Yes, but not as many assume, and often, they aren't the first or best tool for Texans. In Texas, a family home may already have unusually strong protection, including a homestead exemption for up to 10 urban acres or 200 rural acres for a family (100 rural acres for a single adult), regardless of the home's value, so the key question isn't just whether a trust works. It's whether a trust solves a problem Texas law hasn't already solved for you.

If you're asking this question, you may be in a familiar spot. You built a business, bought a home, saved for retirement, and now you're wondering what happens if life goes sideways. A lawsuit. A business dispute. A nursing home stay. A child who inherits money at the wrong time in life. Those worries are real, and they deserve a clear answer.

The Texas reality is more nuanced than many online articles make it sound. Asset protection trusts can be effective. But their value depends on what you're trying to protect, when you act, and how the trust is structured. A revocable living trust won't do the same job as an irrevocable trust. A Medicaid planning trust serves a different purpose than a trust designed to control an inheritance. And because Texas law already gives residents some strong built-in protections, trust planning often works best as part of a larger strategy rather than as a one-size-fits-all shield.

Protecting Your Legacy in Texas

A lot of families come to this issue after years of doing the right things. They paid off debt, invested carefully, kept insurance in place, and tried to build something stable. Then a parent's health starts to decline, or a business owner hears about a lawsuit involving someone in the same field, and suddenly “asset protection” stops sounding like a technical legal term. It feels personal.

Take a simple example. A Texas couple owns a home, has some savings, and wants to leave an inheritance to their children. One child is responsible but going through a difficult marriage. The other has a disability and receives public benefits. The couple has heard that “putting everything in a trust” protects it all. That idea sounds comforting, but it blurs together several very different legal tools.

Practical rule: The right trust depends on the risk you're trying to manage. Probate avoidance, creditor protection, Medicaid planning, and inheritance control are related topics, but they are not the same plan.

Texas trust and estate planning works best when it starts with the basics. What assets do you own? Who needs protection? What level of control are you willing to give up? Those questions matter under the Texas Trust Code, the Texas Estates Code, and basic fiduciary duties in Texas, because trusts don't protect assets by magic. They work because the law treats ownership, control, and trustee duties in specific ways.

Families also get tripped up by timing. If planning starts early, there are more lawful options. If planning starts after a creditor problem appears or after long-term care is immediately needed, many strategies narrow fast.

That's why a calm, Texas-specific analysis matters. A trust can be a very smart move. It just has to fit the actual legal and family problem in front of you.

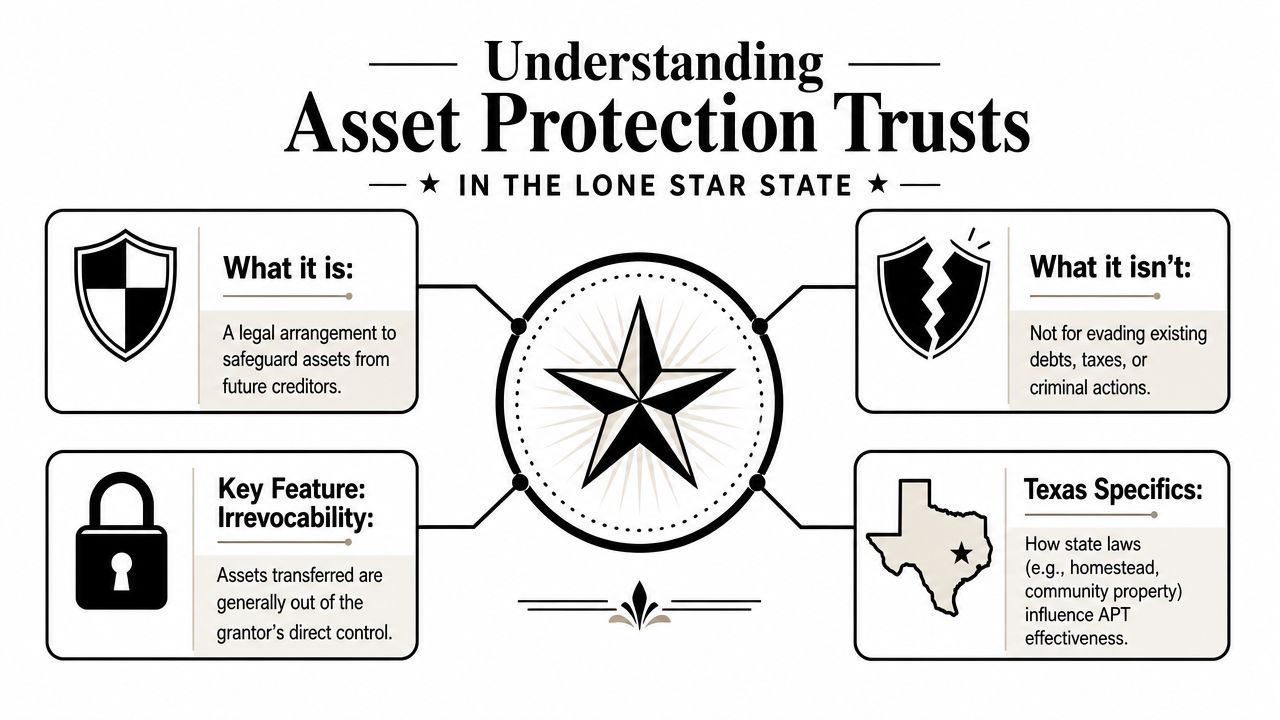

Understanding Asset Protection Trusts in the Lone Star State

An asset protection trust is a legal arrangement designed to place assets into a structure where they may be harder for future creditors to reach. The key word there is “future.” These trusts are not a tool for dodging known debts, taxes, or existing legal trouble.

The first major source of confusion is that many people hear “trust” and assume all trusts protect assets. They don't. Under everyday estate planning practice, different trusts do very different jobs.

Revocable trust versus irrevocable trust

A revocable living trust is like a personal safe in your own closet. It may help with management during incapacity and can help avoid probate, but you still control it. Because you still control it, it usually does not provide meaningful creditor shielding. Texas-focused guidance explains that a revocable trust is mainly for probate avoidance, while stronger protection generally requires an irrevocable structure, and Texas self-settled asset protection trust law remains an evolving policy issue rather than settled law, as discussed in this Texas asset protection primer.

An irrevocable trust is closer to a bank vault managed under written rules. You don't keep the same level of direct control. That loss of control is often the very reason the trust may offer stronger protection.

If you'd like a plain-English comparison of how trust mechanics work in another legal system, this overview of understanding trusts in Australia can be useful for basic concepts like grantor, trustee, and beneficiary. The legal rules are different, but the framework helps many readers understand why control matters so much.

Texas doesn't fit the usual DAPT model

Some states are known for Domestic Asset Protection Trusts, often called DAPTs. Texas is not usually at the top of that list. Texas does not have a straightforward, universally available domestic asset protection trust statute comparable to the states most associated with DAPTs. In 2023, lawmakers considered HB 4376, which proposed rules for a self-settled asset protection trust in certain Texas-connected situations, but that legislative history shows the framework is still developing rather than fully settled. You can review that background in the Texas HB 4376 bill analysis.

That matters because a Texas estate planning attorney often builds protection using tools such as irrevocable trusts, spendthrift provisions, and in some situations out-of-state structures, instead of assuming there is a simple Texas DAPT form waiting on a shelf.

Why funding and trustee duties matter

A trust document alone doesn't do much. Under core Texas Trust Code principles, the trust has to be properly created, and the assets have to be transferred into it. The trustee then owes fiduciary duties, which means the trustee must follow the trust terms, act loyally, keep proper records, and manage trust property for the beneficiaries according to the law and the trust instrument.

For families comparing options, this guide on an irrevocable trust in Texas is a useful next step because it focuses on the type of trust that most often drives real asset protection planning.

When Asset Protection Trusts Are the Right Tool

There are situations where a trust is not just helpful, but the most sensible tool on the table. Usually, those are situations where the family wants to do something Texas's default protections don't fully cover.

One common example is long-term care planning. Another is protecting an inheritance from a beneficiary's creditors, divorce risk, or poor financial judgment. A third is preserving assets for a loved one with special needs without disrupting eligibility for public benefits.

Medicaid planning and the timing problem

For Medicaid planning, timing is the heart of the strategy. A properly drafted and funded Medicaid asset protection trust is generally most effective when established well more than five years before anticipated long-term care needs, and the trust must be irrevocable to remove assets from countable ownership for eligibility purposes and to help avoid estate recovery. That timing rule and the importance of irrevocability are explained in this discussion of a Medicaid asset protection trust in Texas.

Many families are often surprised. They assume they can wait until a nursing home admission is imminent and then quickly “move assets.” Usually, that's exactly when options become limited.

Start before the crisis. Medicaid trust planning is strongest when the family still has time to make careful decisions.

Protecting the beneficiary, not the parent

Sometimes the trust is less about protecting the person creating it and more about protecting the person receiving from it. A parent may want a child's inheritance held in trust so that the child cannot withdraw everything at once. That can matter if the child faces lawsuits, debt problems, addiction, or a future divorce.

In those cases, lawyers often focus on spendthrift features and controlled distributions. The trustee's role becomes important here. Under fiduciary principles, the trustee doesn't get to act on impulse. The trustee has to follow the trust terms, consider the beneficiary's interests, and keep administration organized.

For readers exploring this kind of planning, protective trusts in Texas show how trust language can be used to guard an inheritance from outside pressure while still providing support.

Other good-fit situations

A trust may also be the right move when the family wants to:

- Preserve assets for a loved one with special needs so distributions can be managed carefully.

- Separate management from ownership when a beneficiary is young or financially inexperienced.

- Create a structured inheritance instead of delivering property outright at death.

- Coordinate trust administration with broader estate planning so the trustee, executor, and beneficiaries each know their role.

That's where a Texas trust administration lawyer or Texas estate planning attorney becomes useful. The drafting has to match the goal. If the family wants flexibility, one structure may fit. If they want stronger shielding, they may need to accept tighter limits on control.

The Hard Truth Limitations and Creditor Exceptions

Asset protection trusts can help. They are not an invisible cloak.

That's the part many websites skip, and it's the part families most need to hear. Courts look at intent, timing, control, and the type of claim involved. If those facts don't support protection, the trust may not do what the family hoped.

Fraudulent transfers are a major boundary

If someone transfers assets into a trust to block a known creditor or to escape an existing problem, that creates serious risk. Courts can scrutinize those transfers and may unwind them. In plain language, the law allows planning. It does not allow cheating.

This is why timing comes up so often. Good planning happens before the storm, not while it's already overhead.

A trust works best as a seatbelt, not as a getaway car.

Some claims stand on different footing

Even where trust planning is valid, not every kind of obligation is treated the same. Family support obligations and certain government claims are often viewed differently from ordinary creditor disputes. Readers should be especially cautious about assuming a trust can override court-ordered support obligations or tax-related enforcement.

The broader lesson is simple. Asset protection law is full of exceptions, and those exceptions are exactly where DIY planning falls apart.

Control cuts both ways

Many people want the benefits of an irrevocable trust while still keeping complete control over the assets. That usually isn't how protection works. The more ownership-like powers a grantor keeps, the weaker the protection argument often becomes.

Here are three common limitations families should expect:

- Loss of direct control: If the trust is meant to offer stronger protection, the grantor usually can't continue acting as though the assets are still personally theirs.

- Administrative demands: The trustee must keep records, follow fiduciary standards, and handle distributions correctly. Sloppy administration can create problems.

- Need for consistent funding: If an asset never gets retitled into the trust, the trust may not protect that asset at all.

These fiduciary issues matter under Texas law because trustees aren't figureheads. They carry real legal duties. The same is true for executors handling probate estates and for agents acting under powers of attorney. Good structure only works if the people in charge follow the rules.

Comparing Trusts to Other Texas Asset Protection Tools

For many Texans, the most important asset protection question isn't “Should I start with a trust?” It's “What protections do I already have?”

Texas gives residents some unusually strong built-in protections. That changes the conversation. Texas protects a homestead from forced sale for most debts, with an exemption of up to 10 urban acres for a family residence or 200 rural acres for a family, or 100 rural acres for a single adult, and the exemption applies regardless of home value. That existing legal shield is one reason a standard asset protection trust is often not the first line of defense for Texas residents, as explained in this discussion of Texas homestead and asset protection law.

Why Texas reality changes the usual advice

In some states, trust planning gets marketed as the central answer to nearly every creditor concern. In Texas, that can be misleading. If your main asset is your primary residence, state law may already provide substantial protection. If your concern is beneficiary control, then a trust may be more useful. If your concern is long-term care planning, a specialized irrevocable trust may be the better fit.

That's why good planning compares tools instead of chasing buzzwords.

Texas Asset Protection Tools at a Glance

| Tool | Level of Protection | Best For | Key Limitation |

|---|---|---|---|

| Homestead exemption | Strong statutory protection in many situations | Protecting a primary residence | Applies by law, but not to every kind of claim |

| Revocable living trust | Low creditor protection | Probate avoidance and incapacity planning | Doesn't usually shield assets from the grantor's creditors |

| Irrevocable trust | Can be strong if properly structured and funded | Medicaid planning, inheritance control, some asset protection goals | Requires loss of control and careful administration |

| Retirement accounts | Often protected by law in many contexts | Long-term savings | Rules depend on account type and circumstances |

| Life insurance and annuities | Often part of broader Texas protection planning | Family support and wealth transfer planning | Product terms and legal treatment vary by situation |

| LLC or business entity | Useful for separating business liabilities | Business owners and investors | Doesn't replace personal estate planning |

Choosing the right mix

Most families don't need only one tool. They need the right combination.

A practical strategy may include:

- Homestead planning: Understanding what your home protection already covers.

- Entity planning: Using LLCs or similar structures for business risk separation.

- Insurance review: Making sure liability coverage matches real-world exposure.

- Trust planning: Using irrevocable or protective trust structures for problems the other tools don't solve.

If you want to compare these options in more detail, this guide to Texas asset protection strategies helps place trust planning alongside other legal protections.

This is also where family roles matter. The trustee manages trust property. The executor handles a probate estate. Guardianship may become relevant if an adult loses capacity and planning was not done in advance. A broad estate plan ties those pieces together instead of treating them as isolated documents.

Best Practices for Implementing Your Asset Protection Strategy

A trust can look solid on paper and still fail in real life if the setup is sloppy. In Texas, that matters even more because families often already have meaningful protection for certain assets, especially the homestead. So the job is not just to create a trust. The job is to make sure the trust protects the assets that require extra planning, and to set it up in a way that holds up when stress hits the family.

Start before the problem starts

Timing shapes nearly every asset protection plan.

If a lawsuit, creditor claim, divorce fight, or long-term care crisis is already on the horizon, many planning options become weaker or unavailable. Courts look closely at transfers made after trouble appears. Medicaid planning also becomes much harder when the need for care is close.

Early planning gives a family room to think clearly. It also gives time to line up titles, beneficiary designations, tax reporting, and business records so the trust works with the rest of the estate plan instead of colliding with it.

Choose a trustee with care

The trustee is the person who turns trust language into real-world decisions. That includes following the trust terms, managing investments or distributions, keeping records, and treating beneficiaries fairly. A poor trustee choice can damage a good plan fast.

Some families do well with a relative who is organized and even-tempered. Others need a professional or corporate trustee because family history makes neutrality hard. A trustee works a lot like the driver of a heavy truck. The vehicle may be built well, but judgment behind the wheel still matters.

Consider questions like these:

- Judgment: Can this person follow the trust terms even if relatives push for exceptions?

- Recordkeeping: Can they track statements, notices, and decisions carefully?

- Neutrality: Will they deal fairly with more than one beneficiary?

- Staying power: Are they likely to be available years from now if the trust becomes active later?

Fund the trust correctly

A trust without transferred assets is an empty safe.

That means real estate may need a new deed. Accounts may need to be retitled. Business interests may need assignment documents. Beneficiary designations may need review so they support the trust plan rather than bypass it by accident.

For this reason, families often work with a lawyer, CPA, and financial advisor together. Each one sees a different part of the picture, and missed details are common when no one is coordinating the full plan.

Worth remembering: Signing the trust is only one step. Funding it and keeping records current are what make it function.

Review the plan as life changes

Good planning is not a one-time event. Families change. Assets change. Trustees move away, become ill, or die. A child who once needed tight restrictions may later be ready for more freedom, while another beneficiary may need stronger protection than expected.

Texas families also need to revisit the reason the trust was created in the first place. If state law already protects a key asset, the trust may need to focus on a different risk, such as inherited funds, business interests, or long-term care planning.

The Law Office of Bryan Fagan, PLLC handles trust administration, estate planning, probate, guardianship, and asset protection matters in Texas. That kind of coordinated legal support matters when a trust has to fit into a larger family plan rather than operate as a standalone document.

Is a Trust Right for Your Family Schedule a Consultation to Find Out

So, do asset protection trusts work in Texas? Yes, they can. But in Texas, the better question is whether a trust is the right tool for your specific goal.

If your concern is your home, state law may already give you meaningful protection. If your concern is Medicaid eligibility, timing and irrevocability can make all the difference. If your concern is protecting a child's inheritance, the trust terms and trustee choice may matter more than the label on the document. And if your concern is broader family planning, probate, incapacity, or fiduciary administration, the trust has to fit the full picture.

That's why this isn't a DIY project. Trust planning touches the Texas Trust Code, the Texas Estates Code, fiduciary duties, tax considerations, beneficiary rights, and in some cases probate or guardianship planning too. Families often need one plan that speaks to all of those moving parts.

A careful review can help you answer practical questions such as:

- What assets need protection most

- Whether a revocable or irrevocable structure makes sense

- Who should serve as trustee or executor

- How probate, guardianship, and trust administration fit together

- What steps to take now so your family isn't forced into crisis decisions later

The goal isn't to build the most complicated trust possible. It's to create a plan that works under Texas law and makes life easier for the people you care about.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including estate planning, probate, guardianship, trust administration, fiduciary duties in Texas, and asset protection strategies suited to your family's needs.