Managing a loved one’s trust can feel overwhelming, especially when the trust owns mineral rights, royalty interests, or an old family lease that nobody has reviewed in years. Many new trustees open a drawer, find division orders, check stubs, and lease papers, and immediately worry they’re already behind.

That reaction is normal. Oil and gas interests in trust texas can be managed well, but they require closer attention than many other assets. A checking account is straightforward. A ranch house is visible. Mineral interests are different. They involve title questions, operator statements, lease terms, shifting production, tax treatment, and beneficiary expectations, all at the same time.

Texas families have been dealing with this kind of wealth for generations. After Spindletop, Texas oil production rose from 836,039 barrels in 1900 to 17,421,000 barrels by 1902, and the price collapsed to 3 cents per barrel, a sharp reminder that oil and gas assets can create wealth and risk at the same time, as described in the Texas Almanac history of oil discoveries. That same boom-and-bust pattern still matters to trustees today.

A trustee’s job isn’t to predict every market move. It’s to act carefully, stay organized, follow the Texas Trust Code and fiduciary principles, and make informed decisions that protect both current beneficiaries and future ones.

Introduction Managing Your Family's Texas Oil and Gas Legacy

Many trustees step into this role after a death, a disability, or a parent’s retirement from family business matters. Often, the trust document names someone reliable, but not necessarily someone with oilfield experience. If that’s you, the learning curve can feel steep.

The good news is that trust administration becomes manageable when you break it into parts. First, identify what the trust owns. Then confirm how the assets produce income. After that, focus on accounting, communication, and oversight. Those are legal duties, but they’re also practical habits.

Why these assets feel harder than other trust property

Oil and gas property is easy to misunderstand because the words sound familiar while the legal rights are very different. Owning a mineral interest is not the same as owning a royalty interest. Signing a division order is not the same as approving a lease. A monthly check may reflect production from months earlier and may include deductions that need review.

Trustees also face a tension that shows up quickly in real life. One beneficiary wants higher distributions now. Another wants the trust to preserve long-term value. Texas fiduciary law expects the trustee to balance both fairly.

Practical rule: If you don’t understand what generated a payment, don’t distribute it until you understand the source, the ownership basis, and how Texas law treats it for accounting purposes.

Why history still matters to a modern trustee

Texas oil wealth has deep roots, but the history matters for more than nostalgia. It teaches a core fiduciary lesson. Production can surge, prices can fall, and what looks like a windfall can turn into a management problem if the trustee treats it like a guaranteed stream of cash.

That’s why prudent trustees don’t just collect checks. They review leases, monitor operator conduct, keep records, and ask whether the trust is too concentrated in one asset class. Under fiduciary duties in Texas, loyalty is only part of the job. Prudence matters just as much.

Understanding the Types of Oil and Gas Interests

Before you can manage these assets, you need to know what the trust owns. Most confusion starts here. Families often use the phrase “oil rights” to describe several different interests, but each one carries different rights, risks, and duties.

A simple analogy helps. Think of an orchard. The landowner with mineral rights owns the orchard itself. The person with a royalty interest gets a share of the apples sold. The person with a working interest helps run the orchard and pays the operating costs.

Mineral interests

A mineral interest is the broad ownership right in the minerals below the surface. In Texas, that usually includes the right to lease the property for development, receive lease bonus payments, receive royalty under a lease, and sometimes receive delay rentals under older lease forms.

If a trust owns mineral interests, the trustee may need to decide whether to sign a new lease, approve an amendment, or review pooling language. That’s a real management role. It isn’t passive.

Royalty interests

A royalty interest is usually the right to receive a share of production revenue without paying drilling and operating costs. This is why many families prefer royalty ownership. It can generate income without exposing the trust to the same level of direct expense.

Still, “no drilling cost” doesn’t mean “no issues.” Royalty statements can include deductions, suspended funds, title-related holds, or confusing descriptions of volumes and pricing. Trustees need to read those statements closely.

A royalty check is not self-explanatory. It’s a report card, and sometimes it needs grading.

Working interests

A working interest carries more upside and more risk. The owner generally participates in the operation and bears costs connected to drilling, completion, and production. If a trust owns a working interest, the trustee has to pay much closer attention to cash calls, operating agreements, and possible liabilities.

For many new trustees, the need for legal and accounting help becomes immediate. A working interest can affect not only trust income but also the trust’s exposure to expense and operational problems.

Other terms you’ll see in the file

A few related terms show up often:

- Lease bonus means an upfront payment for signing an oil and gas lease.

- Delay rentals appear more often in older documents and relate to delaying drilling under certain lease terms.

- Division order is the operator’s ownership and payment instruction document.

- Pooling combines acreage for development and payment purposes.

Comparison of Oil and Gas Interests

| Interest Type | Right to Explore & Drill | Receives Lease Bonus | Pays Production Costs | Receives Royalty Payments |

|---|---|---|---|---|

| Mineral Interest | Usually yes, directly or by leasing | Usually yes | Not as a lessor under a standard lease | Usually yes under the lease |

| Royalty Interest | No | Usually no | No drilling or operating costs | Yes |

| Working Interest | Yes, through operational participation | No in the usual sense | Yes | Receives revenue subject to costs |

Where trustees usually get tripped up

The most common mistake is assuming every payment works the same way. It doesn’t. A lease bonus may be treated differently from royalty revenue. A royalty interest may require less active management than a working interest. A mineral interest may require a decision about whether to lease at all.

If you’re a trustee, your first question should always be this: What exact property right does the trust hold? Until you answer that, it’s hard to apply the Texas Trust Code correctly.

Your Fiduciary Duties as a Trustee in Texas

Trust law doesn’t expect perfection. It expects care, loyalty, and sound judgment. For oil and gas assets, that means more than depositing checks. It means active oversight.

Duty of loyalty and duty of impartiality

Under the Texas Trust Code, a trustee must act for the benefit of the beneficiaries, not for personal convenience or personal gain. That means no self-dealing, no side arrangements with family members, and no casual handling of trust assets because “everyone knows each other.”

Impartiality matters too. If one beneficiary relies on current income and another will inherit later, the trustee can’t favor the person who calls most often. Oil and gas assets make this harder because they are both income-producing and depleting. Every barrel or unit produced reduces what remains in the ground.

Prudence with a volatile asset

The prudent investor rule matters in every trust, but it becomes especially important with concentrated mineral wealth. A trustee should ask whether the trust is overexposed to one county, one operator, one producing formation, or one kind of interest.

That doesn’t always mean the trustee must sell. Sometimes the governing instrument encourages holding family mineral property. But even then, prudence requires monitoring, documentation, and reasoned decision-making. A trustee should be able to explain why a lease was signed, why a sale was rejected, or why an operator’s statement was challenged.

For a more detailed discussion of these standards, trustees often benefit from reviewing guidance on fiduciary duties of trustees in Texas.

Why oversight matters even when regulators are active

Some trustees assume state regulators will catch problems that affect trust income. That assumption can be costly. The Texas Railroad Commission approved 99.6% of flaring and venting applications, rejecting only 53 of more than 12,000 applications submitted from May 2021 through September 2024, according to the Texas Tribune’s reporting on flaring permit approvals. For trustees, the point is clear. Regulatory approval rates can leave operators with broad room to act, so the trustee can’t rely on outside enforcement to protect royalty income.

Trustees should assume they are the first line of review for trust-owned oil and gas revenue.

Day-to-day fiduciary behavior

A careful trustee usually does the following:

- Reviews incoming statements: Don’t just note the deposit amount. Match property descriptions, decimal interests, and deductions.

- Documents decisions: Keep a file memo when approving leases, amendments, or settlement positions.

- Uses qualified professionals: Landmen, CPAs, valuation experts, and Texas trust administration lawyers all serve a purpose.

- Communicates consistently: Beneficiaries handle uncertainty better when the trustee explains the process before conflict starts.

A short overview can also help if you prefer to hear these ideas explained aloud.

Principal, income, and fairness

Texas fiduciary accounting principles matter because beneficiaries may have different economic interests in the same asset. Current income beneficiaries care about distributions now. Remainder beneficiaries care about preserving the trust corpus for later.

That’s why a trustee can’t wing the accounting. Oil and gas proceeds often require careful allocation decisions under trust law and accounting rules. If those decisions aren’t handled consistently, a small misunderstanding can turn into a claim for breach of trust.

A Practical Guide to Administering the Assets

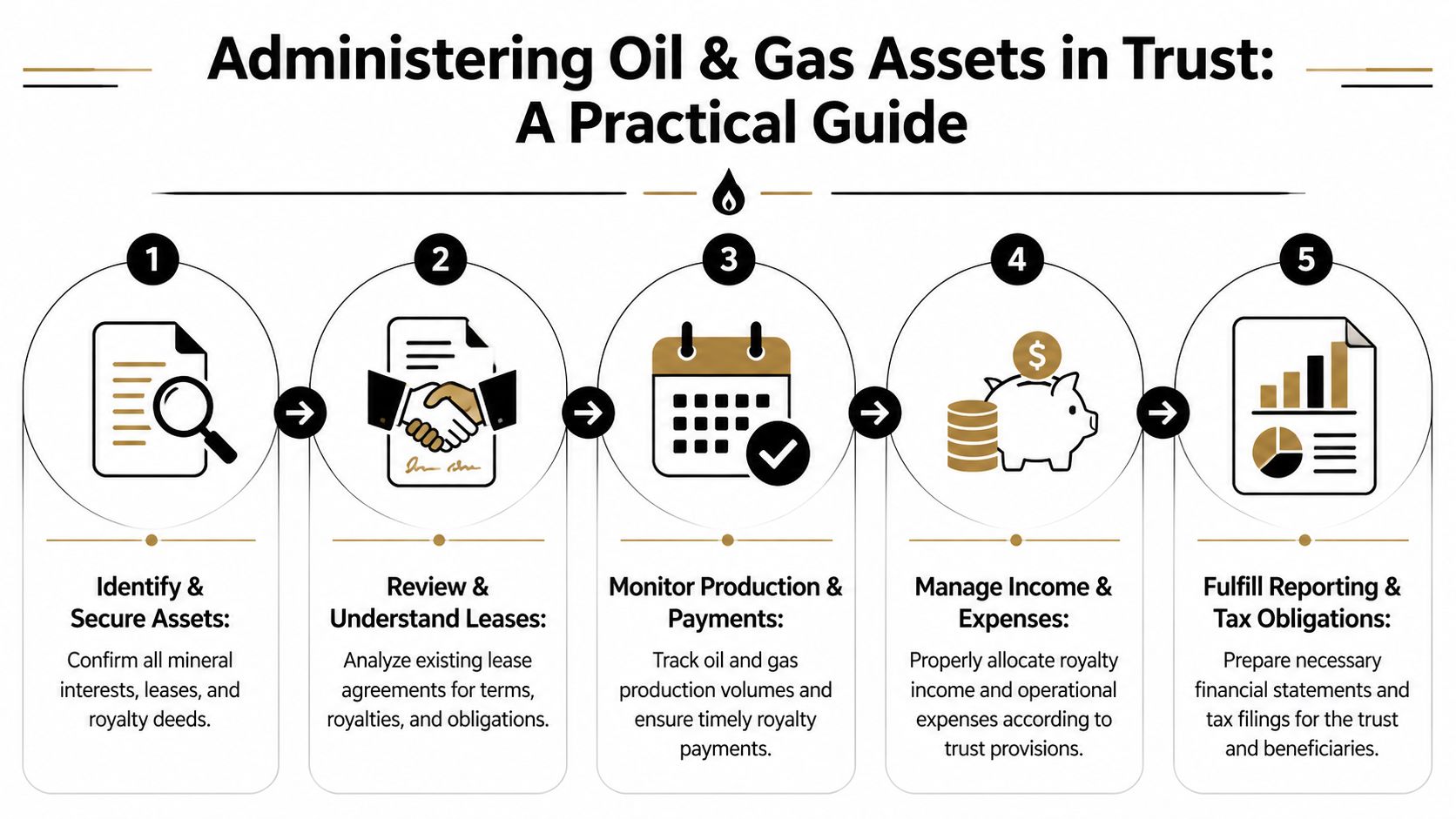

When a trustee first takes control, the work is easiest if handled in a deliberate sequence. You don’t need to solve everything in a week. You do need a clean process.

Your first round of action items

Start with the documents. Pull the trust instrument, any amendments, prior accountings, deeds, royalty deeds, leases, check stubs, tax returns, and operator correspondence. Families often have pieces of this in different places.

Then confirm the trust’s authority. Some trusts give broad power to lease, sell, pool, or settle claims. Others require consent from a trust protector, co-trustee, or beneficiary in certain situations. Read that language before responding to any operator request.

A workable ninety-day checklist

Identify every asset clearly

List each county, legal description, operator name, well name, and type of interest. Separate producing assets from non-producing ones.Verify title and ownership path

Make sure the trust holds what the family believes it holds. If title passed through an estate, confirm the probate documents and recorded instruments match the operator’s records.Notify operators and payors

Send the trust’s tax identification information, trustee certificates if appropriate, and ownership transfer documents. Until that happens, payments can be suspended.Review every division order carefully

A division order should match the trust’s ownership. If the decimal interest looks off, stop and investigate before signing.Audit royalty statements

Look for missing months, unexplained deductions, or sudden drops in revenue that don’t match what you expected.Create a trust accounting file

Keep payment detail, backup documents, tax forms, and correspondence together. If a beneficiary asks a question next year, you’ll need more than memory.

Reading royalty statements without getting lost

Royalty statements often overwhelm trustees because they compress several issues into one page. Focus on a few core fields first:

- Property identification: Does the well name and county match the trust records?

- Interest decimal: Is the ownership fraction the same as the division order?

- Volume and price entries: Do they seem consistent over time, or is there an unexplained drop?

- Deductions and adjustments: Are there transportation or post-production charges, and are they allowed under the governing lease?

If a statement doesn’t make sense, ask for backup. Trustees don’t have to accept unexplained numbers at face value.

Building a system beneficiaries can trust

Beneficiary tension often starts when the trustee has information but doesn’t share it. A simple communication routine can prevent that. Send periodic updates. Explain whether the trust owns royalty interests, working interests, or both. Note any title issues, suspended proceeds, or lease negotiations.

This is also the stage when many trustees decide they need structured legal guidance for trust administration. A practical resource on how to administer a trust in Texas can help trustees build procedures that are defensible, not improvised.

Navigating Tax and Accounting Rules for Mineral Interests

Oil and gas income can look simple on the bank statement and become complicated the moment tax season starts. Trustees need to know what came in, why it came in, and how it should be reported and allocated.

Income versus principal

One of the hardest issues is deciding what belongs to income beneficiaries and what should stay in principal. Texas law gives trustees a framework, but the trust instrument may change the default rules. That means the answer is not always found in a generic chart or a CPA’s software setting.

The depletion of mineral assets over time creates a critical balancing act for trustees. A trustee who distributes too aggressively may satisfy current beneficiaries while eroding the long-term value of the trust. A trustee who retains too much may frustrate income beneficiaries and invite conflict. The goal is consistency, supportable reasoning, and compliance with both the trust document and Texas fiduciary accounting standards.

For trustees who need more structure around reports, allocations, and beneficiary-facing records, a guide to fiduciary accounting in Texas is often a useful starting point.

Tax forms and why they matter

A trustee may receive a Form 1099 for royalty income or a Schedule K-1 if the trust owns an interest through an entity such as a partnership or LLC. Those forms don’t mean the same thing, and they can trigger different filing and recordkeeping questions.

Many families often encounter confusion. The operator’s payment detail, the trust’s accounting treatment, and the tax preparer’s reporting all need to line up. If they don’t, the trustee may end up explaining discrepancies to beneficiaries later.

Depletion and documentation

Trustees also hear the word depletion and assume it’s purely an accountant’s issue. It isn’t. Depletion reflects the wasting nature of the asset and can affect tax treatment and distribution analysis. The exact handling depends on the trust, the type of interest, and the trust’s tax posture, so individualized advice matters.

Good depletion work depends on reliable records. The Texas oil and gas industry’s projected $27.0 billion contribution in fiscal year 2025 in state and local taxes and state royalties provides a broad industry benchmark, and the Railroad Commission’s estimated 132 million pages of historical well records can help trustees verify title and production history, as noted by the Texas Oil and Gas Association’s 2025 energy and economic impact report. For trustees, the practical takeaway is that valuation and accounting should be document-driven, not guesswork.

Valuation in a state with uneven public pricing signals

Texas real estate and mineral valuation can be harder because public sale pricing isn’t always transparent. That’s one reason trustees sometimes use multiple data sources, including county records, operator information, reserve reports, and market comparables. For a useful overview of why valuation gets harder in states with limited price transparency, see PropLab for non-disclosure states.

Strong trust accounting starts with a paper trail. If the trustee can’t explain the number, the number probably isn’t ready for distribution.

Common Disputes and How to Proactively Avoid Them

Most trust disputes don’t begin with a lawsuit. They begin with a question. “Why is this month’s check lower?” “Why did you sign that lease?” “Why are deductions showing up now?” If the trustee can answer clearly and with records, the problem often stays manageable.

A familiar dispute between beneficiaries

Consider a common family scenario. One sibling receives income distributions and believes the trust should pay more because the wells are producing. Another sibling is a remainder beneficiary and worries the trustee is letting the operator drain value without enough oversight.

Neither person is necessarily wrong. They’re reacting to different interests. The trustee’s job is to step out of the family dynamic and return to the file. What does the lease allow? What do the statements show? How has the trustee allocated receipts? Was there a written explanation to beneficiaries?

The operator problem trustees often miss

Modern disputes increasingly involve flaring. Trustees may assume that if gas is being burned off, there’s nothing to be done because the operator has regulatory permission. That’s not always the end of the analysis.

A critical issue for trustees is lost revenue from methane flaring, where operators burn sellable gas. With Texas regulators approving more than 12,000 flaring permits and with concerns about lax enforcement, trustees may face diminished royalties and may need to quantify and potentially reclaim lost income from lessees, as discussed in ProPublica’s reporting on methane flaring and trust-related revenue concerns. For a trustee, that means asking hard questions when royalty income appears weaker than the production footprint would suggest.

Prevention usually looks boring, and that’s a good thing

The best dispute prevention steps are not dramatic:

- Send regular accountings: Beneficiaries should not learn major facts by accident.

- Keep signed copies and backup support: Lease files, division orders, and payment history matter.

- Ask for clarification early: Don’t let unexplained deductions become a year-long pattern.

- Use outside professionals when needed: An independent valuation or legal review can calm a tense situation.

A trustee who explains decisions in real time usually has fewer problems than a trustee who explains everything after trust has already broken down.

When legal help becomes necessary

Some disputes can’t be solved with better spreadsheets. If an operator won’t provide support, if a lessee may owe additional royalties, or if beneficiaries accuse the trustee of favoritism or self-dealing, formal legal advice is often the safest path.

That’s especially true when the issue involves possible breach of fiduciary duty, removal of a trustee, or litigation over trust accounting. Delay can make those problems more expensive and harder to unwind.

Drafting Your Trust to Protect Oil and Gas Wealth

A family trust can look perfectly adequate until the first lease amendment lands on the trustee’s desk. Then the true test begins. If the document says little about mineral management, the trustee may be left guessing whether they can approve pooling, sign a division order, hire a petroleum engineer, or sell a small tract that no longer makes economic sense.

That uncertainty creates practical problems, not just legal ones. A trustee who lacks clear authority may delay decisions, miss lease deadlines, or spend trust money asking a court for instructions that could have been built into the document from the start.

Powers the trust should address clearly

If the trust is expected to hold Texas mineral interests, royalty interests, overriding royalties, or working interests, the drafting should say so plainly. General investment language is often too broad to answer day-to-day oil and gas questions. A trustee may need express authority to lease minerals, amend leases, approve pooling or unitization, sign division orders, resolve payment disputes, consent to surface use terms, and hire landmen, accountants, engineers, or tax professionals.

Clear drafting also helps with modern operating issues. For example, a trustee may need authority to question deductions, investigate whether production is being wasted through flaring, or evaluate whether a nonproductive interest should be sold rather than carried year after year.

Match the trust language to the family’s actual goals

This part is often missed.

Some settlors want the trust to hold family minerals for generations, even if income rises and falls. Others care more about steady distributions and want the trustee free to sell a concentrated mineral position and reinvest. Some want both goals balanced, with room for judgment as market conditions, production levels, and family needs change.

The trust should not leave that choice to implication. If the settlor wants retention, say that. If the settlor wants diversification after a major well sale or a spike in royalty income, say that too. A few direct sentences can spare the trustee from trying to read family intent out of silence.

Drafting choices that help a future trustee do the job well

A stronger trust usually includes provisions like these:

- Specific mineral management powers: Authority for leasing, pooling, unit changes, surface agreements, division orders, settlements, and partial sales.

- Income and principal directions: Guidance on receipts from bonuses, delay rentals, royalties, and other payments if the settlor wants a result that differs from default treatment.

- Accounting instructions for wasting assets: Language that helps the trustee address depletion and explain why a large royalty check is not always the same as ordinary recurring income.

- Professional reliance provisions: Permission to rely in good faith on CPAs, reservoir engineers, appraisers, and land professionals.

- Removal and succession terms: Include a clean plan if the acting trustee cannot manage complex assets or no longer wants the role.

Good drafting works like a set of field instructions. The trustee still has to use judgment, but the trust tells them where they are allowed to act, when they should get help, and how to explain those decisions to beneficiaries. That makes administration easier, lowers the risk of conflict, and protects the oil and gas wealth the settlor meant to preserve.

Conclusion Your Partner in Texas Trust Administration

A new trustee often learns the job on an ordinary Tuesday. A royalty check is lower than last month, the statement shows unfamiliar deductions, a beneficiary wants an explanation, and the trust still needs accurate books. That is what Texas trust administration looks like with oil and gas assets. It is practical work, done carefully, one document and one decision at a time.

The trustee’s role is to keep the asset productive, account for it correctly, and explain it clearly. That can mean reading division orders against the deed, matching royalty statements to lease terms, tracking depletion in the trust accounts, and asking whether issues such as shut-ins, post-production costs, or methane flaring are affecting revenue. A mineral interest may sit dormant for years, then suddenly raise questions that need prompt attention and steady judgment.

Good administration usually looks less like courtroom drama and more like running a careful set of field records. The trustee gathers the lease file, revenue statements, tax forms, prior accountings, and trust language. Then the trustee works through each item in order, gets help from the right professionals when needed, and keeps beneficiaries informed in plain English.

That steady approach matters.

If you are responsible for a trust that holds royalties, minerals, overriding royalties, or working interests, early guidance can prevent accounting errors, missed lease issues, and family disputes. The goal is not just legal compliance. It is protecting the family asset while making decisions that you can explain with confidence years later.

If you are managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys advise Texas trustees on the day-to-day administration of oil and gas assets, from trust interpretation to payment review, accounting, and beneficiary communication.