Skip to content

Skip to content Managing a loved one’s charitable trust can feel overwhelming. You may have just learned that you’re the trustee, and now you’re asking practical questions: What do I sign first? Who do I notify? How do I protect the trust and honor the donor’s wishes?

That reaction is normal. Serving as trustee is both an honor and a legal job. In Texas, charitable trust administration requires care, organization, and a clear understanding of fiduciary duties. The good news is that the work becomes much more manageable when you approach it in order, one step at a time.

Your Guide to Navigating Charitable Trusts in Texas

A common situation starts like this. A parent, relative, or longtime family friend wanted part of their estate to support a church, school, scholarship fund, food pantry, or another mission that mattered a great deal to them. They named you as trustee because they trusted your judgment. Then the paperwork arrives, and the questions begin.

That’s where a practical playbook helps. Charitable trust administration texas isn’t only about handling money. It’s about carrying out a charitable purpose under Texas law, keeping accurate records, and making sure the trust serves the public benefit the donor intended.

Texas has an extensive charitable sector. The state has 92,734 nonprofit organizations statewide, which shows how significant charitable giving and charitable trust management are across Texas communities, according to Independent Sector’s Texas nonprofit profile. Texas law also gives qualifying charitable trusts unusual staying power. Under the Texas Trust Code, qualifying charitable trusts can continue indefinitely to carry out their charitable missions.

That long life creates both opportunity and responsibility. A charitable trust may support causes for years, or even generations, but only if the trustee administers it correctly.

For families holding real property in trust, it can also help to understand how title and ownership are handled in related trust settings. A useful outside primer on trusts for real estate syndication can make that side of trust structure easier to visualize, especially if the charitable trust owns or receives interests connected to real estate.

Practical rule: Your first job isn’t to make a big decision. Your first job is to slow down, read carefully, and avoid accidental mistakes.

Understanding Your Fiduciary Role as a Texas Trustee

A trustee is a fiduciary. That means Texas law holds you to a high standard of honesty, care, and loyalty. You’re not managing the assets as if they were your own. You’re managing them for the trust’s stated charitable purpose.

If you’re new to the role, it helps to think of fiduciary duties as guardrails. They guide every decision, from investments to distributions to beneficiary communication. If you want a deeper overview of fiduciary duties of trustees in Texas, that resource pairs well with the practical points below.

Duty of loyalty

The duty of loyalty means the trust’s charitable purpose comes first. Your convenience, personal preferences, and outside relationships can’t control your decisions.

Suppose a trust was created to fund scholarships at a local school. You can’t redirect money to a charity you personally prefer just because you like it better. You also can’t enter a transaction that benefits you personally unless the trust and law clearly allow it.

Conflicts of interest often confuse first-time trustees. Not every conflict is obvious. If your family member runs a business that wants to provide services to the trust, pause and get legal advice before moving forward.

Duty of prudence

The duty of prudence means you must act with care, skill, and caution. In plain English, don’t guess. Don’t gamble. Don’t ignore risk.

A prudent trustee reviews assets, understands liquidity needs, considers the trust’s time horizon, and documents why a decision makes sense. If the trust needs regular charitable payments, tying up all assets in something difficult to sell may create problems later.

A simple example helps. If the trust owns marketable investments and also owes regular distributions, a trustee usually needs a plan that balances growth with reliability. The goal isn’t chasing the highest return. The goal is supporting the charitable mission while protecting trust assets.

Duty to follow the trust terms

Your authority comes from the trust instrument. That document tells you what the donor wanted, who should benefit, what powers you have, and whether the trust has limits on timing, investment, or distributions.

If the trust says distributions must support educational programs, you can’t use trust assets for unrelated projects. If the trust names a specific organization, you need to confirm whether the trust requires distributions only to that organization or allows a broader charitable category.

Many trustee disputes begin with a trustee acting on memory or assumption instead of reading the document line by line.

The trust document is your operating manual. If a decision feels unclear, go back to the text before you act.

Duty of impartial and careful administration

Some charitable trusts involve current charitable beneficiaries and future remainder beneficiaries. Others may have layered interests that unfold over time. Even when the trust’s purpose seems straightforward, you still need to act fairly within the structure the donor created.

That can mean balancing present distributions with long-term sustainability. It can also mean communicating carefully with interested parties so no one is left guessing about what the trustee is doing.

A trustee who keeps organized records, explains decisions clearly, and sticks to the document usually avoids many preventable problems.

Here’s a short explainer that many new trustees find useful before they start making decisions:

Duty to keep records and stay compliant

Texas fiduciary principles work hand in hand with tax and reporting rules. You need records of assets, income, expenses, distributions, notices, and major decisions. Good records protect the trust. They also protect you.

Keep copies of correspondence, tax filings, appraisals, account statements, minutes of trustee decisions, and proof of distributions. If someone later asks why you acted a certain way, your file should answer the question.

A useful mental checklist looks like this:

- Read before acting: Confirm the trust language before making any distribution or investment change.

- Document your reasoning: Save notes showing why a decision fit the trust’s purpose.

- Separate trust property: Keep trust assets and records separate from personal assets.

- Ask early: If language is ambiguous, get legal or tax advice before the issue grows.

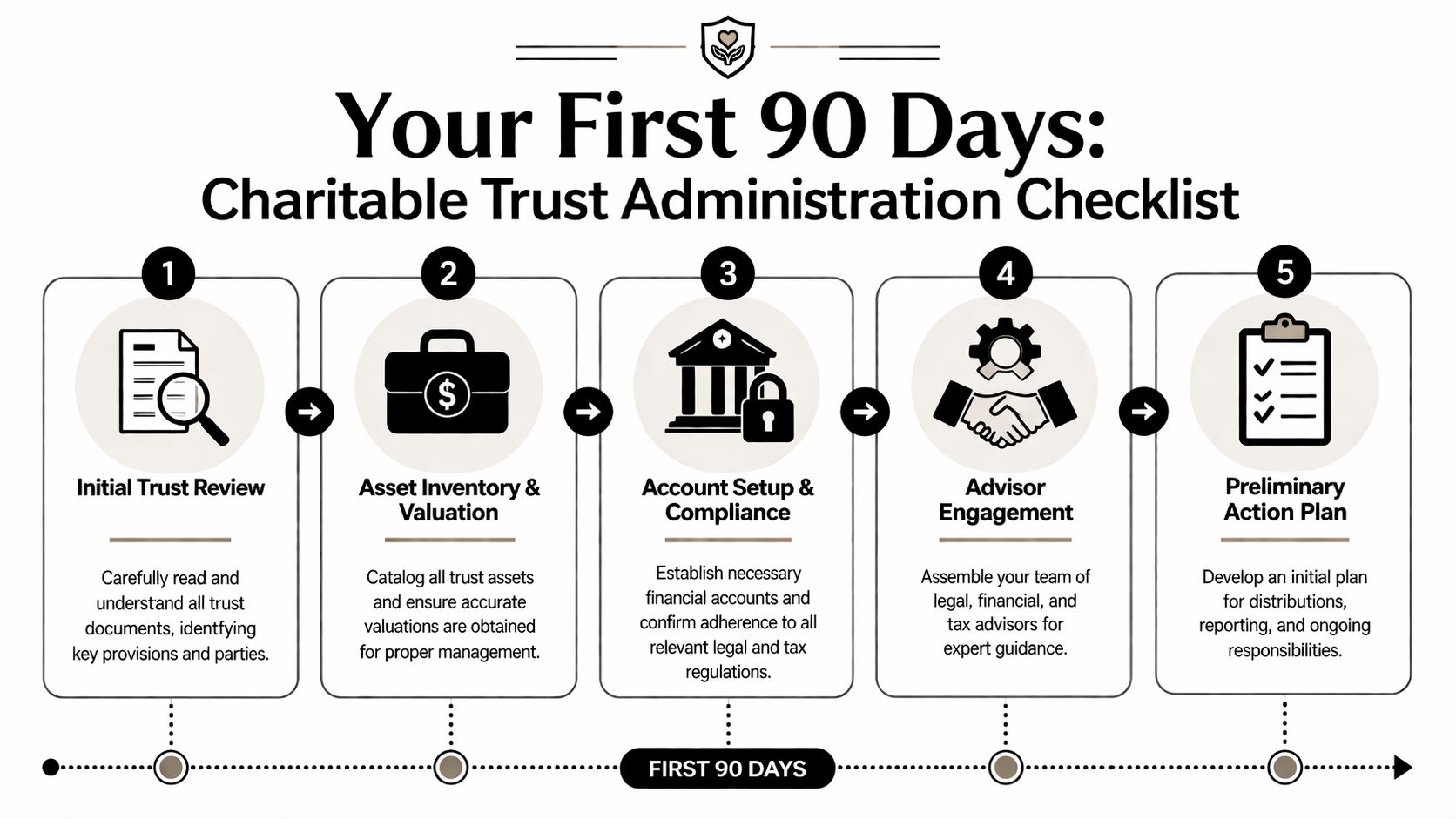

The First 90 Days Your Charitable Trust Administration Checklist

The opening phase of charitable trust administration texas sets the tone for everything that follows. Most trustee problems don’t start with bad intentions. They start with delay, missing paperwork, or assumptions about what the donor “probably meant.”

Treat the first few months like a controlled setup period. Your goal is to confirm authority, secure assets, identify deadlines, and create a working file that keeps you on track.

Put your acceptance in writing

A trustee should formally accept the role in writing. That sounds simple, but it matters. Written acceptance helps establish when your duties begin and shows that you’re acting in an official fiduciary capacity.

Once you accept, create a central administration file. This can be digital, paper, or both. What matters is consistency. Put the trust instrument, amendments, death certificate if relevant, tax identification information, account details, and all incoming correspondence in one place.

Read the trust like a working document

Don’t skim the trust. Read it with a pencil in hand. Mark provisions about purpose, beneficiaries, trustee powers, successor trustees, spending limits, and any special instructions.

Look for answers to questions like these:

- What charitable purpose controls the trust

- Who receives distributions

- Whether principal can be used or only income

- What notice or reporting duties apply

- Whether the trust was fully funded with the intended assets

Incomplete funding is a major source of trouble. A trust may exist on paper but still fail to control an asset if title was never transferred correctly. That’s why deeds, account retitling, and beneficiary designations need immediate review.

Inventory and secure every asset

Your next job is to identify what the trust owns. That often includes bank accounts, brokerage accounts, real estate, closely held business interests, or personal property.

Create an asset list with basic details such as account institution, title, approximate value, and whether the asset is already in the trust’s name. If something appears to belong to the trust but title is still outside it, don’t ignore that mismatch.

A simple working table can help:

| Asset type | What to confirm | Common issue |

|---|---|---|

| Bank account | Title and tax reporting | Account still in donor’s individual name |

| Brokerage account | Ownership and cost basis records | Missing transfer paperwork |

| Real estate | Deed record and legal description | Property never deeded into trust |

| Business interest | Governing documents and assignment | Transfer restrictions overlooked |

Checklist item: If you can’t prove an asset belongs to the trust, don’t assume it does. Verify title.

Notify the Texas Attorney General on time

This is one of the most overlooked parts of charitable trust administration in Texas. A charitable trust has a public-benefit purpose, so the Texas Attorney General has an oversight role.

A critical procedural requirement is notifying the Texas Attorney General’s Charitable Trusts Section by registered or certified mail within 30 days of filing and at least 25 days before any hearing, and failure in notice procedures is identified as one of the two primary failure points alongside incomplete asset funding, as explained in this guide to the Texas trust administration process.

The notice goes to the Texas Attorney General’s Charitable Trusts Section, P.O. Box 12548, Austin, TX 78711-2548. Keep proof of mailing and a copy of what was sent in your file.

New trustees often ask whether this notice step is just technical paperwork. It isn’t. Missing it can create delay, invite objections, and complicate court proceedings.

Build your advisor team early

A trustee doesn’t need to do everything alone. Depending on the trust assets, you may need a Texas trust administration lawyer, CPA, appraiser, investment advisor, or real estate professional.

The right team depends on the trust. A trust with a rental property needs different help than a trust holding marketable securities. A trust with narrow charitable restrictions may need more legal interpretation than one with broad discretion.

One available option for trustees who need legal guidance is the Law Office of Bryan Fagan, PLLC, which handles trust administration, fiduciary guidance, and related estate matters in Texas. Other trustees may already have family advisors or institutional support in place. The key is making sure the people advising you understand Texas trust law and charitable administration.

Open accounts and set an administration calendar

After inventory comes infrastructure. If the trust needs its own bank or investment account, open it correctly. Make sure statements are delivered to the right address and that accounting records can be tracked cleanly from the start.

Then build a simple calendar. Include tax deadlines, expected distribution dates, renewal dates for insurance, valuation dates for assets, and any hearing or notice dates.

A first-time trustee often feels better once everything is visible on one page. The role becomes less mysterious when deadlines are organized.

Send initial communications carefully

If the trust requires notices to beneficiaries or interested parties, send them promptly and keep copies. Use clear, neutral language. You’re not trying to argue a position. You’re confirming that administration has begun and that you’re acting under the trust terms.

This is also the right time to request missing records, gather prior account statements, and identify whether prior trustees, financial institutions, or family members hold key information.

A calm start prevents many future disputes. Trustees get into trouble when they disappear, delay responses, or leave others wondering whether anything is happening.

Ongoing Management Taxes Distributions and Reporting

After setup, the trustee’s work becomes cyclical. Review assets. Pay expenses. track income. Make distributions. File returns. Repeat. That rhythm is the heart of administration.

Many trustees expect a trust to run on autopilot once the accounts are open. It doesn’t. Ongoing administration requires regular attention, and charitable trusts often have less flexibility than people expect because the charitable purpose must remain central.

For readers exploring advanced planning ideas, this discussion of tax-efficient charitable giving in estate planning adds useful context on how charitable structures fit into a broader estate plan.

Recordkeeping that protects the mission

Strong administration starts with records that are current and readable. If someone reviewed your file a year from now, they should be able to tell what came in, what went out, why a decision was made, and how that decision supported the trust purpose.

Your files should usually include:

- Financial statements: Bank, brokerage, and investment account records.

- Distribution records: Copies of checks, wire confirmations, and letters to charities.

- Expense support: Invoices, receipts, tax payments, professional fees, and reimbursements.

- Decision notes: Short written explanations for major investment, sale, or distribution decisions.

This isn’t busywork. Good documentation helps a trustee answer questions before they become disputes.

Taxes and compliance in real life

Tax filing duties depend on the trust’s structure. In the verified guidance for charitable trust administration, trustees may need to handle annual Form 1041 filings in the ordinary administration process. For some charitable lead trust structures, trustees must also file IRS Form 5227 annually.

The practical lesson is simple. Don’t assume that “charitable” means “no tax paperwork.” A charitable trust can still carry significant filing duties, and timing matters.

A charitable lead trust offers a helpful example. In one model, the trust pays $60,000 annually to charity for 15 years, and trustees must manage those payments, investments, and annual Form 5227 compliance, as described in this overview of charitable lead trusts.

How distributions, investments, and taxes connect

A trustee managing a charitable lead trust can’t treat each task as separate. Investment choices affect the trust’s ability to make required payments. Those payments affect accounting. Accounting affects tax reporting.

Here’s how those pieces interact in practice:

| Administration task | What the trustee does | Why it matters |

|---|---|---|

| Investment review | Monitors assets and liquidity | Supports scheduled charitable payments |

| Distribution process | Sends required amounts to the charity on time | Fulfills the trust purpose |

| Tax reporting | Files required returns such as Form 5227 where applicable | Maintains compliance |

| Accounting | Reconciles income, expenses, and distributions | Creates a defensible record |

A trustee who misses one pillar often creates trouble in the others. If distributions are late, records become messy. If records are weak, tax filings become harder. If investments don’t support the trust’s payout needs, the trustee may have to sell assets under pressure.

“The best trustee calendars aren’t complicated. They’re consistent.”

Administering the charitable purpose, not just the assets

The trust’s charitable mission should guide distribution decisions. Before making a payment, confirm that the recipient and use fit the trust language.

If the trust benefits a named charity, verify the organization’s identity and current status. If the trust supports a category such as education or religion, document how the planned distribution aligns with that category. Keep the explanation short, but keep it in writing.

Many first-time trustees often make an innocent mistake. They focus on whether a cause feels worthy, rather than whether the trust authorizes that particular use.

Annual review habits that keep trustees out of trouble

An annual review doesn’t need to be dramatic. It needs to be disciplined.

Consider reviewing these items at least once during each administration cycle:

- Purpose alignment: Are distributions still tracking the donor’s stated mission?

- Asset mix: Does the current portfolio fit the trust’s payment obligations and risk profile?

- Tax file status: Are all needed returns, backup documents, and advisor requests organized?

- Communication log: Have required parties received notices, statements, or updates?

Trustees who build repeatable habits usually feel less stress over time. The trust becomes a managed system rather than a series of emergencies.

Navigating Trust Modifications and Common Pitfalls

Trust administration doesn’t always go according to the original plan. A named charity may close. A restriction may become impractical. A trustee may die, resign, or stop acting. Sometimes the trust still works, but the path forward needs court approval or Attorney General involvement.

The key is recognizing that charitable trusts are not purely private arrangements. Because they serve public purposes, changes often require more oversight than families expect.

If you’re dealing with changes to trust terms, this resource on how to amend a trust in Texas is a helpful starting point for understanding the broader legal framework.

When the trust purpose no longer works as written

A donor may have created a trust for a very specific charitable use that no longer exists in the same form. For example, a trust might direct support to a particular program that was discontinued years later.

In those situations, courts may apply cy pres, a doctrine that allows a charitable trust to be modified so the assets are used in a way that stays as close as possible to the donor’s charitable intent. The trustee doesn’t decide this alone and move on. Charitable trust modifications usually require a formal legal path.

A practical example makes this easier to understand:

- Original instruction: Fund a scholarship for a named school program.

- Problem: The program no longer exists.

- Possible response: Ask the court to approve a similar charitable use that closely matches the donor’s original purpose.

The Attorney General’s oversight role in real terms

Trustees often hear that the Texas Attorney General has authority over charitable trusts, but they don’t always know what that means day to day. It means the AG may need notice, may review certain proceedings, and may object if the proposed action appears inconsistent with the trust’s purpose or public interest.

That matters in trustee succession too. If a named trustee dies, refuses to serve, or fails to act, the process for installing a replacement may involve formal court filings and Attorney General participation.

When a trustee is facing modification, succession, or a disputed interpretation, one of the most important practical habits is early notice and complete documentation. A vague request usually creates delay. A well-supported petition is easier for the court and the AG’s office to evaluate.

Important reminder: If a charitable trust issue may require court involvement, don’t wait until a hearing is scheduled to gather your records.

A major trap is moving administration out of Texas

Some trustees assume they can move a charitable trust’s administration to another state for convenience, lower cost, or proximity to a new trustee. Texas law can make that much harder than people expect.

Texas Property Code Section 113.030 restricts moving administration of certain charitable trusts out of state without court approval, unless the trust terms allow it. A trustee who ignores that issue can face serious consequences, including challenges to their authority and requests for removal.

This problem often appears in multi-state families. A trustee moves to another state, changes advisors, and treats the trust as if it moved with them. For a charitable trust, that assumption can be dangerous. Before any relocation step, review the trust instrument and get legal advice on whether court approval is required.

Common pitfalls that start small and grow

Most trust crises begin as manageable issues. The danger comes from delay, silence, or informal shortcuts.

Here are recurring trouble spots trustees should watch for:

- Ambiguous trust language: A clause seems clear until a real decision has to be made. Get interpretation help early.

- Incomplete funding: The trust document exists, but the asset transfer never happened correctly.

- Loose communication: Family members, charities, or co-trustees receive mixed or inconsistent information.

- Undocumented decisions: The trustee remembers why they acted, but the file doesn’t show it.

- DIY modifications: A trustee tries to “fix” a charitable problem without the needed legal process.

A short comparison can help:

| Situation | Risky reaction | Safer approach |

|---|---|---|

| Named charity changes structure | Keep distributing without review | Confirm the trust still authorizes the payment |

| Trustee can’t continue serving | Informally hand records to someone else | Follow the trust and legal process for succession |

| Purpose becomes impractical | Redirect funds based on judgment alone | Seek legal guidance on court-approved modification |

| Trustee relocates | Assume administration moved too | Analyze whether Texas court approval is required |

Disputes don’t always look like lawsuits at first

Many disputes begin as questions. A beneficiary group asks for information. A charity wonders why distributions stopped. A family member claims the trustee is misreading the donor’s intent.

Responding well at that stage matters. Clear records, respectful communication, and prompt legal review often prevent escalation. Defensiveness usually makes things worse.

If your file shows that you read the trust, followed procedure, tracked the money, and sought help when needed, you’re in a much stronger position. That’s true whether the issue is a modification request, a succession problem, or a challenge to a past decision.

Partner with a Trusted Texas Trust Attorney

A charitable trustee’s job unfolds over time. First you accept the role and secure the assets. Then you read the trust closely, notify the right parties, and set up administration properly. After that comes the long-term work of investments, accounting, tax filings, distributions, and occasional problem-solving when the unexpected happens.

That’s a lot for one person to carry alone, especially if you’re also grieving a loss, balancing family expectations, or trying to protect a donor’s legacy without making a legal mistake. The role is manageable, but it usually works best with experienced support.

A Texas trust administration lawyer can help you interpret the trust, meet Attorney General notice requirements, address fiduciary duties in Texas, coordinate with tax professionals, and handle court filings if the trust needs modification or trustee succession. The same is true if you’re planning ahead. A Texas estate planning attorney can help families build charitable structures that are clear, workable, and easier for future trustees to administer.

Trust administration is not only about compliance. It’s about carrying a charitable vision forward with care.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including estate planning, probate, guardianship, asset protection, and charitable trust administration suited to your family’s needs.