Skip to content

Skip to content A lot of Texas families first learn how complicated mineral ownership is after a death, not before. A parent or grandparent passes away, the family finds old deeds from multiple counties, royalty checks keep arriving, and nobody is fully sure who has the right to sign a lease, collect income, or make decisions for the next generation.

That uncertainty creates stress quickly. One child wants to sell. Another wants to hold. A surviving spouse wants stability. A trustee is trying to do the right thing but is worried about missing a tax filing or signing the wrong document. In many families, the minerals matter financially, but they also carry emotional weight. They represent land, history, and the work of prior generations.

That’s why the conversation about mineral rights in trust texas is really a conversation about stewardship. A trust can bring order to assets that are otherwise easy to divide, delay, or dispute. It can also give one clear decision-maker a legal framework for managing royalties, lease negotiations, and distributions under the Texas Trust Code and, when death has already occurred, in coordination with the Texas Estates Code.

A good plan doesn’t just transfer property. It reduces confusion, protects beneficiaries, and preserves family advantage. If you’re a mineral owner, a trustee, an executor, or a beneficiary trying to understand what comes next, the law is complex, but the path forward can still be clear.

An Introduction to Managing Texas Mineral Wealth

A common situation goes like this. Three siblings inherit interests tied to family land in West Texas, but the ranch itself was divided years ago. One sibling owns part of the surface, all three inherited some mineral interests, and royalty checks are being paid under old lease terms that nobody has reviewed in years.

The family isn’t just asking, “What do we own?” They’re asking harder questions. Who signs future leases. Who keeps records. Should income be distributed now or held back for taxes and maintenance. And how do they keep these assets from splintering even further when the next generation inherits?

Under Texas law, those questions matter because mineral interests are treated as real property and can be separated from the surface. That makes them valuable, but it also makes them easy to mishandle if the ownership records, trust terms, and fiduciary duties don’t line up.

Why families turn to trusts

A trust gives structure where informal family understandings usually fail. It can name a trustee, define who benefits, and set rules for lease decisions, accounting, and succession if the original decision-maker dies or becomes incapacitated.

For many Texas families, the trust is less about paperwork and more about peace. Instead of forcing heirs into repeated probate proceedings or scattered decision-making, the trust creates continuity.

Families rarely argue because minerals are unimportant. They argue because the asset is important and the instructions are unclear.

The right legal framework can reduce that pressure. It can also help a family separate two issues that often get mixed together: honoring a legacy and administering an asset responsibly.

What Are Mineral Rights in Texas

A Texas family may own a ranch, pay the taxes, maintain the fences, and still learn that someone else owns what lies beneath the soil. That surprise is common. Under Texas law, mineral rights can be owned separately from the surface, transferred separately, and placed into a trust separately.

The easiest way to understand the split is to picture the same tract as two distinct property layers. The surface estate covers the land people can use and see. The mineral estate covers the oil, gas, and other minerals below ground, along with certain legal rights tied to developing them. Those layers can stay together, or they can be divided by deed, inheritance, or sale.

That distinction matters because a trustee cannot manage what the trust does not own. Families often say, "the trust holds the land," when the title records show a different story. Sometimes the trust owns only royalties. Sometimes it owns leasing authority. Sometimes the minerals were reserved out decades earlier and never made it into the estate at all.

The mineral estate and the surface estate

Once mineral rights are severed from the surface, each interest follows its own chain of title. Over time, those chains can become difficult to trace because they pass through old deeds, probate files, leases, assignments, and trust transfers recorded in different years.

For estate planning purposes, that creates three practical questions.

- What was conveyed: A deed may transfer the ranch but reserve all minerals to the seller.

- What was funded into the trust: A trust agreement may mention mineral assets, but title must still be transferred correctly.

- What authority comes with the interest: Ownership of income is different from ownership of leasing power.

A trustee who skips those questions can make expensive mistakes. For example, signing a lease without the executive right can trigger conflict with beneficiaries and operators. Distributing income without confirming whether payments are royalty, bonus, or delay rental can create accounting problems and tax confusion.

The main types of interests people confuse

"Mineral rights" is a useful shorthand, but it is not precise enough for trust administration. The exact interest controls what the trustee may do, what beneficiaries may receive, and what long-term value the family is preserving.

| Interest type | What it usually means | Why it matters in a trust |

|---|---|---|

| Mineral interest | Ownership that may include the right to lease, receive bonuses, and receive royalties | The trustee may need clear authority to negotiate leases and balance present income against future value |

| Royalty interest | A passive right to receive a share of production income | The trustee’s job is often collection, accounting, and fair distributions rather than lease negotiation |

| Executive right | The power to sign an oil and gas lease | This power carries fiduciary risk because lease terms can affect multiple family branches for years |

| Overriding royalty interest | An income interest carved out of a lease rather than full mineral ownership | The trustee must track the lease carefully because the income may end with that lease |

Here is where families often get tripped up. A royalty interest may send checks, but it does not necessarily let the trustee sign a new lease. An executive right may let the trustee sign a lease, but that authority should be exercised with care because one decision can shape income, taxes, and family expectations for a long time.

That fiduciary piece deserves attention. Mineral assets are not just investment entries on a balance sheet. They are often inherited property tied to a family story, a ranch, or a grandparent’s planning decisions. A trustee has to treat them as both economic assets and legacy assets, which means keeping good records, acting impartially, and making decisions that can be explained clearly to current and future beneficiaries.

A useful comparison comes from trust disputes in other contexts. The legal principles differ by jurisdiction, but the underlying lesson is familiar: when one person controls property for the benefit of others, clarity about duties and ownership prevents misuse. This expert guide on constructive trusts for businesses illustrates why trust law so often turns on who holds authority, who benefits, and what records prove the arrangement.

Practical rule: Before a trustee leases, sells, distributes, or even values a mineral asset, confirm the exact interest owned, the title history behind it, and the powers granted under the trust.

That work may feel slow at first. It saves families from much harder problems later.

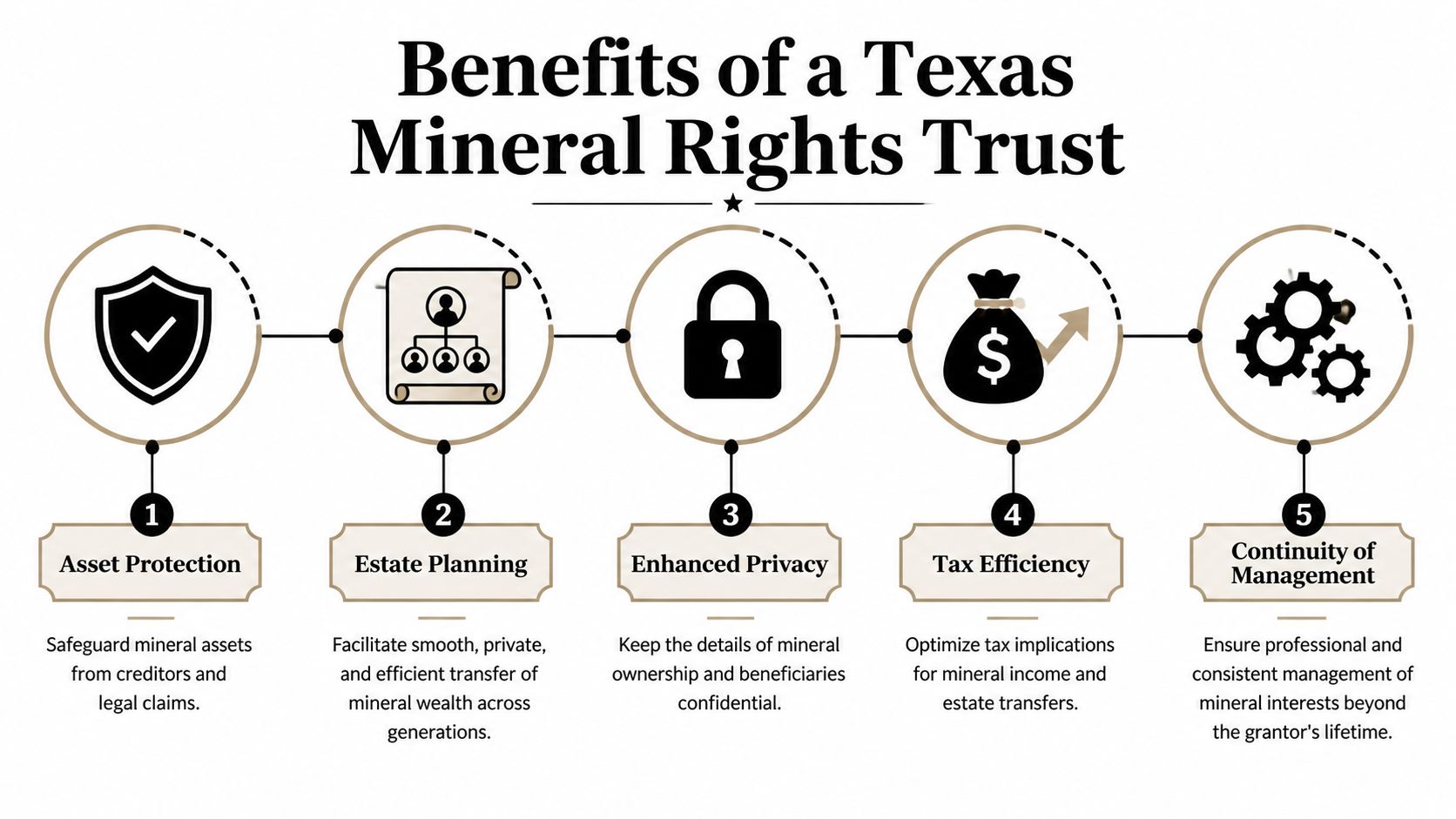

Why Place Mineral Rights in a Texas Trust

Owning mineral rights individually can work for one person. It often stops working well by the second or third generation. Each probate divides control, paperwork grows, and operators may end up dealing with many heirs who disagree about whether to lease, sell, or hold.

A trust helps keep the asset under one management structure. That gives the family continuity, which is often more valuable than people realize until a decision has to be made quickly.

A trust keeps management from becoming a family contest

When minerals pass outright to multiple heirs, each owner may have a voice, but nobody may have clean authority. That can slow lease negotiations, delay title work, and create resentment among relatives who feel excluded or overruled.

A trust changes that by naming a trustee and setting instructions in advance. The trustee doesn’t act based on family pressure. The trustee acts under fiduciary duties in Texas, the trust document, and applicable state law.

That structure can help in several ways:

- Continuity after death or incapacity: The successor trustee can step in without the family rebuilding authority from scratch.

- Private administration: Trust management is generally more private than a public probate file.

- Centralized decision-making: Operators, landmen, accountants, and beneficiaries know who is authorized to act.

- Preservation of negotiating power: Keeping interests together may improve the family’s ability to negotiate consistently.

The Texas Trust Code gives trustees tools

Texas trusts aren’t just containers for ownership. They operate within a legal system that gives trustees authority and imposes duties. One important feature is that trusts holding Texas mineral rights benefit from legal protections under the Texas Trust Code, including recovery of unpaid royalties with statutory interest, as discussed in this analysis of Texas mineral trusts and fiduciary protection.

That matters because royalty administration is not always simple. Payments can be delayed, misdirected, suspended, or questioned. A trustee needs both authority and a legal framework for enforcing the trust’s rights.

Why families choose trusts for legacy planning

Families usually don’t create mineral trusts just to avoid paperwork. They create them because they want to preserve options.

One family may want income for a surviving spouse and long-term ownership for children. Another may want a professional or neutral trustee to avoid sibling conflict. Another may want the trustee to hold minerals for years and distribute only income, not the underlying asset.

A trust can be drafted to match those goals far better than informal co-ownership.

A mineral trust works best when it answers the family’s real questions in advance. Who decides, who benefits, who gets information, and what happens when the market or the family changes.

Trusts can also support asset protection thinking

Some clients who hold business interests, mineral assets, and real estate want to think more broadly about how fiduciary structures can protect property and recover misapplied assets. For readers interested in a comparative perspective, this expert guide on constructive trusts for businesses offers a useful look at how trust concepts can be used to address control and recovery problems in another legal context.

The legal systems are different, but the underlying concern is familiar. Valuable assets need clear control, accountability, and enforceable duties.

When a trust is especially helpful

A Texas trust often makes the most sense when any of these conditions apply:

- The family owns minerals in more than one county

- Several heirs are involved

- The owner wants to avoid repeated probate administration

- A beneficiary is too young, vulnerable, or inexperienced to manage lease and royalty issues alone

- The family wants professional management and regular accounting

- The owner wants a long-range legacy plan instead of one transfer at death

For many families, the biggest benefit is simple. The trust turns a difficult inherited asset into an organized plan.

A Trustee’s Responsibilities for Mineral Assets

A daughter becomes trustee after her father dies. A landman calls about a lease amendment. One sibling wants to sign right away because the bonus sounds good. Another thinks the family should wait. Royalty checks have started, but no one is sure whether the trust holds the full mineral interest or only a share. That is a common Texas trust moment. The trustee is suddenly standing between legal duties, family expectations, and an asset that can keep paying for decades if it is handled with care.

Mineral interests ask more of a trustee than a bank account or a brokerage statement. They are part property title, part income stream, and part family legacy. A trustee has to protect the asset, treat beneficiaries fairly, and make decisions that can be explained years later if anyone questions them.

Under the Texas Trust Code, a trustee owes duties of loyalty, prudence, disclosure, and proper administration. Related estate and title issues can still matter if the minerals reached the trust through an estate or if ownership was never cleaned up after a prior death. In practical terms, the trustee must act for the beneficiaries, avoid self-dealing, and manage the property with the care a responsible person would use for someone else’s property.

Start with title, authority, and the trust terms

Before signing a lease, division order, ratification, or deed, the trustee should answer three basic questions.

What does the trust own?

The interest may be minerals, royalties, executive rights, nonparticipating royalty interests, or a combination. Those rights are related, but they are not the same. A trustee cannot make a sound decision without knowing which sticks in the bundle the trust holds.Was the asset properly transferred into the trust?

Families are often surprised here. A schedule attached to a trust may show intent, but the county records may tell a different story if no deed or assignment was signed and recorded.What powers does the trust document give the trustee?

Some trusts clearly allow leasing, pooling, settling claims, hiring landmen, and retaining a concentrated mineral position. Others are narrower. The trustee’s authority begins with the instrument, not with family consensus.

This review does more than prevent paperwork mistakes. It keeps the trustee from acting outside the role the grantor created.

Administration means records and judgment

Trustees sometimes expect mineral administration to be clerical. Part of it is. Much of it is judgment.

On the records side, the trustee may need to review deeds, confirm decimal interests on division orders, match royalty payments to check detail and production statements, save tax forms, and keep correspondence in a file that makes sense to someone other than the trustee. Good files matter because memories fade, family stories change, and a later trustee may need to reconstruct why an earlier decision was made.

On the judgment side, the trustee has to decide what serves the beneficiaries as a group. That may mean comparing lease offers, deciding whether to sell or hold, setting aside reserves for taxes and expenses, or choosing how much information to share and when. A trustee does not have to produce the best result in hindsight. A trustee does have to use a careful process, ask the right questions, and document the reasons for the decision.

A helpful way to view the job is this. The trustee is not just collecting checks. The trustee is serving as steward of a wasting asset that may support children, grandchildren, and family relationships long after the original owner is gone.

Leasing decisions require a fiduciary lens

If the trust holds the executive right or leasing authority, the trustee may be asked to sign oil and gas leases, amendments, pooling clauses, surface use agreements, or ratifications. Those documents can shape income and risk for years. Common forms are still legal contracts, and small wording changes can shift real money from the family to the operator.

The trustee should closely review items such as:

- Primary term and extension rights

- Royalty language

- Post-production cost provisions

- Pooling authority and unit size

- Shut-in royalty terms

- Continuous development clauses

- Surface protections, if the trust also owns surface rights

- Warranty language and indemnity risk

Beneficiaries often approach these choices from different angles. An income beneficiary may prefer a quick lease and current cash flow. A remainder beneficiary may care more about stronger long-term terms and protection against overdevelopment. The trustee cannot only follow the most vocal relative. The trustee must weigh the trust’s purposes, the terms of the instrument, and the interests of all beneficiaries.

For a closer look at the practical issues trustees face with leasing, royalties, and title review, see this discussion of oil and gas interests held in a Texas trust.

Royalty handling and tax reporting are common trouble spots

Mineral assets produce confusion because the money arrives in different forms and at different times. A lease bonus is not the same as a monthly royalty check. Suspense payments, adjustments, and operator deductions can make the accounting even harder. Beneficiaries often assume that if cash came into the trust, it should be distributed immediately. Trust accounting does not always work that way.

The trustee may need to:

| Trustee task | Why it matters |

|---|---|

| Verify royalty receipts | The payor’s decimal interest and payment history should match the trust’s ownership records |

| Separate income from principal for fiduciary accounting | Allocation affects fairness between current and future beneficiaries |

| Coordinate early with a CPA | Mineral reporting errors are easier to prevent than to correct after returns are filed |

| Keep support for every allocation and reserve | A later accounting request may turn on details the trustee can no longer recreate from memory |

This part of the job carries a human side too. If one beneficiary depends on distributions and another is focused on preserving value, even a correct accounting choice can feel personal. Clear explanations reduce the chance that a technical tax issue turns into a family conflict.

Communication is part of the duty

A trustee does not need beneficiary permission for every routine act. The trustee usually does need regular, even-handed communication. Silence often gets interpreted as favoritism, secrecy, or neglect, especially when the asset came from a parent or grandparent and carries emotional weight beyond its market value.

Helpful habits include annual accountings, plain-English summaries of major decisions, prompt responses to reasonable questions, and consistent treatment of all beneficiaries. If one beneficiary receives lease documents or payment explanations, others should not be left in the dark without a valid reason.

That discipline protects more than the trustee. It protects the family story around the asset. A well-run mineral trust can preserve wealth across generations. A poorly explained one can leave lasting resentment, even if the royalties were substantial.

For trustees dealing with grief, sibling tension, and unfamiliar oil-and-gas paperwork, feeling overwhelmed is normal. Getting legal and tax advice early is often the difference between orderly administration and a dispute that could have been avoided.

Tax and Estate Planning for Mineral Rights

Mineral rights can produce several kinds of economic value, but they don’t all get treated the same way. Lease bonuses, royalty income, and sale proceeds may trigger different tax questions. Trustees and families also have to think about whether the asset should remain in a revocable trust, move into an irrevocable trust, or pass through an estate first.

That’s where tax planning and estate planning stop being separate conversations. With minerals, they’re tied together.

Royalties, bonuses, and depletion

A trustee or mineral owner should understand the character of the payment before deciding how to report it or distribute it.

- Royalty income is commonly treated as income from production.

- Lease bonuses arise when an owner grants a lease.

- Depletion rules may affect taxable income tied to oil and gas interests.

The trust document should also address how these receipts are allocated for fiduciary accounting purposes. Beneficiaries often assume “money in” means “money out,” but that’s not always how trust law works. A trustee may need to retain funds for taxes, expenses, reserves, or principal allocation.

Why irrevocable trusts get serious attention

For some families, especially those focused on preserving wealth over generations, an irrevocable trust deserves a close look. According to Texas trust planning guidance on mineral interests, placing severed mineral rights into irrevocable trusts can preserve 30-50% more value over 10 years versus probate, while also helping shield assets from partition sales under Texas Property Code §23.001.

That doesn’t mean every family should use an irrevocable trust. It does mean the decision is often worth a careful review when the minerals are significant, the family wants continuity, or the owner is concerned about future fragmentation.

For readers exploring this issue further, guidance on tax strategies for Texas trusts can help frame the discussion you’ll want to have with both legal counsel and a CPA.

Tax planning for mineral interests works best when the attorney, CPA, and trustee are talking before a lease is signed or a distribution is made.

Estate planning choices affect control

A will can pass mineral rights. So can a trust. But the control features are different.

A will speaks at death and often requires probate administration under the Texas Estates Code. A trust can define management rules during life, during incapacity, and after death. That continuity is often the deciding factor when the family wants one person or one institution to keep handling minerals without interruption.

This overview gives a useful visual introduction to the planning issues families often face with trust-based wealth transfer:

Questions families should ask early

Instead of starting with tax jargon, start with practical questions:

- Will these minerals stay in the family for multiple generations

- Does one beneficiary need income more than others

- Is there a risk of partition, conflict, or fragmented ownership

- Should one trustee control leasing while another handles distributions

- Would an irrevocable trust better serve protection and legacy goals

Those answers shape the structure. Once the structure is right, the tax reporting is easier to manage. When the structure is wrong, even a good accountant is left cleaning up avoidable problems.

Key Provisions for a Mineral Rights Trust

A mineral trust should not read like a generic estate planning form with a few extra words added at the end. These assets have their own operational demands, and the trust should say clearly what the trustee may do, how income is handled, and what happens if disputes arise.

The drafting matters because the trustee’s authority will be tested by real documents, real payors, and sometimes real family conflict.

Powers the trustee should have in plain language

If a trust is going to hold mineral-related property, it should usually address whether the trustee has authority to:

- Execute oil and gas leases

- Sign ratifications, amendments, and pooling agreements

- Approve division orders

- Collect and settle royalty claims

- Hire landmen, accountants, and attorneys

- Sell, exchange, or retain mineral interests

- Open litigation or settle disputes when needed

Without that level of specificity, trustees may hesitate when action is needed or overstep when the trust language is too vague. Either problem can hurt the beneficiaries.

A well-drafted transfer process matters too. If the asset never makes it into the trust correctly, all the careful drafting in the world won’t solve the ownership problem. This is why families often need guidance on how to transfer property to a trust in Texas, especially when deeds, legal descriptions, and old severances are involved.

Income, principal, and discretion clauses

Mineral assets don’t behave like a savings account. They may produce irregular income, decline over time, or sit non-producing for long periods before new activity begins. The trust should address how the trustee allocates receipts and whether discretionary or mandatory distributions apply.

Helpful provisions often include:

| Provision | Why it helps |

|---|---|

| Allocation language | Helps the trustee separate principal and income in a consistent way |

| Reserve authority | Lets the trustee hold back funds for taxes, legal fees, or future expenses |

| Discretionary distribution standard | Gives flexibility when income is uneven |

| Successor trustee language | Prevents gaps in authority if the current trustee can’t serve |

Surface conflict planning belongs in the document

One of the most important issues in Texas mineral trust drafting is surface use. In Texas, the mineral estate dominates the surface estate, which means trustees should proactively address surface use agreements to reduce disputes and liability, as explained in this discussion of Texas mineral rights and surface conflicts.

That principle can surprise families. A trust may hold minerals, surface, or both. If the trustee ignores the relationship between those interests, family friction can build fast, especially where a ranch, farm, or home site is involved.

If the trust may ever deal with both surface and mineral concerns, the drafting should tell the trustee how to balance production value against protection of the land and family relationships.

Family-focused provisions that are easy to overlook

Some of the most useful clauses are not technical oil and gas provisions. They are practical governance provisions.

Consider whether the trust should include:

- A communication standard so beneficiaries receive periodic reports

- A dispute-resolution clause to encourage early resolution before litigation

- A trustee replacement mechanism if the family loses confidence in the current trustee

- Specific authority for digital and paper recordkeeping

- Instructions on whether to hold or sell long-term

These clauses don’t eliminate every disagreement. They do make the trust easier to administer and harder to misunderstand.

Common Disputes Involving Mineral Trusts and How to Avoid Them

Most disputes around mineral trusts don’t begin with fraud. They begin with uncertainty, poor communication, or assumptions that were never written down. By the time the family calls a lawyer, the issue usually feels personal even when the root problem is administrative.

Three common conflict patterns

One common dispute involves leasing decisions. A trustee wants to sign a lease, but one beneficiary believes the family should wait for better terms. If the trust gives the trustee clear authority and the trustee explains the reasoning in writing, that disagreement may stay manageable. If the trustee acts informally and leaves no record, the same decision can look suspicious later.

A second dispute grows out of uneven information. One sibling speaks with the operator, sees the check detail, and assumes that makes them the practical decision-maker. The others begin to think the trustee is favoring one branch of the family. A regular accounting and uniform communication policy usually helps prevent that.

A third dispute arises when surface and mineral interests collide. A beneficiary who lives on or uses the land may feel that mineral development is damaging the property or family lifestyle. That is where thoughtful administration and, in some cases, related planning for vulnerable family members through guardianship and protective proceedings in Texas can become part of the broader solution.

Prevention usually looks unglamorous

Families often hope there is a single magic clause that prevents litigation. There usually isn’t. Disputes are more often avoided through steady habits:

- Write down decisions: Keep minutes, memos, and correspondence.

- Explain the trustee’s reasoning: Beneficiaries don’t have to agree, but they should understand.

- Follow the trust strictly: Don’t improvise when the document gives direction.

- Use professionals when needed: Title, tax, and lease issues often need separate expertise.

Many trust disputes could have been avoided if someone had sent a clear letter, attached the key documents, and kept a clean accounting.

When conflict is already developing

If a beneficiary is asking for records, challenging a lease, or alleging self-dealing, don’t treat it as a personality problem alone. Review the trust, gather the documents, and address the complaint directly. Early legal review is often far less costly than trying to reconstruct years of decisions after everyone has stopped trusting each other.

Your Action Plan for Securing Mineral Wealth

A common family meeting starts this way. A parent wants the minerals to stay in the bloodline, one child is willing to serve as trustee, and another only wants to know whether the royalty checks will keep coming. Everyone is talking about the same property, but each person has a different legal job. A good plan brings those roles into focus before confusion turns into conflict.

If you are dealing with mineral rights in trust texas, start by identifying your role first. A settlor decides the rules. A trustee carries them out. A beneficiary has rights to information and, depending on the trust, rights to distributions. That distinction matters because the next smart step is different for each person.

If you’re creating the trust

Start with the paper trail. Gather deeds, royalty statements, division orders, lease files, probate records, and any prior trust documents. Mineral ownership often passes through several generations, and a missing deed or an old probate can create uncertainty later.

Then get clear about your purpose. Some families want steady income. Others want to preserve the asset for children and grandchildren, even if that means limiting present distributions. Some want a structure that reduces the chance of family pressure, uneven treatment, or rushed sales. Your trust should reflect those goals in plain terms.

The choice of trustee deserves special care. For mineral assets, the trustee is not just a bookkeeper. The trustee is the person standing between the asset and the family disputes that poor administration can create.

If you’re serving as trustee

Read the trust carefully, then read the mineral records with the same care. The trust tells you what authority you have. The property records tell you what the trust owns. If either piece is misunderstood, the trustee can make avoidable mistakes in leasing, distributions, or reporting.

Set up one organized file, digital or physical, for title documents, payment records, tax information, correspondence, and notes explaining major decisions. That file becomes the history of your administration. It also shows beneficiaries that decisions were made with care and loyalty, not guesswork.

Communication carries a lot of weight here. Beneficiaries may not object to a hard decision if they can see the reasoning, the timing, and the supporting records. A short written update at the right time often protects both the trust and the relationship.

If you’re a beneficiary

Begin with the basic question. What exactly does the trust own, and what does the trust require the trustee to do with that asset?

Then ask for the documents that answer those questions. You may need the trust terms, an accounting, or records showing income received and expenses paid. A focused request usually works better than a broad accusation. If something feels off, say what concerns you specifically, whether it is delayed distributions, missing information, or a lease decision you do not understand.

Mineral interests can preserve family wealth for a long time, but only if the trust is administered with discipline and fairness. In many families, the larger goal is not solely collecting revenue. It is preserving confidence across generations so that the asset remains a source of support rather than a source of resentment.

If your family owns Texas minerals and wants a trust structure that protects both the asset and the relationships around it, speak with a qualified Texas estate planning and trust administration attorney. Careful planning now can spare your family expensive uncertainty later.