances changed, a beneficiary is impatient, or a family member believes a different result would be fairer. If you depart from the trust terms without proper authority, you risk a breach of fiduciary duty claim.

What your role actually involves

A first-time trustee often assumes the role is mostly about dividing property. In practice, it starts with control, protection, and communication.

You'll need to:

- Locate authority documents so banks, title companies, and advisors know you're authorized to act

- Secure trust property so no asset is lost, neglected, or transferred too early

- Communicate with beneficiaries because silence creates suspicion faster than almost anything else

- Pay valid obligations first before making distributions

- Document every meaningful decision in case your work is later reviewed

Practical rule: A trustee's safest default is simple. Follow the document, keep records, and communicate before frustration turns into conflict.

Trustees sometimes benefit from a plain-English explanation of fiduciary duty and investor protection, because the core idea is the same in trust administration. You're handling property that benefits other people, so the law expects care, loyalty, and discipline.

The why behind Texas fiduciary law

The Texas Trust Code is built around one central concern. A trustee controls property that belongs in a legal sense to the trust, but is meant to benefit others. That gap between control and benefit is where mistakes happen. Fiduciary law exists to close that gap.

That's why the best trustees don't treat administration as a race to distribute assets. They treat it as a process of verification. Done well, your role protects the trust estate, the beneficiaries, and you.

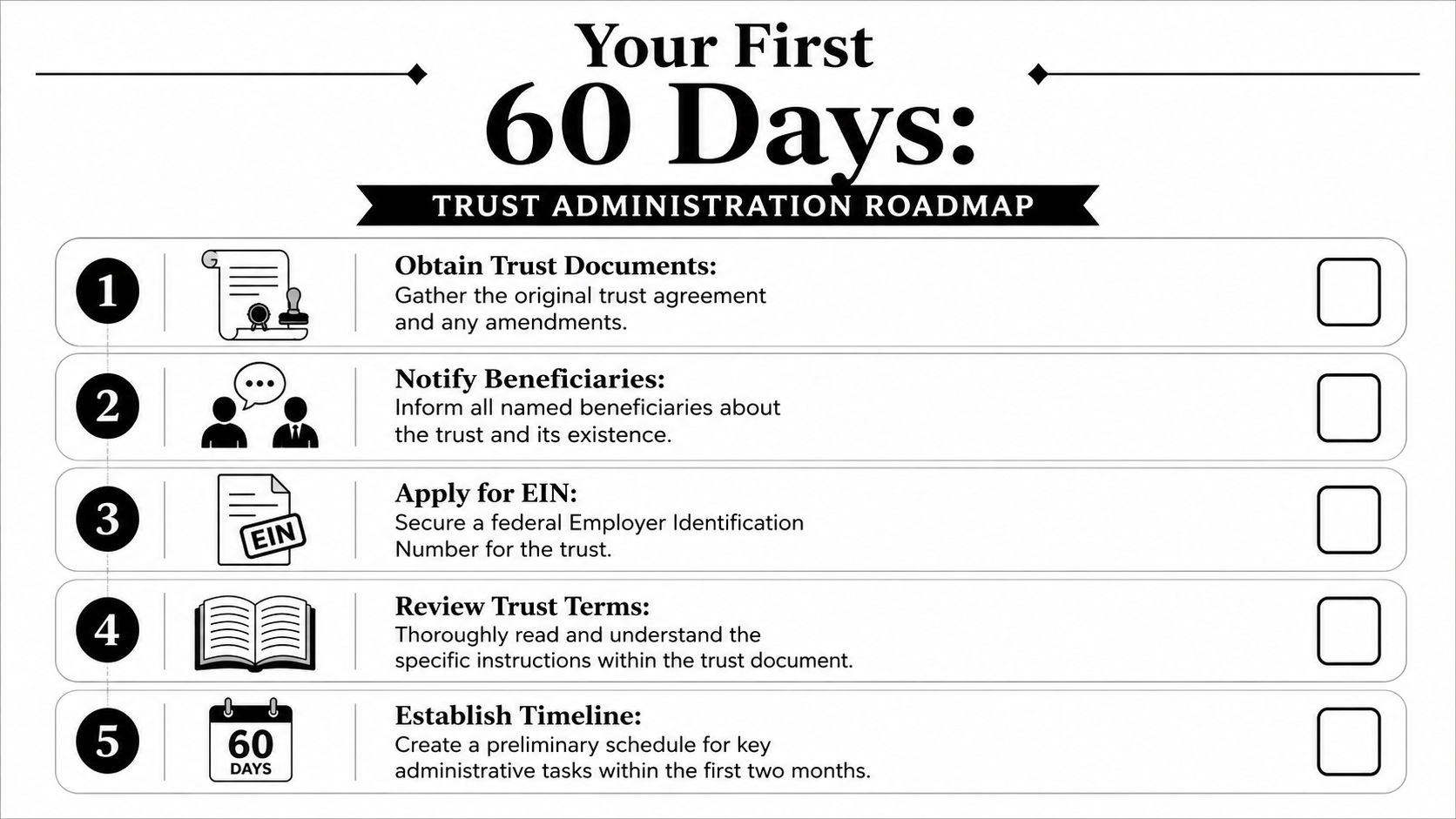

Your Initial Responsibilities in the First 60 Days

The first stretch of administration sets the tone for everything that follows. Trustees who get organized early usually avoid the confusion that causes later delays. Trustees who “wait until things settle down” often create bigger problems for themselves.

Gather the documents that prove your authority

Start with the original trust agreement and every amendment or restatement. If you only have a summary or a partial copy, don't assume that's enough. Financial institutions usually want to see reliable proof of your authority before they'll speak with you about trust assets.

You should also obtain multiple certified death certificates. In day-to-day practice, you'll use them often. Banks, brokerage firms, county offices, and insurance carriers commonly request their own copy.

A useful first-step checklist appears in this guide on first steps after becoming a trustee in Texas. If you want a focused resource on immediate trustee duties, First Steps for a Successor Trustee in Texas addresses what to do immediately after stepping into the trustee role.

Apply for a new tax ID and separate trust business from personal business

Once the grantor dies, the trust's tax posture changes. The trustee must secure a new Tax ID using Form SS-4, because the trust becomes irrevocable and no longer operates under the grantor's prior tax identity. You may also need to file IRS Form 56 to establish the trust's fiduciary status.

This is one place where first-time trustees make preventable mistakes. They keep using an old account structure, mix trust activity with personal funds, or delay opening a trust administration account. Don't do that. Even when you mean well, mixed records are hard to unwind and even harder to explain.

Notify beneficiaries early and clearly

Texas law imposes an affirmative, non-waivable duty to notify current beneficiaries that the trust became irrevocable due to the settlor's death, and that notice must be given as soon as practicable. The notice must confirm the trust exists, identify the beneficiary's status, and disclose basic trust terms. Failure to do this can create personal exposure for the trustee under the Texas beneficiary notice requirements summarized here.

A good notice does more than satisfy a legal duty. It lowers the emotional temperature. Beneficiaries usually don't expect instant distributions, but they do expect acknowledgment, clarity, and honesty about timing.

Clear communication doesn't eliminate every conflict. It does eliminate many of the conflicts that start when people assume they're being ignored.

Read the trust like an instruction manual

Before you move assets, review the trust for distribution standards, special gifts, subtrusts, age-based restrictions, and directions about real property or business interests. Some trusts call for outright distributions. Others continue for years, especially when a beneficiary is young or needs asset management.

Here are the early questions that matter most:

- Who are the current beneficiaries and what information rights do they have?

- What assets should already be in the trust and which ones may still be outside it?

- Are there continuing trusts for children, grandchildren, or a beneficiary with spending concerns?

- What does the trust say about accountings and timing of distributions?

If a provision seems unclear, pause before acting. A trustee who slows down to verify meaning is usually safer than one who moves quickly and guesses.

Inventorying Trust Assets and Managing Creditors

A trust can't be settled until the trustee knows what the trust owns, what it owes, and what may still need probate. At this stage, trust administration becomes concrete. You move from general responsibility to a list of specific assets, values, and liabilities.

Marshal the assets before you make promises

“Marshaling assets” means identifying, securing, and bringing trust property under your control as trustee. In Texas, that often includes real estate, bank accounts, brokerage accounts, business interests, and personal property.

For real estate, the successor trustee generally needs to file an affidavit of successor trustee or a new deed in the county where the property is located so public title records reflect the current trustee's authority. For financial accounts, institutions commonly ask for the trust document, the death certificate, and proof you accepted the trusteeship before they'll give you signature authority.

A practical inventory should note:

| Asset type | What to verify |

|---|---|

| Real estate | Title, insurance, taxes, occupancy, deed records |

| Bank accounts | Exact title, balance, date-of-death status |

| Investments | Account registration, holdings, cost basis information |

| Business interests | Ownership documents, operating agreements, management rights |

| Personal property | Location, condition, and whether the trust actually owns it |

Date-of-death values matter

Valuation isn't paperwork for paperwork's sake. You need reliable values for tax reporting, for fair distribution, and for deciding whether an in-kind distribution makes sense.

Take a simple example. Suppose the trust holds a house in Harris County and a brokerage account. If one child wants the house and another will receive financial assets, you can't make a fair plan without a defensible date-of-death value for both. The same is true if the trust owns ranch land, mineral interests, or a closely held business.

Beneficiaries usually accept unequal asset types more easily than unclear valuations. The problem isn't always the result. It's the lack of a transparent method.

Confirm what is and isn't in the trust

One of the most common surprises in administration is finding that an asset was never titled into the trust. If an account or parcel of land remained in the decedent's individual name, it may fall outside the trust and require a probate proceeding under the Texas Estates Code.

That's why trustees shouldn't assume a trust avoids probate for everything. A well-drafted trust only governs assets that were transferred to it, or that properly name the trust as beneficiary.

Publish notice to creditors the right way

Texas gives trustees a powerful tool for dealing with creditor claims, but only if they use it correctly. When settling a revocable living trust after death, the successor trustee must publish a Notice of Trust in a newspaper in the decedent's county of residence for a continuous period of two weeks, and that publication triggers a strict 4-month deadline for claims. All claims against the trust must be filed within 4 months after the second publication, as described in this Texas trust creditor notice discussion.

This step is not a technicality. It helps close the trust against later claims and protects the trustee from personal exposure. If valid debts aren't handled properly, the trustee may be personally liable before beneficiaries ever are.

What works and what doesn't

A trustee usually does well when they build a written asset list, preserve supporting statements, and treat each asset transfer like a document trail that may be reviewed later.

What doesn't work is memory, informal family understandings, or verbal assurances from institutions. Trust administration is much smoother when the file can prove each step without relying on anyone's recollection.

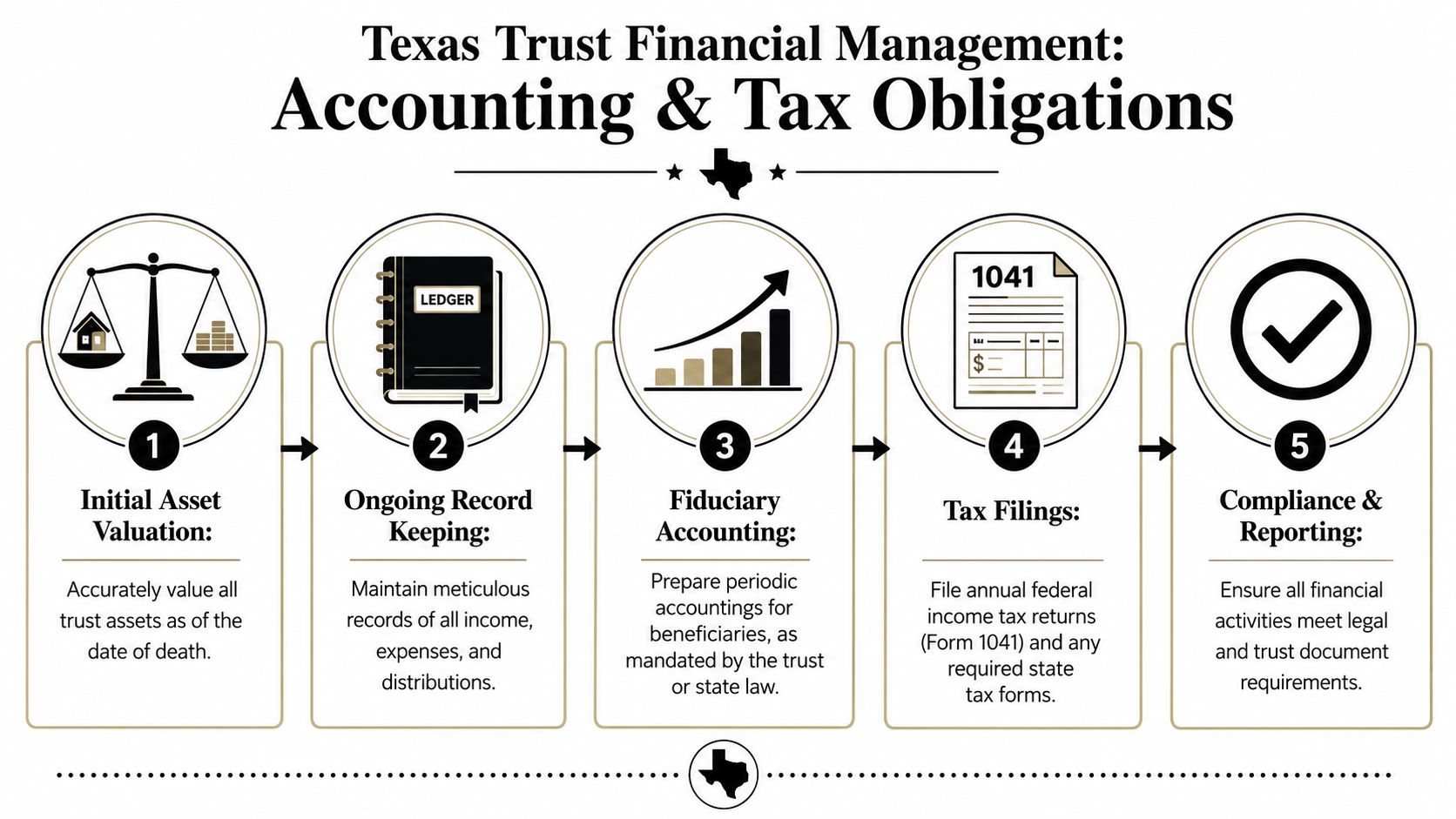

Fiduciary Accounting and Tax Obligations in Texas

Once assets are identified, administration becomes a financial management job. Trustees don't need to be accountants, but they do need accounting discipline. In Texas, that discipline is part of your fiduciary duty.

Keep records as if you'll have to explain every transaction

That standard may sound strict, but it's the safest one. Beneficiaries have rights to information and, in many cases, accountings. If you can't show where money came from, where it went, and why, your administration becomes vulnerable.

Before distributing assets, the trustee must settle valid debts, administrative costs, property taxes, and trust tax obligations, including the grantor's final tax returns and, if applicable, a trust income tax return on Form 1041. Texas courts also require precise transaction records, as explained in this overview of Texas trust administration accounting and tax duties.

A practical accounting system should track:

- Receipts such as dividends, rent, interest, refunds, and sale proceeds

- Disbursements including taxes, maintenance, professional fees, insurance, and debt payments

- Distributions to beneficiaries, whether cash or property

- Asset changes such as market sales, retitling, or liquidation events

For trustees who want a deeper look at reporting expectations, this resource on fiduciary accounting in Texas is a helpful starting point.

Understand the difference between the decedent's taxes and the trust's taxes

These are related, but they're not the same.

The decedent may still need a final personal income tax return for the last year of life. The trust, after death, may need its own income tax reporting if it earns income during administration. That often happens when trust assets generate dividends, interest, rental income, or gains from asset sales.

A few practical points help trustees avoid confusion:

| Return or filing | Why it matters |

|---|---|

| Final personal return | Closes out the decedent's own income tax obligations |

| Form 1041 for the trust | Reports post-death trust income when required |

| Form 56 and EIN setup | Establishes fiduciary authority and the trust's tax identity |

Accountings are not just for disputes

Some trustees think a formal accounting is only necessary if a beneficiary is difficult. That's usually backwards. A good accounting often prevents the very distrust that leads to a dispute.

An accounting should make it easy for a beneficiary to see the administration path: opening assets, income collected, expenses paid, distributions made, and assets remaining. It doesn't need drama. It needs clarity.

Important point: If you distribute first and try to reconstruct records later, you've made the hardest version of the job for yourself.

Good process protects the trustee

Fiduciary principles and practical administration often overlap. Accurate books show that you acted prudently. Timely tax compliance shows you respected legal obligations. Together, they create a record that supports your decisions if anyone questions them later.

That's why careful trustees use a dedicated bank account, preserve statements, and avoid cash transactions whenever possible. Clean records don't just help the beneficiaries. They protect you.

Distributing Assets and Terminating the Trust

Distribution is the part families usually focus on first, but it should happen near the end. Once debts, taxes, expenses, and asset verification are handled, the trustee can move into the final phase with much more confidence.

Follow the trust terms exactly

The trust document controls the distribution plan. If it says one beneficiary receives a specific piece of property, the trustee shouldn't substitute cash because that seems easier. If it requires a continuing trust for a younger beneficiary until a stated age, the trustee can't accelerate distribution just because the family agrees informally.

This is one of the clearest differences between serving as trustee and serving as an informal family coordinator. Your authority exists to carry out written instructions, not to negotiate a new estate plan after death.

A successor trustee's fiduciary responsibilities can continue until the trust is fully distributed, and sometimes much longer when the trust includes staged distributions or ongoing management of property for beneficiaries, as explained in this discussion of successor trustee duties in Texas.

Create a distribution plan before moving assets

Even when a trust allows immediate distributions, it helps to slow down and create a written plan. That plan should identify what each beneficiary will receive, whether the distribution is cash or in kind, what conditions must be satisfied first, and what documents the trustee wants signed on delivery.

A useful distribution checklist often includes:

- Confirming all obligations are paid so no later bill forces a clawback

- Matching each gift to the exact trust language rather than family expectation

- Preparing transfer documents for deeds, assignments, account transfers, or bills of sale

- Obtaining receipts and releases when beneficiaries receive property

Handle difficult assets with extra care

Some assets are easy to split. Cash is simple. Publicly traded securities can often be transferred or liquidated with relative efficiency. Other assets are harder. A family home, vacation property, mineral interest, or closely held business can produce disagreement even when the trust terms are clear.

In those situations, trustees do better when they explain process before outcome. For example, if a home must be sold and proceeds divided, say that early. If one beneficiary wants to buy out another's share, document the valuation method and timing. If the trust requires continued management of an asset, explain that the role doesn't end just because someone wants a faster result.

Here's a practical overview of how trustees think through final distributions and closure:

Final accounting and trust termination

Before closing the trust, provide the final accounting required by the trust terms or reasonably requested by beneficiaries. This is your closing report. It should show what came into the trust, what was paid out, what was distributed, and that the balance is now zero or otherwise fully allocated.

After that, the trustee typically completes the final transfers, preserves the trust file, and documents that the administration has ended.

A careful closing matters. Many trustee disputes don't start at the beginning. They start after an incomplete or poorly documented final distribution.

Where related legal services fit

Some administrations stay entirely within trust administration. Others spill into neighboring areas of law. If you discover untitled assets, probate may be necessary. If a beneficiary is incapacitated or a minor, guardianship issues may arise. If the trust holds a business or complex property, broader asset protection and transfer planning may matter. A Texas trust administration lawyer and a Texas estate planning attorney often coordinate across those areas because trust settlement rarely exists in isolation.

Avoiding Common Pitfalls and When to Seek Legal Help

Most trust disputes don't start with fraud. They start with missed notices, poor records, vague explanations, or distributions made before the file is ready. Trustees usually mean well. The trouble comes from underestimating how formal the role really is.

Texas trust administration data points to a few recurring problem areas. 30% of trust disputes arise from inadequate beneficiary notification, 25% from misvaluation of assets, and 20% from premature distributions before debt or tax clearance. Those mistakes often stretch administration from a typical 6 to 12 months to 18+ months and increase administrative costs by 40 to 60%, according to this Texas trust dispute overview.

The disputes trustees can prevent

A surprising number of conflicts are preventable with basic habits. Beneficiaries don't need constant updates, but they do need enough information to understand that the trustee is working from a plan.

The patterns that usually cause trouble look like this:

- Silence after death leaves beneficiaries guessing whether the trustee is acting at all

- Loose valuations create suspicion that one person is being favored

- Early distributions make later tax or creditor issues much harder to solve

- Informal side agreements pull the trustee away from the written trust terms

Families often describe these situations as fairness problems. Legally, they're usually process problems first.

What prudent trustees do differently

Strong trustees act like managers of a file, not just holders of family authority. They keep communications measured, preserve supporting documents, and explain delays before delays become frustrations.

When a conflict may be developing, these steps usually help:

- Send a written status update that explains what has been completed and what is still pending.

- Use third-party valuations when an asset could become a point of disagreement.

- Pause distributions if taxes, debts, title issues, or unclear trust language remain unresolved.

- Ask for legal guidance early instead of waiting until positions harden.

If you're unsure whether a problem has crossed the line from routine administration to legal risk, this guide on when to hire a trust administration attorney in Texas can help frame the decision.

When legal help is the prudent move

Seeking counsel isn't a sign that you've failed as trustee. In many cases, it's the most responsible decision you can make. Legal help is especially important when the trust owns unusual assets, the document is ambiguous, a beneficiary challenges your actions, or an asset appears to fall outside the trust and into probate.

This is also where a law firm's broader practice matters. A trustee may need guidance that touches estate planning, probate, guardianship, or asset protection at the same time. The Law Office of Bryan Fagan, PLLC handles trust creation, administration, modification, termination, and related fiduciary and probate issues in Texas, which is the kind of integrated support trustees sometimes need when administration becomes more complex.

The most effective trustees understand one final point. Your job isn't to satisfy every family preference. Your job is to administer the trust lawfully, transparently, and with respect for the person who created it. That's how you protect the estate and preserve as much family peace as the situation allows.

If you're managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.