Managing a loved one's inheritance can feel overwhelming. You want to help, not control. You want to protect assets, not create family tension. That's why many Texas families ask about a spendthrift trust when they're worried a beneficiary may spend too fast, face creditor trouble, or need long-term structure rather than a lump-sum inheritance.

The short answer is that a spendthrift trust can be a very useful tool in Texas, but it isn't a simple “yes” or “no” decision. The key question is whether your family is comfortable with the trade-off between protection and independence. In many cases, the legal document works exactly as intended. The practical stress point is the relationship between the trustee and the beneficiary after the trust is funded.

Understanding a Texas Spendthrift Trust

If you're searching for guidance on Spendthrift trust Texas: pros and cons, you're probably in a familiar position. A parent or grandparent wants to leave money for someone they love, but worries that direct access to the inheritance could create problems. That concern is common, and Texas law gives families a way to plan for it.

A spendthrift trust is a trust that limits a beneficiary's ability to transfer, assign, or cash out their future interest before the trustee makes a distribution. In plain English, the beneficiary doesn't get to treat the trust like a personal checking account.

Who does what in the trust

Three people matter most:

- Grantor: The person who creates the trust and sets the rules.

- Trustee: The person or institution that manages the trust assets and makes distributions.

- Beneficiary: The person who receives the benefit of the trust under the terms the grantor wrote.

In practice, the grantor decides the overall structure. The trustee carries it out. The beneficiary receives support, but only in the way the trust allows.

Texas families often use this structure when they want support to come in stages. That may mean regular distributions, payments for certain life needs, or trustee-managed discretion instead of one large inheritance at once. If you want a broader overview of trust options, this guide to different types of trusts in Texas is a useful starting point.

Why Texas law gives these trusts real strength

Texas's modern spendthrift-trust rules are grounded in the Texas Trust Code, which authorizes spendthrift provisions and makes them a major asset-protection tool for families who want staged distributions instead of lump-sum inheritances, as explained in this discussion of Texas spendthrift trusts and their benefits.

That legal foundation matters because it gives the trust real force. A valid spendthrift clause blocks a beneficiary from assigning or selling their interest before distribution. Texas commentary also notes that creditors generally can't reach those trust assets while they remain in trust.

Practical rule: A spendthrift trust works best when the family wants a trustee to control timing and purpose, not when the beneficiary expects immediate access and full freedom.

Here's the basic picture:

| Question | Typical answer in a Texas spendthrift trust |

|---|---|

| Who controls distributions? | The trustee, under the trust terms |

| Can the beneficiary sell future trust rights? | Usually no |

| Can ordinary creditors reach assets still in trust? | Generally no |

| Does the beneficiary own the trust principal outright? | Usually no |

| Is this mainly about protection or flexibility? | Protection |

That legal protection is powerful. It's also only the beginning of the conversation.

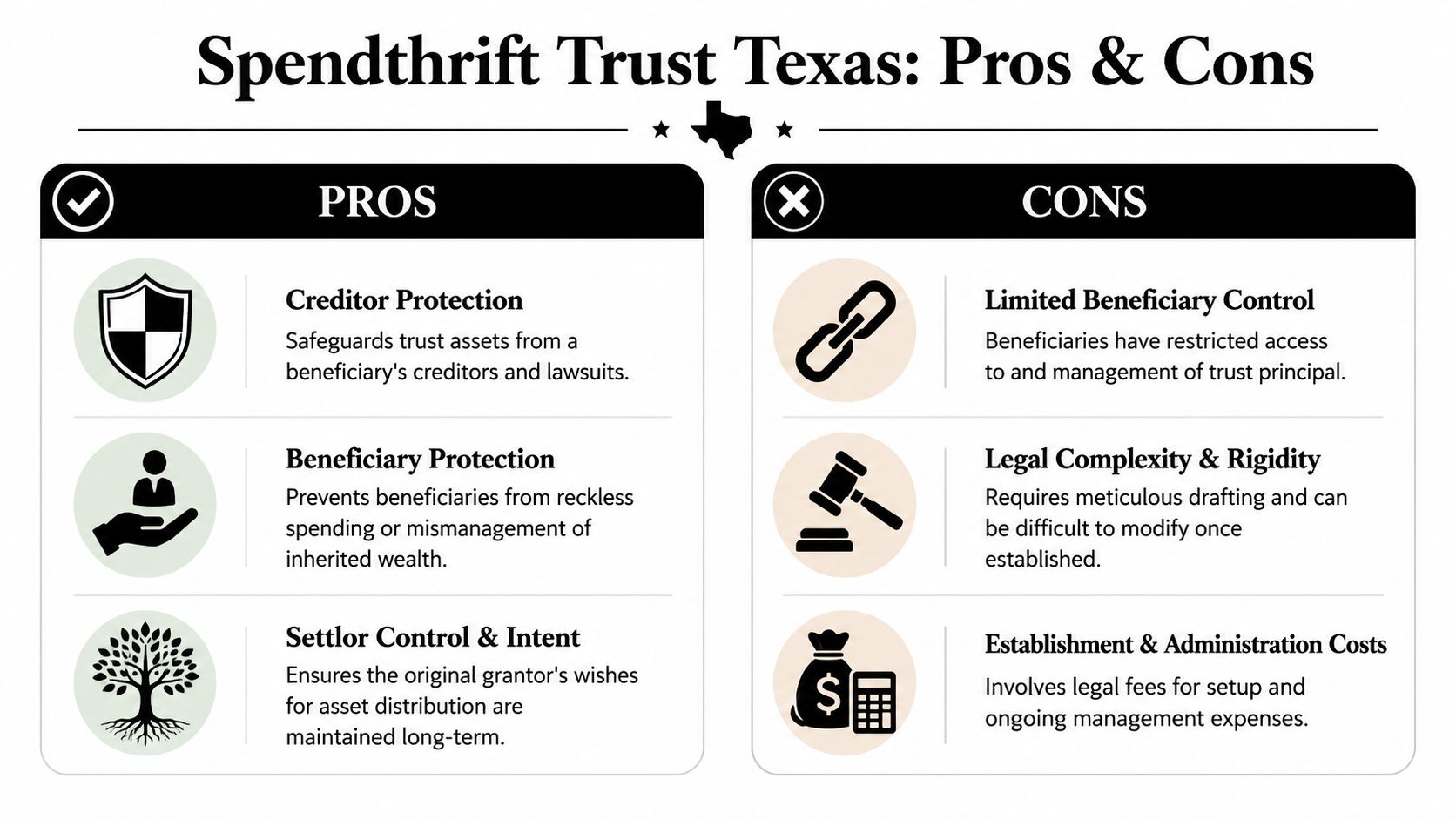

A Balanced Look at the Pros and Cons

A spendthrift trust is appealing because it solves a real problem. It can also create a different one. Families often focus on the asset protection and overlook the daily reality of living under the trust's rules.

This comparison helps frame the trade-offs early:

| Issue | Potential advantage | Potential downside |

|---|---|---|

| Access to assets | Limits rash decisions | Beneficiary may feel trapped |

| Creditor exposure | Helps protect assets held in trust | Protection has limits |

| Family legacy | Preserves the grantor's intent over time | Terms may feel rigid later |

| Trustee oversight | Adds structure and judgment | Can create delay or conflict |

| Administration | Professional management is possible | Ongoing legal and trustee costs |

Here's a quick visual summary before we go deeper.

Where a spendthrift trust works well

The strongest case for a spendthrift trust is when a family wants to protect a beneficiary from outside pressure and from their own weak financial habits. A parent may worry about debt, impulsive spending, unstable relationships, or a simple lack of experience handling money. In those situations, trustee oversight can preserve the inheritance and stretch support over many years.

The trust also helps the grantor keep control over the purpose of the gift. Instead of handing over everything at once, the grantor can require that distributions happen according to the trust terms. That can preserve the grantor's wishes long after death.

A well-designed spendthrift trust doesn't just hold money. It creates a process for support.

This is often why families choose it for younger heirs, financially inexperienced beneficiaries, or long-term preservation goals.

Where families feel the strain

The main downside is reduced flexibility and higher administration costs. The beneficiary usually has no direct access to principal, and the trustee must manage and distribute assets according to the trust terms rather than the beneficiary's preferences, as described in this overview of spendthrift trust disadvantages and administration issues.

That becomes real when life doesn't follow the script. A trust might work smoothly for years, then a beneficiary faces a sudden housing issue, medical need, business setback, or educational opportunity the document didn't clearly address. If the trust language is narrow, the trustee may say no even when the request seems reasonable.

The section below adds another layer of perspective.

What usually tips the decision

Families often choose a spendthrift trust when these facts are true:

- Protection matters more than autonomy: The beneficiary needs guardrails more than freedom.

- The trustee is well chosen: The person in charge is calm, organized, and capable of saying yes or no fairly.

- The trust terms are realistic: The document accounts for ordinary life needs and doesn't assume everything can be predicted.

On the other hand, the structure tends to disappoint people when:

- The beneficiary is financially responsible: In that case, tight restrictions may do more harm than good.

- The trustee is a poor fit: A rigid or conflict-prone trustee can turn a protective plan into a family dispute.

- The family wants flexibility: Some families need a structure that can adapt more easily over time.

The core issue in any Spendthrift trust Texas: pros and cons analysis is simple. You gain security, but you give up freedom.

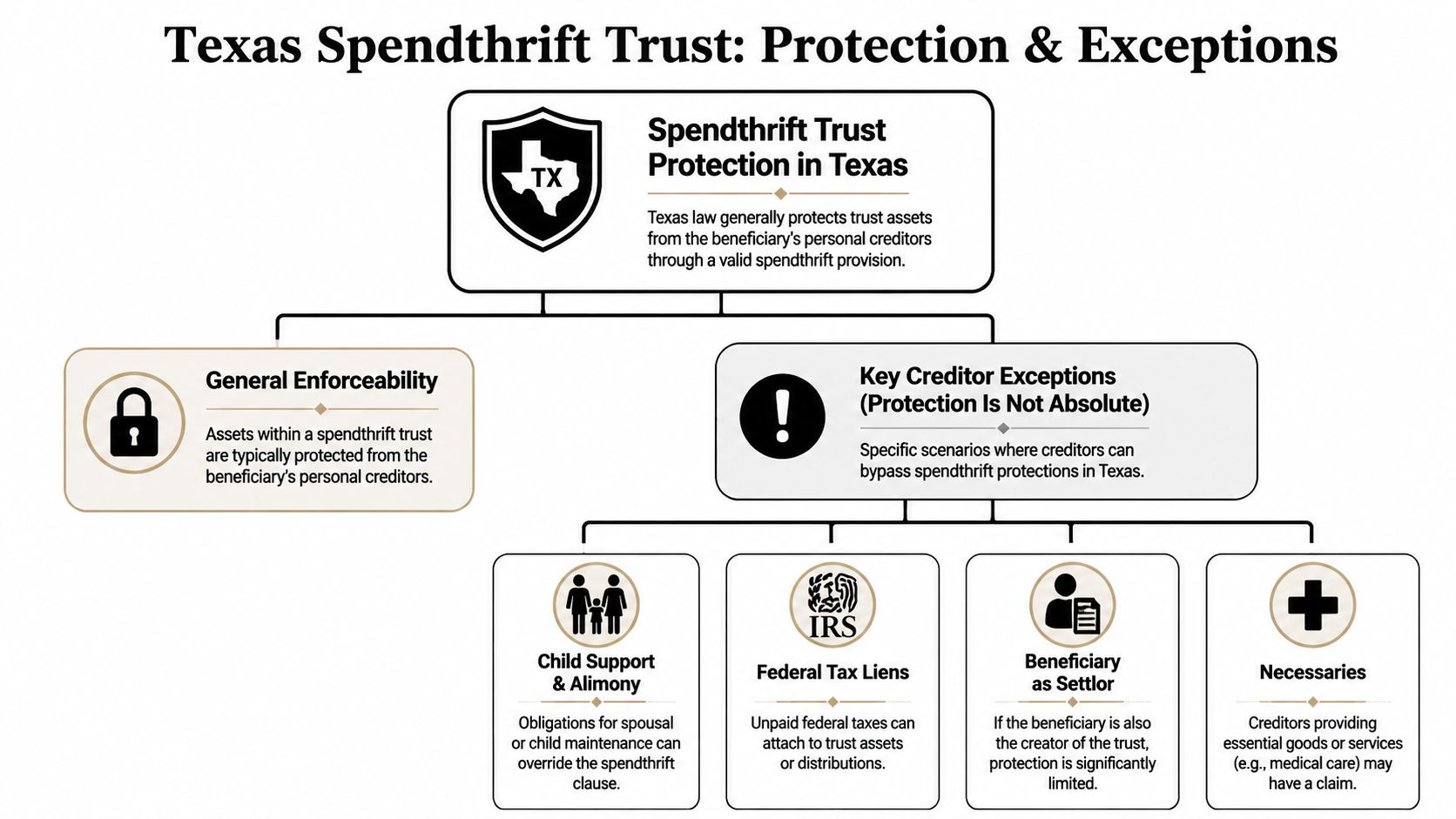

Enforceability and Creditor Exceptions in Texas

Many people hear “asset protection” and assume the trust creates a complete shield. It doesn't. A spendthrift trust can be strongly enforceable under Texas law, but it is not absolute protection against every claim in every situation.

That distinction matters because bad assumptions lead to bad planning. Families should understand both the rule and the exceptions.

What enforceability usually means

When the trust is properly drafted and administered, the spendthrift clause generally prevents the beneficiary from transferring future trust rights and keeps many ordinary creditors from reaching assets that are still inside the trust. That's the core protection most families are looking for.

It's one reason these trusts are often discussed alongside broader Texas asset protection trust strategies. They're not the same tool, but they often serve related goals.

Where the protection stops

Texas-specific commentary notes an important limit. Child-support claims can still be ordered against trust distributions, which means the protection is strong but not absolute.

That's the kind of exception families need to hear clearly. A spendthrift clause can do a lot, but it won't erase every legal obligation attached to the beneficiary.

Don't judge a spendthrift trust by its label alone. Judge it by the exact claims it can resist, and the claims it cannot.

Other vulnerability points are often less about the clause itself and more about execution. Poor drafting can invite disputes. Weak administration can give a creditor or opposing party room to argue. Sloppy funding can also undermine the structure if assets were never properly transferred into the trust.

A practical way to think about creditor protection

Use this lens when evaluating enforceability:

- Inside the trust: Protection is often strongest while assets remain under trustee control and undistributed.

- At distribution: Once money leaves the trust and reaches the beneficiary, the practical protection often narrows because the funds are no longer being held under the trust structure.

- When special claims apply: Certain legal obligations can still reach distributions despite the spendthrift language.

That's why drafting matters so much. A Texas estate planning attorney should spell out the distribution standard, trustee authority, and administrative procedures with care. The legal concept itself is well established. The quality of the document often determines how well that concept works in practice.

The Critical Role of the Trustee

Most articles about spendthrift trusts stop too early. They explain the clause, mention creditor protection, and move on. Families usually care about something more immediate. What happens if the trustee is too strict, too slow, or too personally involved to act fairly?

That concern is legitimate. A key question beneficiaries and families ask is what happens when the trustee is overly rigid, slow, or conflicted, and what remedies exist under Texas trust law. Many discussions never explain the practical escalation paths, even though trustee discretion can become a critical point of failure, as noted in this article on Texas estate protection and spendthrift trust concerns.

Trustee power is real, but it isn't unlimited

A trustee has authority, but that authority comes with fiduciary duties in Texas. In plain terms, the trustee must act in good faith, follow the trust document, manage trust property responsibly, and avoid using the position for personal advantage.

That's why choosing the trustee is often more important than choosing the trust type. A careful trustee can make an ordinary trust work well. A poor trustee can make even a strong document miserable to live under.

If you want a practical overview of the job itself, this guide on what a trustee does in Texas is a helpful companion.

What beneficiaries can do when problems start

Most trust conflicts don't begin with a lawsuit. They begin with silence, delay, or vague denials. A beneficiary asks for help with tuition, housing, or medical support. The trustee doesn't answer clearly. Weeks pass. Family frustration grows.

When that happens, beneficiaries should take structured steps:

Read the trust terms carefully

The first question is whether the requested distribution fits the written standard. If the trust allows distributions for health, education, maintenance, or support, the request should be framed in those terms.Make the request in writing

Verbal requests are easy to misunderstand. A written request creates a timeline and gives the trustee something specific to evaluate.Attach supporting records

If the beneficiary needs help with rent, tuition, treatment, or another major expense, documents matter. Estimates, invoices, admissions paperwork, and medical records often make the difference between a vague appeal and a proper request.Ask for a written explanation

If the trustee denies the request, the beneficiary should ask why. A written explanation often reveals whether the trustee is following the trust or solely acting from personal preference.

Beneficiary guidance: The more specific your request and the better your records, the harder it is for a trustee to dismiss you without explanation.

When informal resolution doesn't work

If the trustee remains unresponsive or appears conflicted, the next step is often legal review. Depending on the facts, families may need to request an accounting, seek instructions, ask the court to interpret the trust, or pursue removal of the trustee.

That doesn't mean every disagreement justifies litigation. Courts generally don't exist to second-guess every discretionary call. But courts can intervene when a trustee breaches duty, ignores the document, refuses to act, or turns discretion into personal control.

For concerned families, the practical lesson is simple. Don't just ask whether a spendthrift trust protects assets. Ask who will hold the power day to day, and what happens if that person mishandles it.

Drafting and Administering the Trust Effectively

A spendthrift trust often looks solid on paper and then starts to strain under ordinary family moments. A beneficiary asks for help with tuition, treatment, or housing. The trustee hesitates, asks for more information, or says no. The trust document usually determines whether that decision feels fair, arbitrary, or headed for a dispute.

Good drafting gives the trustee direction before those moments arrive. Good administration keeps the relationship from breaking down once money, stress, and family history enter the picture.

Drafting choices that prevent future problems

The strongest trust documents answer practical questions in advance. They tell the trustee what the grantor intended, how much discretion to use, what information the beneficiary should receive, and what happens if the trustee-beneficiary relationship stops working.

Useful drafting points often include:

- A clear distribution standard: Spell out whether distributions are limited to health, education, maintenance, support, or a family-specific standard that fits the beneficiary's situation.

- Examples of approved expenses: Tuition, rent, counseling, medical care, transportation, or business startup costs can be listed if the grantor wants the trustee to have clearer guidance.

- Communication requirements: Regular reports, annual summaries, or written responses to significant requests can prevent silence from turning into suspicion.

- Successor trustee planning: Name backup trustees and provide a realistic method for transition if the original trustee resigns, becomes ill, or proves to be a poor fit.

- Removal provisions: A carefully written removal clause can reduce deadlock and give the family a path forward without immediate court involvement.

The trust's design often determines whether families prevent conflict or plant the seeds for it. If the trust says only that distributions are “discretionary,” the trustee may have broad authority but very little guidance. If the trust is too rigid, the trustee may be unable to respond sensibly to real life.

Administration habits that build confidence

Administration is daily fiduciary work. It includes recordkeeping, investment oversight, tax reporting, timely responses, and consistent decision-making. In practice, beneficiaries are often less upset by a denial than by feeling ignored, confused, or judged.

A trustee should be able to show how a decision was made. That means keeping requests, invoices, notes, emails, and supporting records together in an orderly file. Families can reduce avoidable confusion by using practical systems for recordkeeping, including these tips for final document organization, especially if several people may need access to trust information during an emergency or after incapacity.

Consistency matters. So does tone.

A trustee who explains the process, asks for documents, and responds within a reasonable time usually preserves more trust than one who makes the same decision with no explanation.

A workable checklist for trustees

Trustees rarely get into trouble because one decision was hard. Problems usually grow from poor habits repeated over time.

- Read the trust before making a decision: Memory and family assumptions are not enough.

- Apply the same standard each time: Similar requests should be evaluated in a similar way unless the facts have changed.

- Create a record of major decisions: Note what was requested, what documents were reviewed, and why the request was approved, delayed, or denied.

- Respond promptly, even if the answer will take time: A short acknowledgment can prevent unnecessary resentment.

- Keep family dynamics out of fiduciary decisions: Old conflicts, personal disappointment, and parenting instincts are not the legal standard.

- Ask for legal guidance when needed: A Texas trust administration lawyer can advise on distributions, accountings, modifications, and dispute prevention.

The best-run spendthrift trusts are usually the ones with the clearest process, not the longest document.

That is the practical goal. A trust should protect assets without turning every request into a power struggle. If the document sets fair rules and the trustee follows them consistently, the trust is far more likely to do what the grantor intended and far less likely to leave the beneficiary feeling trapped.

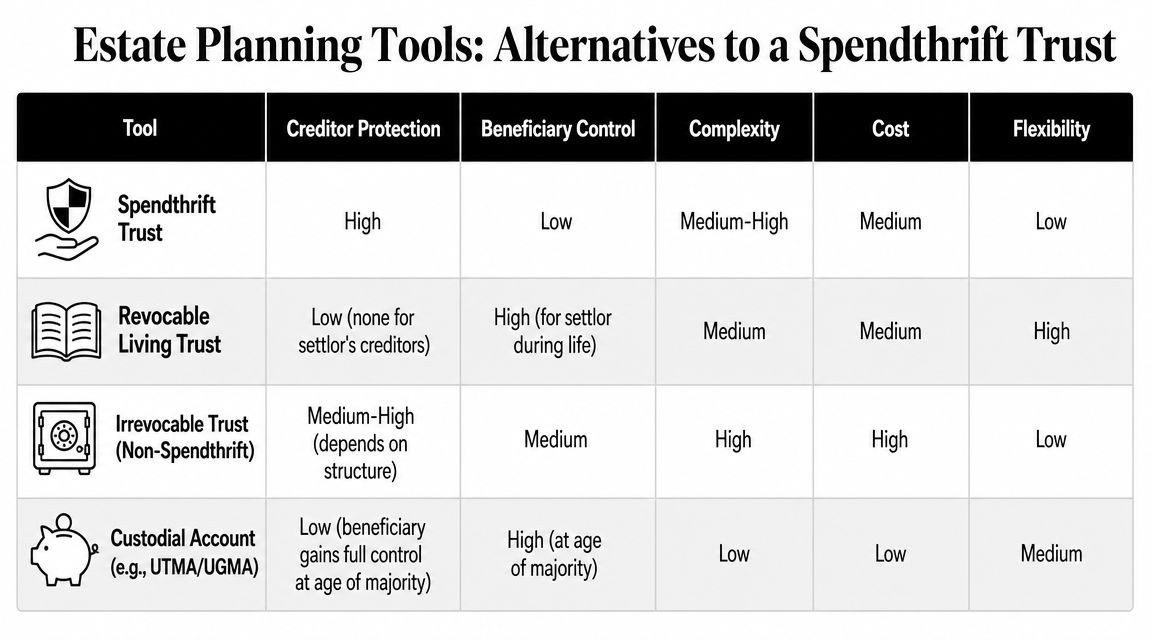

Exploring Alternatives to a Spendthrift Trust

A spendthrift trust is not the only way to protect a beneficiary. Sometimes it's the right tool. Sometimes it's too restrictive. A family should compare alternatives based on the beneficiary's maturity, the size and type of assets, the need for creditor protection, and how much control the grantor wants to keep through the trustee.

When a different trust may fit better

A discretionary trust can work well when the beneficiary's needs may change over time. It allows the trustee to evaluate circumstances and make judgment calls without being tied to a rigid schedule. For some families, that extra flexibility is an advantage. For others, it creates too much dependence on trustee personality.

An incentive trust may fit a family that wants to encourage certain milestones or habits. The trust can connect distributions to events such as graduation, employment, or other defined benchmarks. This approach can work, but it also requires careful drafting so the trust doesn't become punitive or unrealistic.

A revocable living trust serves a different purpose. It's often useful for probate avoidance, privacy, and management during incapacity, but it doesn't generally serve the same protective role for a beneficiary that a spendthrift trust does.

When simpler options may be enough

Not every beneficiary needs a heavy layer of control. In some families, an outright gift is appropriate because the beneficiary is financially responsible, well supported, and unlikely to misuse the inheritance.

For younger beneficiaries, a custodial arrangement may be simpler in the short term. But simplicity has a cost. Once the beneficiary gains control, the protective structure drops away.

This side-by-side view helps clarify the differences:

| Tool | Best fit | Main strength | Main weakness |

|---|---|---|---|

| Spendthrift trust | Beneficiary needs protection and structure | Controlled distributions | Less autonomy |

| Discretionary trust | Needs may be unpredictable | Flexibility for trustee | More room for dispute |

| Incentive trust | Family wants behavioral conditions | Goal-based planning | Can feel rigid or personal |

| Revocable living trust | Probate and incapacity planning | Flexibility during life | Limited protective value in this context |

| Outright gift | Beneficiary is ready for full control | Simplicity | No ongoing guardrails |

How families usually make the choice

Ask these questions:

- Is the beneficiary likely to benefit from restrictions or resent them?

- Does the family trust the proposed trustee to exercise judgment fairly?

- Is creditor protection a major concern, or is this mostly about convenience and probate planning?

- Will the trust terms still make sense years from now?

A good estate plan doesn't use the most complicated tool. It uses the right one.

If you're weighing Spendthrift trust Texas: pros and cons, the decision should turn on human realities as much as legal doctrine. The strongest document in the world can't fix a poor trustee choice, unclear expectations, or a trust structure that doesn't match the beneficiary's actual needs.

If you're managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including estate planning, probate, guardianship, asset protection, trust administration, fiduciary duties in Texas, and questions about how to modify a trust in Texas.