You may be looking at everything you've built and asking a hard, personal question: how do we keep this from unraveling after we're gone?

For many successful Texas families, that question doesn't start with taxes. It starts with people. A daughter who is responsible but busy raising children. A son-in-law in a high-risk profession. Grandchildren who may inherit substantial wealth before they're ready to manage it. A family business that took decades to build. Land, investments, and values that matter just as much as the balance sheet.

A dynasty trust can help hold those pieces together. Used carefully, it isn't just a legal document. It's a long-range structure for stewardship, protection, and family governance. For families exploring dynasty trusts in Texas, the key consideration isn't whether the concept appears intricate. It's whether the plan fits the family's assets, goals, and tolerance for long-term administration.

Planning Your Legacy Beyond a Single Lifetime

A common conversation starts like this. A Texas business owner has spent years building a successful company, paying close attention to risk, growth, and succession. Their estate plan may already include wills, powers of attorney, insurance planning, and a revocable living trust. But one concern remains. If assets pass outright to children, what happens after that?

An outright inheritance can work well for some families. But it can also create pressure points. A beneficiary may face creditors. A marriage may fail. A child may be financially mature, but the next generation may not be. The family may also want wealth to do more than transfer. They may want it to support education, encourage work, preserve a business, or protect vulnerable beneficiaries.

That's where a dynasty trust enters the picture. Instead of handing assets down in a series of direct transfers, the family places selected assets into a long-term trust designed to benefit multiple generations under one durable set of rules.

A strong legacy plan doesn't just move wealth. It gives future generations a structure for using it wisely.

Families often pair this planning with broader estate review. For example, if a loved one dies and life insurance becomes part of the planning picture, practical resources like Evermore Directory's insurance insights can help families understand what happens next while the legal and financial team handles the larger estate framework.

Why families look beyond a basic inheritance

Several concerns usually drive this kind of planning:

- Long-term protection: Parents and grandparents often want assets protected from personal and financial disruptions in later generations.

- Order and consistency: A trust can create one management system instead of repeated transfers and repeated mistakes.

- Values-based stewardship: Some families want wealth to remain a support system, not become a source of harm or conflict.

For the right family, this approach can feel less like “locking up money” and more like building a private family framework that outlasts any one person.

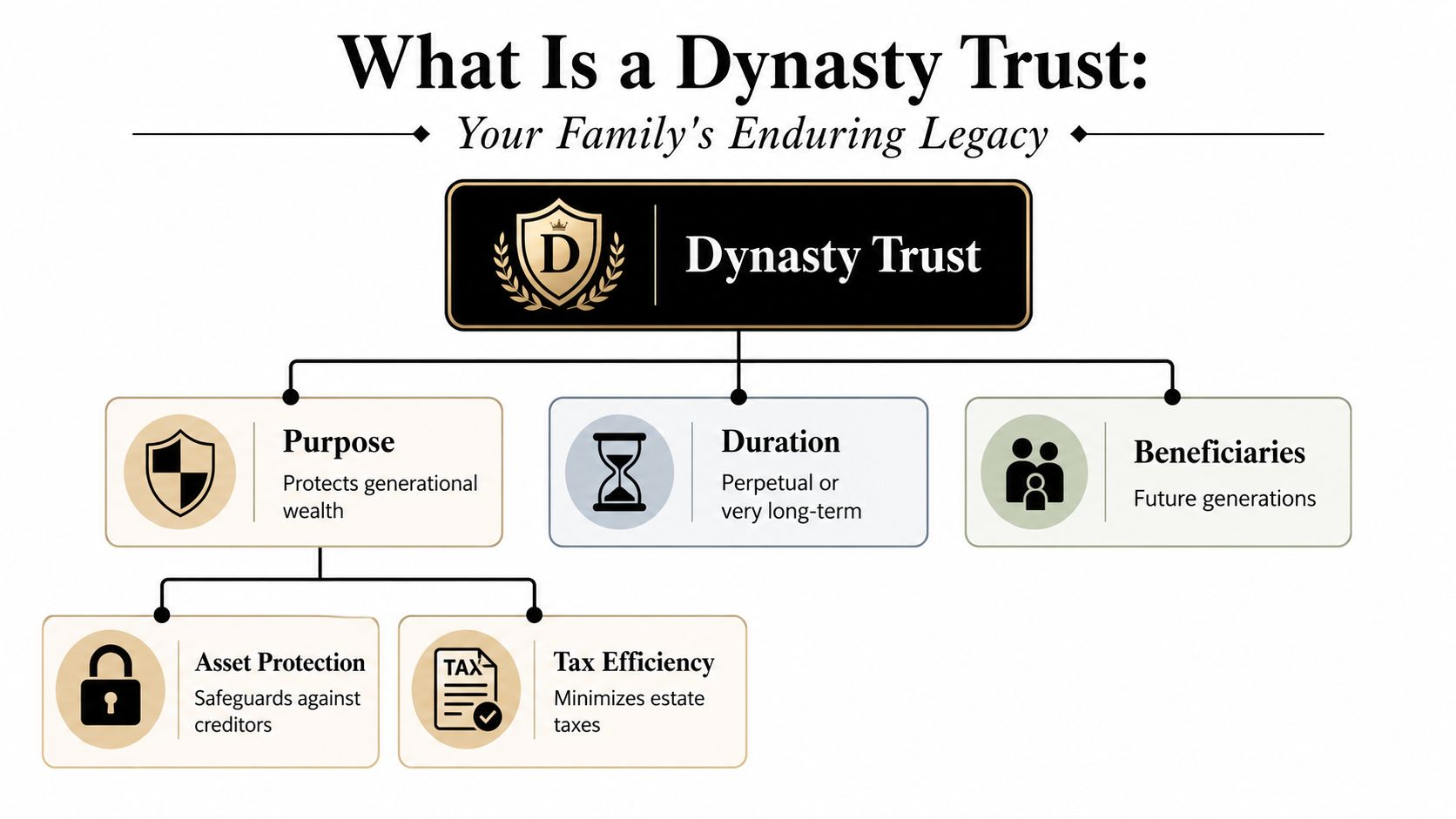

What Is a Dynasty Trust

A dynasty trust is a long-term irrevocable trust designed to hold wealth for multiple generations. The easiest way to understand it is to think of it as a private family endowment. Instead of distributing everything when one generation dies, the trust continues, and future descendants receive benefits according to the rules written into the trust document.

How it differs from a revocable living trust

Many families are already familiar with a revocable living trust. That type of trust is usually about convenience, privacy, and avoiding some probate friction. The person who creates it usually keeps control during life and can amend or revoke it.

A dynasty trust is different in a very important way. It is generally irrevocable. That means the person creating it gives up direct ownership and accepts a more formal structure. In exchange, the trust may offer stronger long-term protection, more disciplined control over distributions, and potential tax advantages when properly designed.

If you'd like a broader foundation on this category of planning, this guide to an irrevocable trust in Texas helps explain why families use irrevocable structures in the first place.

What the trust actually does

A dynasty trust usually has three moving parts:

Assets go in

The family transfers selected assets into the trust.A trustee manages them

The trustee follows the trust terms and Texas fiduciary principles, not personal preference.Beneficiaries receive controlled support

Children, grandchildren, and later descendants may receive distributions for approved purposes under the trust's rules.

A common point of confusion for readers is that beneficiaries can benefit from the trust without owning the trust property outright. That distinction matters because legal ownership, control, and access are not the same thing.

Practical rule: If a family wants maximum flexibility for the creator, a revocable trust may be the better fit. If the family wants long-term protection and multigenerational control, an irrevocable dynasty trust may be the better tool.

Why high-net-worth families use it

The basic purpose is preservation. A dynasty trust tries to prevent wealth from being broken apart by repeated transfers, unmanaged distributions, and family disruptions. It can also serve as a governance document, setting expectations for who manages wealth, how beneficiaries are supported, and how family priorities carry forward.

That's why the phrase “dynasty trusts in Texas: what high-net-worth families use” points to a real planning distinction. This is not a standard estate plan for every household. It's a specialized structure for families who need long-term asset management, protection, and continuity.

The Texas Advantage Why Dynasty Trusts Thrive Here

Texas became much more attractive for dynasty trust planning when state law changed in a meaningful way. Texas's modern dynasty-trust regime changed materially on September 1, 2021, when a revised law allowed certain trusts to last for up to 300 years from the trust's effective date, while preserving a separate 100-year limit for real property assets held in trust, as explained in this discussion of the 2021 Texas dynasty trust law change.

Why that change matters

Before that shift, long-term trust planning in Texas was more constrained. After the change, Texas families gained a much stronger in-state option for extended multigenerational planning. That matters for families who prefer to work within Texas law, use Texas fiduciaries, and keep trust administration connected to their home state.

The law also uses an effective-date framework that depends on how the trust comes into being. For a lifetime irrevocable trust, the effective date is the date of creation. For a will or living trust that becomes operative at death, the effective date is the date of death. That detail sounds technical, but it can affect how the trust term is measured and how counsel drafts the plan.

The real property point that families shouldn't miss

Texas did not remove all limits. The separate 100-year limit for real property assets is an important planning check.

That creates a practical issue for families with concentrated land holdings, ranch property, commercial buildings, or other real estate interests. The trust may still be a powerful planning tool, but the lawyer drafting it has to account for real estate rules and think carefully about how different asset classes are held.

A simple comparison helps:

| Asset type | Texas long-term planning point |

|---|---|

| Operating businesses and investment assets | Often central to long-duration dynasty planning |

| Real property assets | Subject to the separate 100-year limit described above |

Why Texas families often prefer a Texas solution

Families usually don't want a trust plan that works only on paper. They want one that fits their business operations, family relationships, and legal team. A Texas-centered structure can make trustee selection, administration, beneficiary communication, and future dispute resolution more practical.

That's one reason the 2021 law mattered so much. It gave Texas families a stronger way to pursue multi-generational planning without immediately looking outside the state.

Core Benefits for High-Net-Worth Texas Families

The strongest case for a dynasty trust usually rests on three ideas. It can improve long-term transfer-tax planning. It can create a layer of protection between family wealth and outside claims. And it can help a family write durable rules for how wealth is used over time.

Tax planning over generations

The core tax engineering behind a dynasty trust is the generation-skipping transfer tax exemption. With the current federal exemption at $13.61 million per person, a married couple can potentially shield over $27 million, plus all future appreciation on those assets, from estate and GST taxes for the entire 300-year term of the trust in Texas, as described in Schwab's dynasty trust overview.

That's a major reason affluent families pay attention to this strategy. If a properly structured trust receives GST exemption allocation and future appreciation occurs inside the trust structure, later growth may stay outside the taxable estates of children and grandchildren.

This section of planning often overlaps with broader family wealth design. Families reviewing concentrated assets, transfer plans, and succession issues often also explore estate planning for high-net-worth families as part of the same process.

A short explainer may help if you'd like to hear the concept discussed in another format.

Protection from creditors and family disruption

A dynasty trust also changes who owns the asset. Beneficiaries may receive support, but they don't hold the property in their own names. That can make a practical difference when a beneficiary faces creditor pressure, litigation exposure, or a divorce.

No lawyer should promise absolute protection in every circumstance, because outcomes depend on trust language, administration, and facts. But a carefully designed trust can create a meaningful legal barrier that an outright inheritance does not provide.

Families often assume “my child inherited it” and “my child owns it personally” mean the same thing. In trust planning, they don't.

A governance tool, not just a tax tool

Some of the most effective dynasty trusts are drafted around family purpose, not just tax rules. A trust can encourage education, support entrepreneurship, preserve a family business, assist a beneficiary with health needs, or promote responsible financial habits.

That kind of planning works best when the trust document answers real-world questions such as:

- Who decides on distributions: Is the trustee given broad discretion, or are standards tighter?

- What the money is for: Education, health, support, business opportunities, or other family priorities.

- How family leadership continues: Some families add trust protectors, advisory roles, or successor trustee structures.

Why this tool tends to serve substantial estates

Professional commentary consistently describes dynasty trusts as a planning tool for high-net-worth families because the structure is designed to preserve significant assets across multiple generations while reducing repeated transfer-tax exposure. It is most relevant where the family has enough wealth to justify long-term trustee administration, governance, and compliance, as discussed in this Texas-focused analysis of 300-year dynasty trusts.

That point matters. A dynasty trust can be powerful. It can also be more structure than a smaller or simpler estate needs.

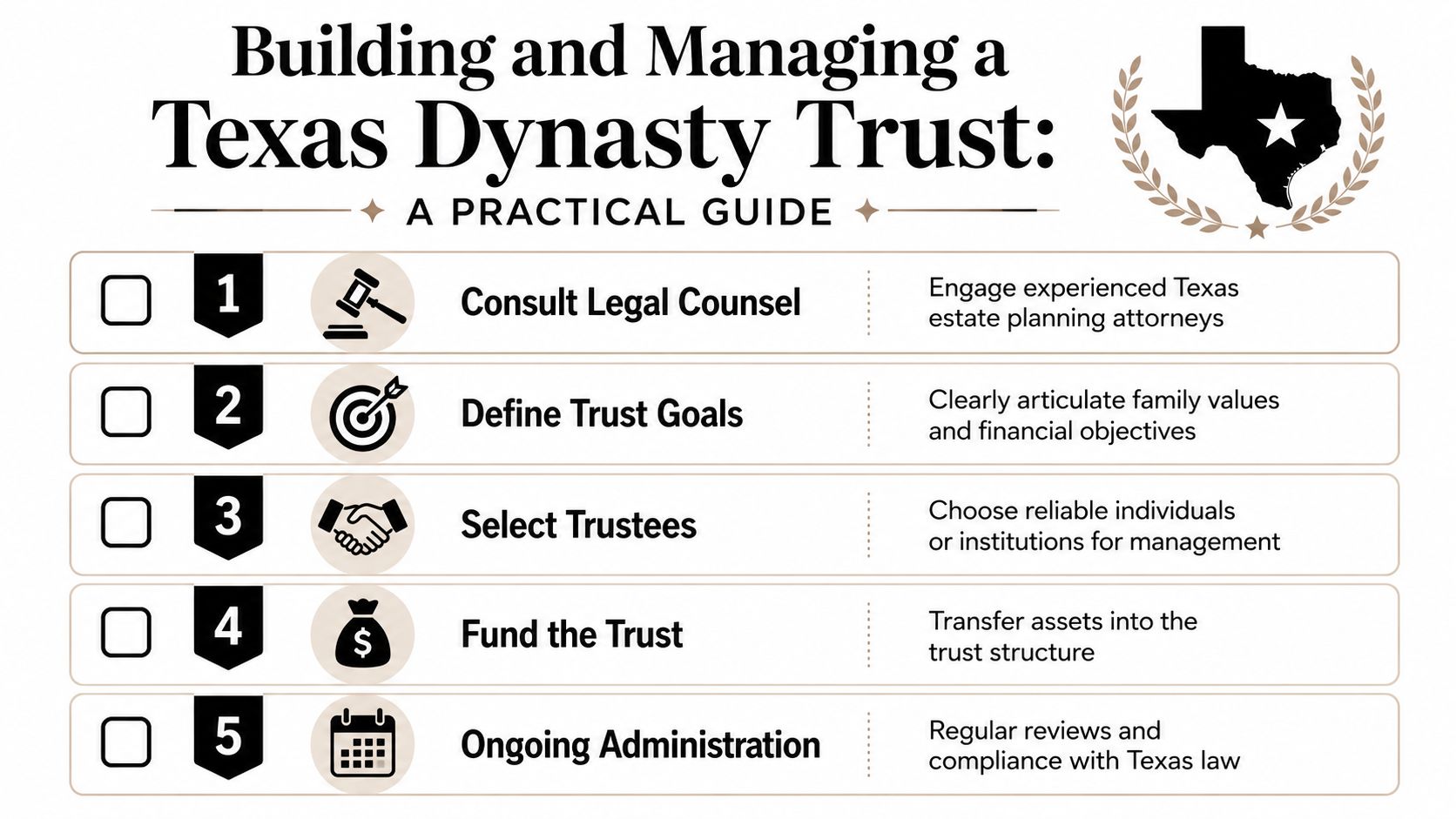

Building and Managing a Texas Dynasty Trust

A Texas dynasty trust is built in two stages. First, you design the rules. Then you choose the people and processes that will keep those rules working long after the person who created the trust is gone.

That distinction matters. A beautifully drafted trust can still fail in practice if the wrong assets go in, the wrong trustee is chosen, or no one sets expectations for how decisions will be made over time.

Start with the assets, not the paperwork

Families often focus first on signing documents. The stronger approach is to begin with the property itself.

Ask which assets belong in a long-term trust. Closely held business interests, investment accounts, and some real estate can be good candidates. Other assets may create avoidable friction because they are hard to value, hard to manage, or likely to trigger conflict among beneficiaries. A ranch, for example, may carry emotional value, operating costs, and competing views about whether it should be preserved, leased, or sold.

Funding choices also affect taxes, control, and administration. Families sorting through those issues can review this Texas-specific discussion of tax strategies for Texas trusts before making transfer decisions with legal and tax advisors.

Choose a trustee with staying power

The trustee's job is part manager, part referee, and part recordkeeper. Under the Texas Trust Code, that role carries fiduciary duties. The trustee must follow the trust terms, act loyally, invest and distribute prudently, keep records, and communicate when required.

For a trust meant to last for generations, continuity matters as much as good judgment today.

| Trustee option | Practical considerations |

|---|---|

| Individual trustee | May understand the family history well, but can face conflicts, fatigue, health issues, or pressure from relatives |

| Corporate or professional trustee | Offers continuity, systems, and consistent administration, but families should evaluate fees, responsiveness, and how the institution handles discretion |

| Co-trustee structure | Can combine family knowledge with professional discipline, if the trust clearly divides authority and resolves deadlocks |

A useful way to view this choice is simple. You are not only picking who makes the next distribution decision. You are picking the decision-making system your grandchildren may inherit.

Draft the rules so they work in real life

Texas families can make a dynasty trust much more than a tax device. The trust agreement can become a family governance document.

The distribution standard is a good example. A broad standard may give the trustee room to respond to changing needs. A narrower standard may reduce conflict by giving everyone a clearer rulebook. Neither is automatically better. The right choice depends on the family, the asset base, and how much discretion the grantor wants future trustees to have.

Other drafting tools often matter just as much:

- Powers of appointment: These can give future flexibility without handing a beneficiary full control.

- Trust protector or advisory roles: These can add oversight, help replace trustees, or address future changes in family circumstances.

- Succession provisions: These spell out who steps in when a trustee resigns, dies, or becomes unable to serve.

- Standards for special assets: Family businesses, mineral interests, ranch property, and concentrated stock positions often need custom instructions.

Texas families should pay close attention here because the trust has to fit with the rest of the estate plan. Wills, beneficiary designations, entity agreements, and probate strategy all need to point in the same direction. If they do not, the trust can be underfunded or burdened with preventable disputes.

The 2021 Texas law that opened the door to much longer trust duration changed the planning conversation in a significant way. It gave families more room to build structures that can last well beyond children and grandchildren. That longer runway makes governance design more important, not less. If a trust may last for centuries, the rules for replacing trustees, handling disagreement, and adapting to future family conditions deserve careful attention at the front end.

Keep administration practical

Long-term trusts require maintenance. They work more like a well-run family enterprise than a document stored in a safe.

Good administration usually includes:

- Regular review of trustee performance and fees

- Clear communication with beneficiaries about process and expectations

- Coordination with accountants and tax advisors

- Periodic review of family changes, including marriages, divorces, disability, and business transitions

- Attention to Texas fiduciary standards and recordkeeping

Families also ask whether a dynasty trust can be changed later. Sometimes yes, sometimes no. The answer depends on the trust language, Texas law, the interests of the beneficiaries, and the reason for the change. That is why careful drafting matters so much at the beginning. A long-term trust should be sturdy, but it should not be rigid in ways that create unnecessary trouble for future generations.

Real-World Scenarios for Texas Families

A dynasty trust becomes easier to understand when you see how it works in family life.

The Houston business owner

A Houston founder built a valuable private company and wants the business to remain in the family without becoming a source of conflict. She doesn't want each generation to inherit shares outright and then make independent decisions that pull the company in different directions.

Her dynasty trust holds noncontrolling interests for descendants. The trustee follows a detailed distribution standard. Beneficiaries can receive support for health, education, and major life needs, but they can't force a liquidation just because they want cash. The trust document also gives future decision-makers a framework for handling votes, management transitions, and beneficiary expectations.

The result is practical, not magical. The company still needs strong leadership. But the ownership structure is less likely to splinter with each generation.

The Dallas family with a large investment portfolio

A Dallas couple has substantial marketable securities and wants to create a family safety net that lasts well beyond their children. Their concern isn't just tax exposure. It's behavioral risk. They want descendants to have access to support without treating inherited wealth as a checking account.

The trust is drafted with measured discretion. A professional trustee manages investments and distributions. The family writes in guidance that supports education, responsible business ventures, and health-related needs. Beneficiaries receive meaningful support, but the principal stays protected inside the trust structure.

This is often where fiduciary duties in Texas matter most. The trustee must act according to the trust terms and cannot merely respond to whichever beneficiary applies the most pressure.

The Austin tech family planning around future growth

An Austin entrepreneur expects significant appreciation in company-related assets and wants to move selected value out of the taxable estate while also creating a long-term family framework. The family doesn't want future generations making major financial decisions without oversight.

A dynasty trust can fit that profile because it allows the family to transfer selected assets into a long-term vehicle, assign management responsibility to a capable trustee, and set rules for future distributions. That structure can be especially helpful when a family wants to support descendants generously while still preserving discipline around access, timing, and purpose.

The strongest dynasty trust plans usually reflect a family's actual concerns. Business continuity, beneficiary maturity, marriage risk, and stewardship are often more important than abstract legal theory.

Is a Dynasty Trust the Right Choice for Your Family

A dynasty trust is powerful, but it isn't automatic. Some families need flexibility more than long-term control. Others don't want the cost, structure, or administrative commitment that comes with a trust designed to last for generations. In those cases, a simpler irrevocable trust, a revocable trust combined with strong downstream planning, or generation-specific trusts may fit better.

The right question isn't whether dynasty trusts are complex. The right question is whether your family needs this level of long-term design.

A good candidate usually wants more than a tax result. They want a framework for managing wealth across generations. They care about trustee quality, family governance, beneficiary protection, and preserving assets without handing out unrestricted ownership. They also understand that trust planning works best when integrated with probate planning, asset protection, business succession, and, where needed, guardianship planning for vulnerable loved ones.

If that sounds like your situation, a thoughtful review can clarify what belongs in the trust, who should manage it, and whether a dynasty structure is the best fit under Texas law.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.