A week after a loved one dies, the practical questions usually arrive before the grief has settled. Someone hands you a binder. A banker asks for documents. A beneficiary wants to know what happens next. You may have just learned that you're the successor trustee, and now every paper, password, and property record feels urgent.

That feeling is normal.

Most trustees aren't failing because they don't care. They struggle because nobody showed them a workable system. They were told to "keep good records" without being told what that looks like in a Texas trust administration.

A good record system does two jobs at once. It helps you carry out your loved one's wishes, and it protects you as the trustee if questions come later. If you're just starting, a practical first steps after becoming a trustee in Texas guide can help you get your footing.

Your Guide to Managing a Loved One's Trust

A new trustee usually starts in the same place. The trust exists somewhere. The house deed may or may not be in the trust. Financial statements are scattered between paper mail, email, and online portals. Family members assume you know what to do.

You don't need to know everything on day one. You do need a method.

Think about two common Texas scenarios. In the first, a daughter finds the trust agreement in a fireproof box, but the brokerage statements are still going to her father's email. In the second, a son knows there is rental property in the trust, but he can't tell whether the deed was ever updated. Both trustees have the same problem. They need a record system before they can make reliable decisions.

Good trust administration starts with locating authority, identifying assets, and preserving proof.

That's why learning how to organize trust records and documents Texas style isn't busywork. It's one of the most practical parts of fiduciary service. Once the papers are gathered and the files make sense, the rest of the administration becomes far more manageable.

The work usually falls into three parts:

- Gather the right documents: Find the trust agreement, asset records, tax information, insurance papers, and contact information.

- Build one filing system: Use the same structure for paper files and digital files so nothing gets lost.

- Maintain the record trail: Log transactions, save supporting documents, and keep communications clear.

Texas families often need reassurance that this can be done in an orderly way. It can. The key is to stop treating trust records like a pile of paperwork and start treating them like evidence of careful administration.

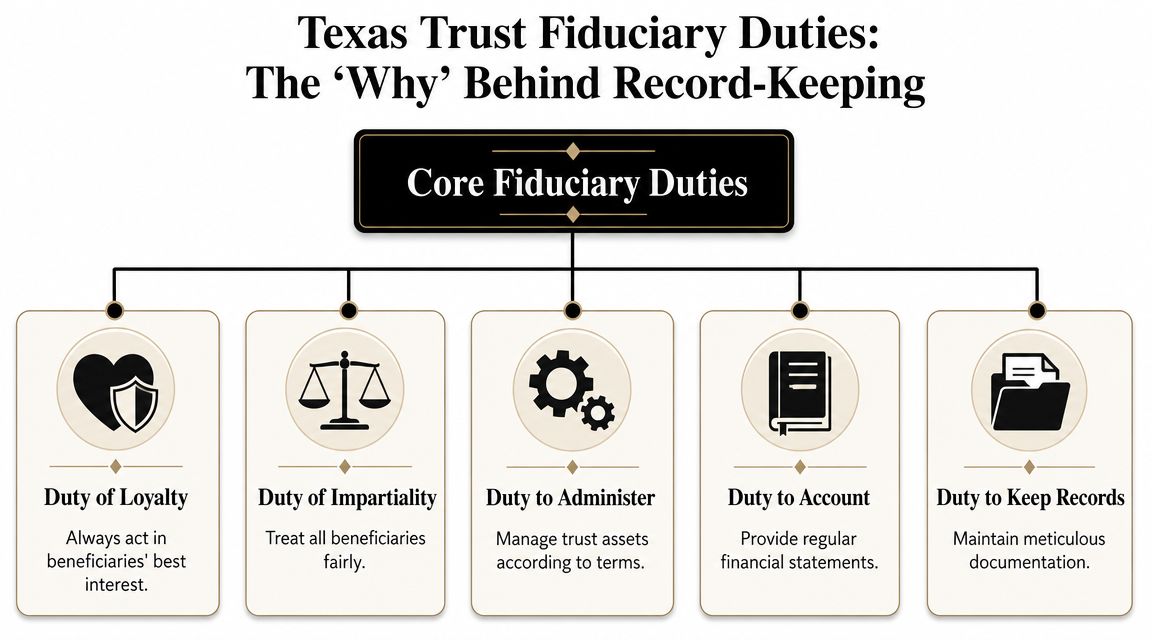

Understanding Your Core Fiduciary Duties in Texas

Being a trustee isn't just an honor. It's a legal role. Under the Texas Trust Code and general fiduciary principles, you're expected to act in the beneficiaries' interests, manage trust property responsibly, and keep records that show what you did and why. The Texas Estates Code also matters because some assets may still involve probate or other estate administration questions if they were never properly transferred into the trust.

For many trustees, anxiety often begins here. They assume the law expects perfection. It doesn't. It expects diligence, honesty, and organized follow-through.

What these duties mean in plain English

A trustee's core duties usually sound technical, but the daily application is practical:

- Duty of loyalty: You must act for the beneficiaries, not for your own convenience or advantage.

- Duty of prudence: You need to make careful, informed decisions about trust assets.

- Duty of impartiality: If there are multiple beneficiaries, you can't favor one unfairly over another.

- Duty to administer the trust: You must follow the trust terms as written, unless a court or applicable law requires something different.

- Duty to account and inform: You should keep beneficiaries reasonably informed and be able to show accurate records if asked.

If you strip away the legal language, the message is simple. A trustee must be able to explain each significant action and support it with records.

Why record-keeping is part of fiduciary compliance

Many trustees think accounting is something they do at the end. In reality, record-keeping starts the moment you take over. Every letter, statement, appraisal, invoice, and distribution receipt may become part of the story you later need to tell.

Practical rule: If you make a decision as trustee, keep the document that explains why and the document that proves what happened next.

That includes records tied to asset ownership. Texas-focused guidance stresses that a trust isn't really operational until assets are transferred into it, and failure to fund the trust is a major reason trusts don't work as intended because assets can remain outside the trust and still pass through probate, as discussed in this Texas trust funding overview.

That issue surprises trustees all the time. A trust agreement may exist, but if the deed, account title, or beneficiary arrangement was never updated, the asset may not be controlled by the trust.

A common first mistake

A trustee often assumes, "If Mom signed the trust, the house and accounts must be in it." That's not always true. Your first task is to verify funding, not assume it.

A careful review usually includes:

- Read the trust agreement and any amendments

- Check title on each major asset

- Compare the trust papers to current statements and deeds

- Flag anything that may still be outside the trust

If you want a deeper explanation of these legal obligations, this discussion of fiduciary duties of trustees in Texas is a useful next step.

Once you understand the duty, the filing system makes more sense. You're not organizing papers for appearance. You're creating proof that you acted like a responsible fiduciary in Texas.

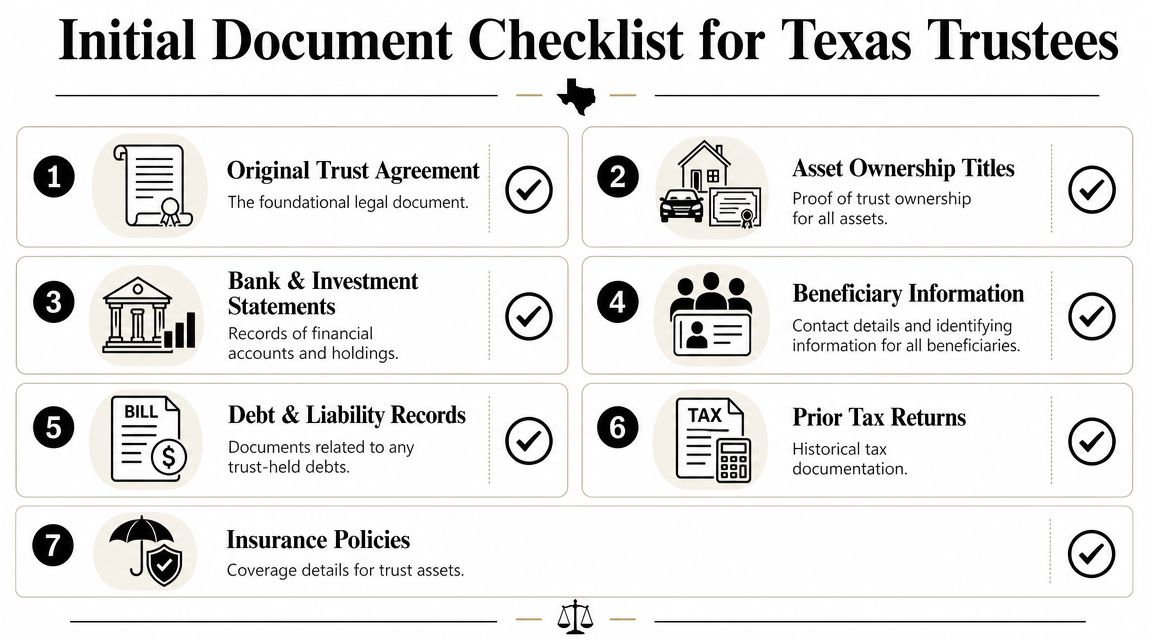

The Initial Collection What Trust Documents to Gather

You may be standing in a living room with a banker asking for proof, a relative handing you a stack of papers, and three different passwords scribbled on envelopes. That is a normal start. The goal at this stage is simple. Gather enough records to prove your authority, identify what the trust owns, and preserve the paper trail before anything gets misplaced.

This checklist image gives a helpful overview before you begin:

Start by collecting, not perfecting. Sorting can wait until the documents are in one controlled place.

Pull the papers that prove you can act

A trustee cannot do much without authority documents. Financial institutions, title companies, insurance carriers, and tax professionals usually want to see them before they will speak freely with you or change account access.

Gather these first:

- Trust agreement and all amendments: Keep the signed version together with every later amendment or restatement.

- Certification or abstract of trust, if one exists: Many institutions prefer a short summary rather than the full trust instrument.

- Death certificate: This is often required to obtain information, retitle accounts, or claim benefits.

- Trustee acceptance, resignation, or successor trustee documents: Save anything showing how you became the acting trustee.

- Related estate planning documents: Pour-over will, powers of attorney, and any memorandum about tangible personal property can answer questions that the trust alone does not.

If you find originals, treat them like vehicle titles. Do not staple notes to them, highlight them, or carry them around from meeting to meeting. Scan them, label the scans clearly, and work from copies.

Build one master inventory early

Trust administration gets easier once every asset has a line on a master list. That list is the index for everything else you collect. Without it, trustees tend to chase random statements and miss gaps in ownership, valuation, or insurance.

Your inventory should identify:

- What the asset is

- Where it is held

- How it is titled

- What document proves ownership

- Whether a date-of-death value is needed

- What follow-up is still pending

A spreadsheet works well because it can double as a task list. Common columns include:

- Asset description

- Institution or location

- Account number or identifier

- Current title

- Proof of ownership on hand

- Date-of-death value requested

- Assigned professional, if any

- Follow-up status

A short video can help reinforce what trustees are dealing with in the early stages of administration.

Gather supporting records in groups that make sense later

Once the inventory exists, start matching each asset to its supporting documents. File gathering works like assembling an evidence file. If a beneficiary asks why you valued, insured, sold, or distributed something a certain way, the answer should be sitting in that asset's folder.

Focus on these categories:

- Real estate records: Deeds, title policies, property tax notices, insurance policies, mortgage statements, HOA records, surveys, leases, and repair invoices

- Financial account records: Recent statements, beneficiary forms if relevant, account agreements, online access details stored securely, and confirmation of any account freezes or retitling

- Business interests: Operating agreements, shareholder records, buy-sell agreements, prior valuations, K-1s, and tax returns

- Personal property: Appraisals, photographs, inventory lists, receipts, storage contracts, and records for firearms, collections, jewelry, or vehicles

- Debt records: Promissory notes, credit lines, liens, recurring bills, and payoff statements tied to trust property

- Tax records: Prior income tax returns, gift tax returns, property tax records, and correspondence from taxing authorities

- Insurance records: Home, liability, umbrella, auto, business, and vacant-property coverage

Keep collecting until each significant asset has two things. Proof that it exists, and proof of what it was worth or what it was titled as.

Do not overlook hard-to-find records

Some of the most important trust documents are not sitting in the obvious folder. Check the decedent's email, prior tax returns, and safe deposit box records for clues about assets that are easy to miss. Mineral interests, small local bank accounts, brokerage accounts with paper statements turned off, and partnership interests often surface this way.

Also look for records of liabilities and ongoing expenses. Trustees sometimes gather only asset documents and forget the bills attached to them. Property taxes, insurance premiums, management fees, loan payments, and utilities all matter because they affect administration decisions and later accounting.

A practical Texas example

Suppose the trust appears to own a Harris County home, a brokerage account, and mineral interests in West Texas. Your file for the house should include the recorded deed, current insurance, tax statement, mortgage information if any, photographs, and a valuation document. The brokerage file should include the latest statement, title registration, named beneficiaries if applicable, and the institution's date-of-death valuation. The mineral interests file should include division orders, royalty statements, deeds or assignments, and contact information for the operator.

That may sound like a lot. In practice, it is just one folder per asset, with a checklist in front.

That approach is what makes the system court-defensible later. You are not trying to create a museum archive. You are creating a repeatable record that shows what you found, what you verified, and what still needs attention.

Creating Your Defensible Filing System Physical and Digital

Most trustees don't need a fancy system. They need a repeatable one. The strongest filing systems are boring in the best way. Anyone reviewing them can understand the structure without needing your memory.

Texas guidance increasingly points to a hybrid approach. Original signed documents should be stored securely, while digital backups should be encrypted and paired with a master inventory that helps the trustee locate both originals and digital records, including passwords and account portals, as discussed in this estate document organization guide.

Use one structure in both places

Set up a physical binder or file box and a matching digital folder tree in Google Drive, Dropbox, OneDrive, or a secure document platform. The names should mirror each other. If the paper file says "04 Real Estate," the digital folder should say the same thing.

That consistency matters when you're tired, under pressure, or answering a beneficiary question months later.

| Main Folder | Subfolders & Contents |

|---|---|

| 01 Governing Documents | Trust agreement, amendments, death certificate, trustee acceptance, certifications of trust |

| 02 Master Inventory | Asset spreadsheet, funding matrix, contact list, task log, timeline notes |

| 03 Financial Accounts | Bank statements, brokerage statements, account-change confirmations, online access instructions |

| 04 Real Estate | Deeds, tax records, insurance, mortgage statements, leases, repair invoices, appraisals, photographs |

| 05 Personal Property And Business Interests | Appraisals, ownership records, valuation materials, photos, transfer documents |

| 06 Expenses And Disbursements | Invoices, bills paid, reimbursement records, receipts, proof of beneficiary distributions |

| 07 Taxes | Prior returns, current filings, notices, workpapers provided by the CPA |

| 08 Beneficiary Communications | Notices, letters, emails saved as PDFs, call notes, meeting summaries |

| 09 Final Accounting And Closing | Interim accountings, final reports, receipts and releases, closing checklist |

What belongs in the master control file

Every trustee should have one place that answers the question, "What do we have, where is it, and what's still pending?" That's your master control file.

Include:

- Asset inventory spreadsheet

- Funding matrix showing each asset, transfer instrument, date of retitling, and current title status

- Beneficiary contact sheet

- Professional contacts such as CPA, realtor, appraiser, financial advisor, and attorney

- Task tracker for deadlines, requests sent, and responses received

- Document location map showing where originals are stored

If you're using digital folders, save file names in a standard format such as "2025-04 Bank Statement Wells Fargo Trust Checking" or "HarrisCounty Deed ElmStreet Property." Searchable naming saves enormous time later.

How to handle digital-first assets

Organizing trust records often presents a hurdle for many trustees. The decedent may have used online-only bank access, cloud storage, paperless statements, and password managers. If you don't map digital access early, records can disappear into a login screen.

A workable digital protocol looks like this:

- Create a secure access list with account portals, username location, multi-factor contact method, and status notes

- Store passwords in a secure password manager if lawful and available to you, rather than in a loose text document

- Export key statements to PDF so your file doesn't depend on future website access

- Back up the digital trust folder to an encrypted secondary location

- Keep originals offline when necessary for signed trust documents, deeds, or certified records

Keep the original where it is safest. Keep the scan where it is easiest to find. Keep the inventory where a successor could understand it.

Make the system court-defensible

A defensible system is one that tells a coherent story. If a beneficiary, court, accountant, or Texas trust administration lawyer reviews your file, they should be able to see:

- what property existed,

- what authority you had,

- what actions you took,

- what communications you sent,

- and what support exists for each transaction.

That doesn't require expensive software. It requires consistency. Some trustees use labeled binders and Excel. Others use Adobe Acrobat, Dropbox, and a spreadsheet. Some families also work with counsel to set up a standardized administration file, including support from the Law Office of Bryan Fagan, PLLC, when the trust involves multiple assets, family tension, or incomplete funding records.

Ongoing Maintenance Accounting and Beneficiary Communication

A filing system only helps if you keep using it. Once the initial setup is done, the trustee's main job shifts to maintenance. Consequently, organized records reduce stress. Instead of rebuilding history at the end, you record events as they happen.

Keep a ledger, not just a folder of statements

In Texas trust accounting, every transaction must be traceable. Best practices call for a formal ledger that records the owner, purpose, date, and running balance for each entry, with monthly reconciliation and retention of supporting records such as bank statements, ledgers, and reconciliation reports for at least five years after representation ends, according to this Texas trust accounting guidance.

That means saving statements isn't enough. You need a working ledger.

A simple trust accounting workflow often includes:

- Dedicated trust bank account: Keep trust funds separate from personal money.

- Transaction ledger: Track deposits, expenses, distributions, and transfers.

- Monthly reconciliation file: Match the bank balance, ledger balance, and the total of sub-ledgers if the trust administration requires them.

- Supporting document attachment: Each ledger entry should point to a receipt, invoice, statement, or confirmation.

If you're unsure how the accounting side should be structured, this overview of fiduciary accounting in Texas can help clarify the expectations.

A practical monthly routine

Trustees often do better with a set monthly checklist than with vague reminders to "stay organized." Here's a routine that works:

- Download the statements: Save bank, brokerage, and credit-related records to the correct folder.

- Update the ledger: Enter every receipt, bill payment, and distribution while the details are fresh.

- Reconcile the account: Compare ledger entries against the statement and flag anything you can't explain.

- File source documents: Attach or save invoices, receipts, deposit records, and confirmations in the same month folder.

- Update the task log: Note outstanding appraisals, tax questions, pending sales, or unanswered beneficiary requests.

For receipt-heavy administrations, especially where trust property has maintenance costs or tax-related expenses, this practical guide on tax receipt organization offers useful ideas on sorting and preserving backup documents.

Beneficiary communication doesn't have to be complicated

Many trustee disputes start with silence, not wrongdoing. Beneficiaries get nervous when they don't know whether anything is happening. You don't have to write a legal brief every month. You do need communication that is accurate, calm, and documented.

A strong update usually includes:

| Item to communicate | What to include |

|---|---|

| Current status | What stage of administration you're in |

| Assets being handled | Which assets are confirmed, valued, or pending transfer or sale |

| Expenses paid | General categories of administration costs |

| Next steps | What you expect to do before the next update |

| Requests for information | Any documents or decisions needed from beneficiaries |

Save the email as a PDF or keep a copy of the signed letter in the communication folder. If you speak by phone, make a short memo to file.

Clear communication won't eliminate every conflict, but it often prevents confusion from becoming suspicion.

A simple example of a trustee update

A useful update might say that the trust home is insured and being prepared for appraisal, the brokerage firm has been asked for date-of-death records, property taxes were paid from the trust account, and no distributions will be made until values and expenses are confirmed. That's enough to show movement without overpromising.

This is also where fiduciary duties in Texas and broader asset protection concerns overlap. If you're preserving trust property, handling liability risks, or protecting a vulnerable beneficiary's interests, related planning around asset protection strategies in Texas may become part of the larger conversation.

When to Consult a Texas Trust Administration Lawyer

Some trustees can handle a straightforward administration with good records, steady communication, and help from a CPA or financial professional. Others run into legal questions that shouldn't be guessed at.

Consider speaking with a Texas trust administration lawyer if any of these issues appear:

- Unclear trust language: You can't tell what the trust requires, when distributions should occur, or how discretion should be used.

- Funding problems: Important assets may never have been transferred to the trust, and you're unsure whether probate is now required under the Texas Estates Code.

- Beneficiary conflict: Someone is accusing you of favoritism, demanding immediate distributions, or threatening suit.

- Complex assets: The trust holds a business, mineral interests, rental property, or assets that need valuation and coordinated transfer work.

- Tax uncertainty: You don't know what filings, basis records, or reporting duties apply.

- Successor trustee confusion: Authority documents are missing, or institutions are refusing to recognize your role.

A Texas estate planning attorney can also help when the trust itself needs review because the administration exposed larger estate plan problems, such as outdated deeds, inconsistent beneficiary designations, or missing instructions after a death or incapacity.

You don't need to wait until a dispute is underway. In many cases, early legal advice is what keeps a manageable file from turning into expensive litigation. The same is true if your family also needs help with probate, guardianship, or questions about how to modify a trust in Texas.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.