Skip to content

Skip to content Managing a loved one’s trust can feel overwhelming, especially when the document is full of legal terms and family members are already asking questions. Many new trustees in Texas are stepping into the role during a stressful season. A parent has died, a spouse can no longer manage finances, or a family business is part of the trust and nobody is sure what happens next.

The good news is that irrevocable trust administration texas doesn't have to be guesswork. A trustee’s job is serious, but it follows a clear path. You gather the right documents, identify the assets, communicate carefully, make distributions exactly as the trust allows, and keep records that can stand up to scrutiny.

Texas law gives trustees both authority and responsibility. The Texas Trust Code and Texas Estates Code expect a trustee to act with loyalty, prudence, and fairness. That sounds intimidating at first. In practice, it means you protect trust property, follow the written instructions, and avoid making side deals or informal decisions just because they feel easier in the moment.

Many trustees get into trouble not because they meant harm, but because they moved too fast, trusted memory instead of paperwork, or tried to keep the peace by bending the trust terms. This guide is meant to slow that process down. If you’re a new trustee, a beneficiary trying to understand what the trustee should be doing, or a family member helping behind the scenes, you can use this as a practical roadmap.

Stepping into the Role of a Trustee in Texas

You may have learned you were the trustee in a phone call, at a kitchen table, or during a meeting after a funeral. Individuals typically do not respond with confidence. They respond with questions. What am I supposed to do first? Who do I call? Am I personally liable if I make a mistake?

That reaction is normal.

Serving as trustee is both an honor and a legal duty. Someone chose you because they believed you would carry out their wishes with care. In Texas, that means more than writing checks. It means managing property for other people, staying faithful to the trust terms, and acting in a way that protects both current and future beneficiaries.

A simple example helps. Suppose a mother created an irrevocable trust for her two children and named her brother as trustee. One child needs help with tuition. The other wants the trustee to hold funds back until a business sale closes. The trustee may feel pressure from both sides, but his job isn’t to pick a favorite outcome. His job is to read the trust, understand what it permits, and act accordingly.

Practical rule: Your first loyalty is to the trust document, not to the loudest beneficiary or the most urgent family request.

Texas trustees often discover that administration is less about dramatic decisions and more about disciplined follow-through. You review the terms, identify everyone affected, secure the property, and create a paper trail from the start. That steady approach reduces risk and keeps the process grounded in the grantor’s instructions. A helpful overview of the legal environment appears in this guide to Texas irrevocable trust basics.

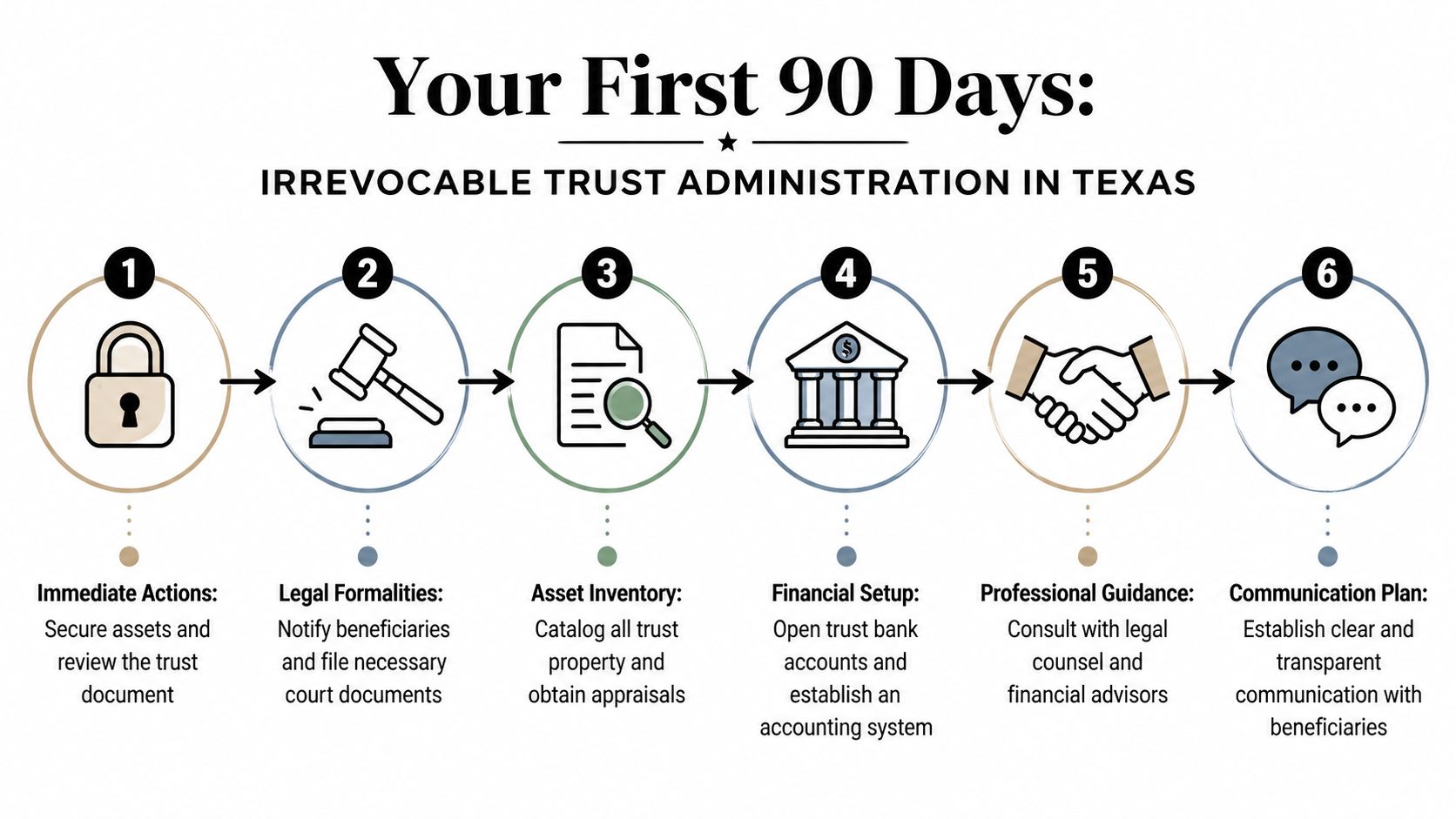

Your First 90 Days A Trustee's Initial Roadmap

The first three months often shape the rest of the administration. Early organization can prevent later disputes. Disorganization at the start tends to multiply.

Start with the trust document and supporting records

Before you move assets or answer beneficiary questions, read the trust itself. Then read it again with a pen in hand. You’re looking for the parts that control real-world decisions:

- Trustee powers: What can you sell, invest, distribute, or delegate?

- Beneficiaries: Who has current rights, and who may inherit later?

- Distribution standards: Is the trust mandatory, discretionary, or tied to a specific event?

- Successor trustee language: Were you properly appointed, and what proof do banks or title companies need?

- Special instructions: Family business rules, real estate restrictions, or tax-sensitive provisions

Don’t stop with the trust agreement. Gather amendments, schedules of property, deeds, account statements, insurance records, prior tax returns, and any letters of wishes the grantor left behind. If the trust owns hard-to-value property, such as closely held business interests, appraisals may be necessary so you know what the trust holds.

A new trustee also needs to identify not just obvious beneficiaries, but contingent beneficiaries too. In some trusts, unborn descendants or future classes of beneficiaries matter. That affects your duty of impartiality under Texas law.

Notify the right people early

Silence creates suspicion. Beneficiaries often assume the worst when they hear nothing, even if the trustee is working hard behind the scenes.

Your notices should be prompt, clear, and dated. In practical terms, that often means telling beneficiaries that you’ve accepted the role, explaining how future communications will work, and keeping copies of everything you send. If you’re stepping in as a successor trustee, financial institutions and advisors need notice too.

Use a communication log from day one. Track the date, the person contacted, the issue discussed, and any follow-up promised. That sounds basic, but it’s one of the easiest ways to show that you acted responsibly.

According to Husch Blackwell’s trustee administration checklist, professionally managed trusts achieve 95% compliance rates versus 70% for lay trustees, and common pitfalls for new trustees include undocumented distributions and asset review oversights. That gap reflects process. Experienced trustees document first and act second.

A trustee who communicates clearly and keeps records usually looks organized to the family and credible to a court.

Secure and retitle trust assets

Once you know what the trust owns, secure it. That may include changing locks on vacant property, confirming insurance coverage, forwarding mail, or freezing informal access to accounts. If a family member has been treating trust property like personal property, this is often the moment you need to set boundaries.

Then confirm legal title. Assets should be held in the trust’s name if the trust is meant to own them. Real estate may require deed review and recording work. Brokerage firms may ask for certificates of trust, death certificates, tax identification information, or trustee acceptance documents. Life insurance and business interests require their own paperwork.

Here’s a practical first-90-days checklist:

- Read every controlling document and create a summary sheet.

- Identify all beneficiaries and note whether their interests are current or future.

- Collect asset records for bank accounts, real estate, investments, insurance, and business holdings.

- Secure property immediately so nothing disappears, lapses, or gets misused.

- Notify beneficiaries and institutions in writing and save copies.

- Create a trustee file with a calendar, contact log, accounting folder, and document index.

Build your system before making distributions

Many new trustees want to make quick payments to show progress. That can backfire if you haven’t set up the administration correctly.

Open any needed trust bank account. Separate trust money from your own money completely. Create folders for receipts, invoices, statements, notices, tax documents, and correspondence. Even a simple spreadsheet is better than relying on memory.

A basic trustee file might look like this:

| Trustee file category | What to keep |

|---|---|

| Governing documents | Trust agreement, amendments, acceptance papers |

| Beneficiary records | Names, addresses, notices, responses |

| Asset records | Statements, deeds, appraisals, business documents |

| Transaction log | Deposits, expenses, distributions, reimbursements |

| Tax file | EIN records, prior returns, annual filings |

| Communication log | Calls, emails, letters, meeting notes |

The first 90 days are about control, not speed. If you’re careful here, later decisions become easier to defend.

Prudent Management Inventory Accounting and Investments

A trust can’t be managed well until it’s measured well. That starts with inventory and valuation. Then it continues through accounting, cash management, and investment oversight.

Build an inventory you can trust

An inventory is more than a list. It’s the foundation for every future decision you make as trustee. If your inventory is incomplete, your accounting will be incomplete. If your accounting is incomplete, distributions and tax filings become much harder to defend.

For each asset, identify:

- What it is: house, ranch land, brokerage account, LLC interest, mineral rights, life insurance, cash

- How it is titled: trust name, individual name, joint ownership, transfer-on-death designation

- Its approximate value: based on statements, appraisals, or professional valuation

- Its income and expense profile: rent, dividends, maintenance, taxes, insurance

- Its restrictions: sale limitations, partnership agreements, occupancy issues, debt, liens

During administration, trustees often discover surprises. A trust may own property the family forgot about. An account might still be titled incorrectly. A closely held company may need formal valuation work before any beneficiary can be treated fairly.

Apply prudence, not guesswork

Texas trustees operate under fiduciary principles that require prudent management. In plain English, that means you must use care, skill, and caution when handling trust property. You’re not expected to predict the market perfectly. You are expected to act thoughtfully and document why you made each significant decision.

If the trust holds investments, ask practical questions. Does this portfolio fit the trust’s purpose? Does it produce income for a current beneficiary while preserving value for remainder beneficiaries? Is one risky holding dominating the entire account? Is a vacant home draining cash without a plan?

The duty of impartiality matters here. A trustee must balance competing interests when one beneficiary wants current income and another benefits from long-term growth. That doesn’t always mean equal treatment in every moment. It means fair treatment under the trust’s terms and consistent reasoning.

Trust accounting is where many trustees get stuck, especially if they’ve never managed a formal fiduciary ledger before. This overview of trust accounting in Texas can help you understand what beneficiaries and courts often expect to see.

Plan for the real cost of administration

Trust administration has ongoing costs. Some trustees underestimate that and then scramble when tax prep, professional fees, or valuation work arrives.

For a typical $1 million irrevocable trust in Texas, annual administrative costs can exceed $11,500, combining a professional trustee’s 1% fee with tax preparation expenses. Over a decade, those fees can surpass $100,000, according to this discussion of irrevocable trust costs in Texas.

That doesn’t mean every trust needs a corporate trustee. It does mean trustees should budget realistically. If the trust owns a rental property, business interests, or tax-sensitive assets, professional help may protect the trust and the trustee from costlier mistakes later.

Here’s one way to think about the cost question:

| Administrative need | Why it matters |

|---|---|

| Appraisals | Support fair valuation and reporting |

| Tax preparation | Help with annual filings and income allocation |

| Legal advice | Clarify powers, notices, distributions, and disputes |

| Bookkeeping support | Keep records organized and current |

| Investment review | Align asset management with trust purposes |

Use accounting habits that hold up under pressure

A trustee’s records should allow another person to understand what happened without relying on your memory. That means every deposit, bill, reimbursement, and distribution should be traceable.

Good month-end discipline helps. If you need a simple framework for organizing receipts and recurring financial review, this article on month end best practices from Smart Receipts is a practical reference. It isn’t trust-specific, but the habit of reconciling records regularly translates well to fiduciary administration.

Keep the ledger current while events are fresh. Reconstructing a year of trust activity after a beneficiary challenge is much harder than updating records each month.

Some trustees prefer spreadsheets. Others use QuickBooks with customized categories. Some work with a CPA or bookkeeper. The tool matters less than consistency. What matters is that your records show what money came in, what went out, who approved it, and why the transaction benefited or complied with the trust.

A short discussion of prudent trust administration can also help put these responsibilities in context:

When trustees manage inventory, accounting, and investments with discipline, they usually feel less reactive. They stop guessing. They start making decisions from a reliable record.

Fulfilling the Trust’s Purpose Distributions and Tax Compliance

A trustee often feels the pressure most when a beneficiary asks for money. The request may sound simple. A tuition bill is due. A medical expense cannot wait. A family member says, “Dad would have wanted this paid.” In that moment, your job is to slow the process down just enough to protect the trust, the beneficiaries, and yourself.

Distributions are the point where trust administration becomes visible to the family. They are also the point where good intentions can turn into personal liability if the trustee pays first and checks the trust later.

Follow the distribution language exactly

Start with the trust document, not with the request.

Some trusts require mandatory distributions at a certain age, after a death, or when another event occurs. Others give the trustee discretion to distribute money for health, education, maintenance, or support. Those two categories create very different jobs for a trustee.

If the trust says the trustee “shall distribute” income each year, that usually means you must make the distribution once the conditions are met. If the trust says the trustee “may distribute” principal for health needs, you usually need a fair process for reviewing the request and deciding whether it fits the trust’s standard.

A safe habit is to treat each distribution like a file you may need to defend later. Pull the exact clause. Match the request to that clause. Gather the papers that support the request. Then make the decision.

A careful distribution process often includes:

- Reviewing the exact clause that authorizes the payment

- Collecting supporting documents such as medical bills, tuition statements, care invoices, or a written explanation of need

- Recording the amount, date, recipient, and reason for the payment

- Giving written notice when appropriate, especially for larger or unusual distributions

- Avoiding informal advances or family “loans” unless the trust clearly permits them

Practical rule: If you cannot point to the line in the trust that supports the payment, stop and review before sending money.

Match your process to the kind of trust you are administering

In practice, trusts do not all work the same way.

A trust for a young beneficiary may call for fixed distributions in stages. If the beneficiary receives one-third at age 25, another third at 30, and the balance at 35, your task is mostly to confirm the triggering event and document the payment correctly.

A support trust is more judgment-based. One month you may review a request for rent. Another month it may be a therapy bill or tuition payment. In those cases, paying the provider directly may fit the trust better than handing cash to the beneficiary, depending on the wording and the facts.

A fully discretionary family trust often requires the most care. One beneficiary may ask for help starting a business. Another may need funds for surgery or long-term care. Your role is not to guess what feels fair in the moment. Your role is to apply the standard written in the trust consistently, explain your reasoning in the file, and avoid favoritism.

That consistency matters. Family members may accept “no” more easily when they can see there was a process.

Do not let tax deadlines sneak up on you

Many first-time trustees are surprised to learn that an irrevocable trust may be its own taxpayer. That means tax compliance is part of carrying out the trust’s purpose, not a separate administrative chore.

Most irrevocable trusts must file IRS Form 1041 if they have taxable income, $600 or more in gross income, or a nonresident alien beneficiary. This overview of irrevocable trust tax considerations and filing issues explains why trustees often need tax planning early, not just at filing time.

Texas does not impose a state income tax on trusts, which removes one layer of work. Federal reporting still requires care. Income may need to be tracked by source. Distributions may affect what the trust reports and what a beneficiary reports. A year-end decision to distribute or retain income can change the tax result.

A simple tax calendar helps:

| Tax task | Why it matters |

|---|---|

| Confirm taxpayer identification information | Needed for banking, tax forms, and reporting |

| Track income by source | Helps prepare the trust return accurately |

| Separate principal from income in your records | Supports proper accounting and tax treatment |

| Gather annual statements early | Prevents delays at tax time |

| Coordinate with a CPA or tax attorney | Reduces filing mistakes and missed deadlines |

If trust accounting feels like keeping two scoreboards at once, that is because it often is. One scoreboard tracks what the trust allows. The other tracks what the tax rules require. They overlap, but they are not identical.

Community property issues can change what looks like a simple distribution

Texas trustees need to be careful when trust assets have ties to a marriage.

If a married grantor funded the trust, or if the trust holds assets acquired during marriage, you may need to determine whether property is community property, separate property, or a mix that requires tracing. That question can affect title review, accounting, distribution decisions, and whether another person should receive notice before action is taken.

This is a common area of confusion. Placing property into a trust does not automatically erase every marital property issue. A house purchased during marriage, a brokerage account built with mixed funds, or an asset affected by divorce or death may require a closer legal review before you distribute, sell, or retitle it.

A trustee dealing with possible community property should ask:

- How was the asset acquired? Before marriage, during marriage, by gift, or by inheritance?

- How is title held now? Title helps, but it does not always answer characterization by itself.

- Were funds commingled? Mixed funds can create tracing problems.

- Does a spouse need notice or consent? The answer may depend on the trust terms and the nature of the asset.

- Could this distribution affect marital rights? If yes, pause and get legal advice before acting.

This part of the job can feel technical, but the goal is simple. You are making sure the trust distributes the right asset, to the right person, for the right reason, with a record that will hold up if anyone asks questions later.

Navigating Challenges Disputes and Trust Termination

You may reach a point where the paperwork is in order, the assets are identified, and the hardest part is no longer financial. It is human. One beneficiary believes you are taking too long. Another wants an early distribution. A third questions whether you are favoring someone else.

That moment is common for a Texas trustee, especially a family member trustee. The job can start to feel less like administration and more like trying to referee a tense family conversation while following legal instructions at the same time.

The good news is that many trust disputes grow from preventable mistakes. Uneven communication, casual promises, unclear records, and acting before your authority is clear often create more trouble than the underlying issue. A careful trustee can lower that risk.

Use communication to lower the temperature

Beneficiaries often become suspicious when they do not understand what is happening. Silence leaves room for assumptions. Inconsistent updates can look like favoritism even when none is intended.

A better approach is simple and disciplined. Treat communication like part of the administration file, not like side conversation.

Try these habits:

- Set a regular update pattern: tell beneficiaries when they should expect information

- Put key points in writing: confirm important calls by email or letter

- Explain delays: if you are waiting on tax documents, appraisals, or legal advice, say so

- Use the same process for everyone: similar requests should receive similar responses

- Pause before replying in anger: a sharp text can become an exhibit later

Good records often calm conflict because they show that your decisions came from the trust terms, not emotion.

You do not need to agree with every complaint. You do need to take concerns seriously enough to review them, respond clearly, and keep a record of what you did.

Trust changes require authority, not family consensus alone

A trustee will sometimes hear, "We all agree, so can't we just change it?" That question sounds practical. Under Texas law, the answer depends on the trust terms, the type of change requested, and the legal method available.

Some changes may be handled through a valid nonjudicial settlement agreement. Others may require court approval. Some requests are not really administrative updates at all. They are attempts to rewrite who gets what, or when, or under what conditions. That is where trustees get into trouble.

A useful way to think about this is to separate housekeeping from redesign. Updating an administrative process is one kind of issue. Changing the trust's substance is another. Both require care, but the second one carries much more risk.

Here is a practical starting point:

| Situation | Better first step |

|---|---|

| Outdated administrative terms | Ask trust counsel whether a nonjudicial agreement may be available |

| Tax concerns | Review the issue with both trust counsel and a CPA |

| Changed beneficiary needs | Compare the request to the exact trust language before doing anything |

| Beneficiaries disagree | Pause until your authority is clear |

| Unclear or conflicting language | Seek legal interpretation before acting |

If you are wondering how to modify a trust in Texas, avoid informal fixes. A trustee should not rely on verbal family agreement, handwritten side notes, or "everyone understands what Mom wanted." Clear authority matters.

When a dispute is becoming dangerous

Some conflict is manageable. Some is a warning sign that you need legal help quickly.

Pay attention if you see any of these:

- A beneficiary accuses you of self-dealing

- Someone demands distributions that the trust does not clearly allow

- Family members pressure you to act fast without documentation

- You discover missing records or questionable past transactions

- A lawsuit, demand letter, or threat of removal appears

At that stage, your role is to slow the process down enough to protect the trust and yourself. Do not make a pressured decision just to keep peace at dinner. Short-term peace can create long-term liability.

Closing the trust the right way

Trust termination is the final test of whether the administration was handled carefully. Closing a trust is a little like closing out a business account after years of activity. You need to make sure nothing is left unresolved before the last assets go out.

A trust may end because its stated purpose has been fulfilled, its termination date arrived, or its remaining assets are ready for final distribution under the document. Before you send out the last checks or transfer the last title, make sure the trust is ready to close.

A careful termination usually includes:

- Confirming the legal basis for termination under the trust terms or applicable law

- Preparing a final accounting that a beneficiary can read and follow

- Paying remaining expenses, debts, and taxes

- Making final distributions exactly as the trust requires

- Obtaining receipts, consents, or releases when appropriate

- Saving the records in case questions arise later

That final accounting matters more than many new trustees expect. It is your closing map. It shows what came into the trust, what went out, why decisions were made, and what remains at zero. If a beneficiary later asks questions, your file should answer them.

Many trustees feel pressure to "just finish it." Resist that urge. A rushed termination can undo months of careful work. A methodical closing gives beneficiaries a clear picture, reduces later conflict, and helps you step out of the role with fewer loose ends.

Frequently Asked Questions About Texas Trust Administration

Can a trustee get paid in Texas

Often, yes. Texas law may allow reasonable compensation depending on the trust terms and the work involved. Some trust documents set compensation clearly. Others are silent, which can lead to questions about what is fair. A trustee should never pull money casually from the trust as “extra reimbursement” without authority and records supporting it.

What if I can’t find a beneficiary

Don’t guess, and don’t distribute that person’s share to someone else because it seems practical. Start with the trust file, prior correspondence, known relatives, financial records, and formal written outreach. If the beneficiary still can’t be located, the next step depends on the trust terms and the situation. This is one of those moments when legal advice can prevent an avoidable misstep.

How long does irrevocable trust administration texas usually take

There isn’t one standard timeline. A trust holding cash and a single investment account may move much faster than a trust holding real estate, business interests, disputed assets, or tax issues. Administration also slows down when titles need correction, beneficiaries disagree, or valuation work is required. What matters most is not speed by itself, but orderly administration supported by records.

Can a trustee make loans to beneficiaries

Only if the trust clearly permits it and the terms are followed carefully. Informal family loans create major risk because they blur the line between trust property and personal favors. If the trust allows loans, the trustee should document the authority, the amount, repayment terms, security if any, and the reason the loan fits the trustee’s duties.

How do the 2025 Medicaid changes affect trust administration

Recent Texas policy revisions effective April 2025 expanded the Medicaid look-back period for certain trust transfers and can impose penalties of up to 10 years for non-arm’s-length administration, according to this discussion of Texas trust planning and Medicaid changes. For trustees and families handling elder care planning, that means funding decisions and later administration need to be handled carefully. Transfers that look harmless inside a family may still create eligibility problems if they aren’t managed at arm’s length.

Do I need a Texas trust administration lawyer if the family gets along

Sometimes yes, even when everyone is cooperative. Friendly families can still face title defects, tax questions, community property issues, or uncertainty about the trustee’s authority. A Texas trust administration lawyer can help with legal interpretation, fiduciary duties in Texas, and protective documentation. That kind of guidance can also support related needs involving a Texas estate planning attorney, probate matters, or long-term asset protection planning.

Your Partner in Texas Trust Administration

A trustee’s journey usually follows a pattern. First, you gather documents and secure the assets. Then you inventory what the trust owns, create an accounting system, and manage property with care. After that, you make distributions only as the trust allows, handle tax reporting, and address disputes or final termination in an orderly way.

What makes this role hard isn’t only the paperwork. It’s the human pressure around it. Beneficiaries may need answers fast. Family members may remember the grantor’s wishes differently. Some assets raise technical issues involving valuation, marital property, taxes, or title. A trustee who slows down, documents decisions, and asks for help when needed is usually in a much stronger position than one who tries to solve everything alone.

Outside support can matter here. For example, teams looking to organize legal workflow and staffing sometimes explore resources such as Hire Paralegals to understand how administrative support can improve consistency in document-heavy matters. Even if a trustee never builds a formal team, the principle is useful. Trust administration works better when the process is organized and the right professionals are involved at the right time.

If your responsibilities touch related areas, it may also help to coordinate trust administration with broader legal planning, including estate planning, probate, guardianship, and asset protection. These issues often overlap, especially when the trust is part of a larger family plan.

A good trustee doesn’t need to know everything on day one. But the trustee does need to act carefully, keep good records, and get guidance before a small question becomes a larger legal problem.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.