Skip to content

Skip to content Managing a loved one's trust can feel overwhelming, especially when one beneficiary needs money now and the trust still isn't ready for final closing. A trustee may feel pulled in two directions at once. One side says, “Help the beneficiary.” The other says, “Don't make a mistake that hurts the trust or the rest of the family.”

That tension is common. It doesn't mean anyone is doing something wrong.

A partial distribution is often the tool that helps. It gives a trustee a way to release some trust assets before the entire administration is finished, while still protecting the trust and honoring fiduciary duties in Texas. For anxious beneficiaries, it can also answer a basic question that comes up often: “Do I really have to wait until everything is over?”

This guide offers partial distributions from a trust in Texas explained in plain English. It's written for new trustees, concerned beneficiaries, and families trying to understand what Texas law expects, what practical steps matter, and when legal help from a Texas trust administration lawyer or Texas estate planning attorney makes sense.

Navigating Your Role in Trust Administration

You may be holding two very different concerns at the same time. A beneficiary needs money now. The trust still has unanswered questions.

If you are the trustee, you are expected to make a careful call without freezing up or rushing ahead. If you are a beneficiary, you may be looking at the same trust and wondering why a payment cannot happen sooner. Both reactions are normal.

The hard part is that a trustee is making a decision under uncertainty. A trust can look well funded on paper and still be short on cash once taxes, property costs, accounting fees, or unresolved claims are considered. A trustee also has to ask a practical question that many families miss at first: how much should stay in the trust as a reserve so the administration can finish safely?

That is why this process works best as a sequence of decisions rather than a single yes-or-no choice.

Why this feels more complicated in real life

Trusts rarely contain one simple asset. They often hold a mix of cash, brokerage accounts, real estate, business interests, mineral rights, or personal property. Cash can usually be distributed quickly. A house, closely held business interest, or disputed asset may take much longer to value, manage, or transfer.

A partial distribution works a bit like serving one course before the full meal is ready. The trustee may be able to release part of the value now, while keeping enough in reserve to cover what is still unknown.

That judgment call matters.

A trustee is not just sending money out. The trustee must follow the trust terms, protect trust property, pay proper expenses, consider taxes, and treat beneficiaries fairly. Those responsibilities are part of the trustee's fiduciary duties under Texas law. A beneficiary, by contrast, often sees an immediate need and a trust that appears to have available assets. That difference in viewpoint is where tension usually starts.

A sound partial distribution decision usually turns on five practical questions:

- What does the trust authorize or require?

- Which assets are liquid today?

- What expenses, taxes, or claims might still need to be paid?

- How much should remain in reserve?

- How will the trustee explain the decision clearly to all beneficiaries?

That last question is easy to underestimate. Clear communication often prevents the suspicion that one beneficiary is being favored or that the trustee is stalling. A short written explanation can calm a situation that might otherwise grow into a dispute.

Trust administration becomes much more manageable when you treat partial distributions as a framework for decision-making. First identify what can be paid. Then identify what must be held back. Then document why the amount is fair, prudent, and consistent with the trust. That is the practical "how" many families are looking for, and it is often the difference between a smooth administration and an avoidable conflict.

What Is a Partial Trust Distribution

A partial trust distribution is an advance payment from trust assets before the trust is fully wrapped up. Think of it as an interim payout. The trustee releases part of what a beneficiary may ultimately receive, while keeping enough in the trust to finish administration properly.

That last part matters. A partial distribution is not the same as the final distribution.

How it differs from a final distribution

A final distribution usually comes after the trustee has done the major administrative work. By that point, the trustee has typically addressed debts, taxes, expenses, and the accounting needed to show what came into the trust and what went out.

A partial distribution happens earlier. It gives a beneficiary access to some value now, but it doesn't end the trustee's job. The trustee still has to reconcile that advance later.

Texas practitioners note that partial or preliminary distributions are often used to provide beneficiaries immediate access to liquid assets like cash and marketable securities while administration continues, especially when the trust also holds less-liquid assets such as real estate. Any such advance must be reconciled in the trust's final accounting, as discussed in this overview of partial distributions.

Why trustees use them

A trustee may consider a partial distribution when there is cash on hand but other assets still need time. Common situations include:

- Immediate support needs: A beneficiary needs help with living expenses, housing, or other pressing costs.

- Uneven asset mix: The trust has cash and investments, but also real estate that can't be sold quickly without risk.

- Administrative delay for good reason: Taxes, valuations, or debt issues still need to be resolved before the trust can close.

Here's a simple example. A trust holds cash, a brokerage account, and a house. The trustee can distribute part of the cash now without forcing a sale of the house at the wrong time. Later, once the house is sold or transferred and final costs are known, the trustee can make the final distribution.

A partial distribution helps when the trust is ready to share some assets, but not ready to share all of them.

What a beneficiary should understand

A partial distribution doesn't automatically mean the beneficiary is entitled to demand money right away. It also doesn't mean the trustee can hold everything back forever. It's a middle path.

For beneficiaries, the key point is this. A partial distribution is usually a sign that the trustee is trying to balance immediate needs with the duty to protect the trust as a whole.

The Legal Framework for Texas Trust Distributions

A partial distribution usually feels straightforward until the first hard question appears. A beneficiary asks for funds now. The trust owns enough cash to pay something. But there are still taxes to file, bills to confirm, and other beneficiaries to treat fairly. At that point, a trustee needs more than a general idea of discretion. The trustee needs a decision framework grounded in Texas law.

Start with three sources of authority. The trust document sets the rules. Texas law fills in what the document does not spell out. Fiduciary duty controls how the trustee applies both of those in real life.

The trust document sets the starting rules

The trust instrument is the first place to look because it tells you what kind of distribution power the trustee possesses. Some trusts require distributions at specific times or under specific conditions. Others permit distributions only if the trustee decides a stated standard has been met, such as health, education, support, or maintenance.

That difference shapes nearly every later decision. If the trust says a beneficiary is entitled to receive income, the trustee's job is very different from a case where the trustee may distribute principal in the trustee's judgment. One is closer to following a written payment instruction. The other is closer to making a supervised judgment call.

Texas law also recognizes that trust terms can define and limit a trustee's authority in important ways. For a concise discussion of how Texas law distinguishes between rights a beneficiary is entitled to enforce and distributions that remain discretionary, see this discussion of Texas trust law development.

Texas law fills the practical gaps

Even a well-drafted trust will leave open questions. It may not say how much cash should stay in reserve before a partial distribution. It may not explain how quickly a trustee must respond to a request. It may use broad language that sounds simple until family circumstances make the choice harder.

Texas trust law provides the guardrails for those moments. It helps answer questions about administration, interpretation, and the trustee's duties to current and remainder beneficiaries. A useful way to view it is this. The trust gives the map, and Texas law supplies the road signs when the map is incomplete.

That matters most in the "how" and "when" decisions trustees often struggle with. Can you distribute now if the final tax bill is still unknown? Should you wait for an appraisal before dividing assets? Is it fair to make a cash payment to one beneficiary if another will receive illiquid property later? Those are not abstract legal questions. They are daily administration questions, and Texas law gives the trustee a structure for answering them carefully.

Some readers also like to compare how trust planning is discussed in other settings. For broader context, see financial advice for small business owners, but a Texas trustee should always return to Texas law and the language of the trust at hand.

Fiduciary duty is the control on discretion

Trustees often get tripped up by the word "discretion." In plain English, it sounds like freedom to choose. In trust administration, it means authority to choose within legal limits and for proper reasons.

A good analogy is a referee with a rulebook. The referee has judgment. The referee does not have permission to ignore the rules, favor one side, or make calls without a reason. A Texas trustee works under the same basic discipline.

So even if the trust gives broad discretion, the trustee still has duties of good faith, loyalty, prudence, and, when applicable, impartial treatment among beneficiaries. That affects both the decision and the process. The trustee should gather current financial information, consider foreseeable expenses, keep reasonable reserves, and be able to explain why the amount and timing of a partial distribution made sense.

Tax issues are part of that analysis, not an afterthought. A distribution can affect reporting, timing, and the net result to beneficiaries, which is why trustees should understand the basics before sending money out. This practical guide on how trust distributions are taxed in Texas is a helpful starting point.

The safest way to read the framework is simple. The trust grants the power. Texas law supplies the operating rules. Fiduciary duty requires the trustee to use that power with care, consistency, and a record that shows the decision was reasoned rather than reactive.

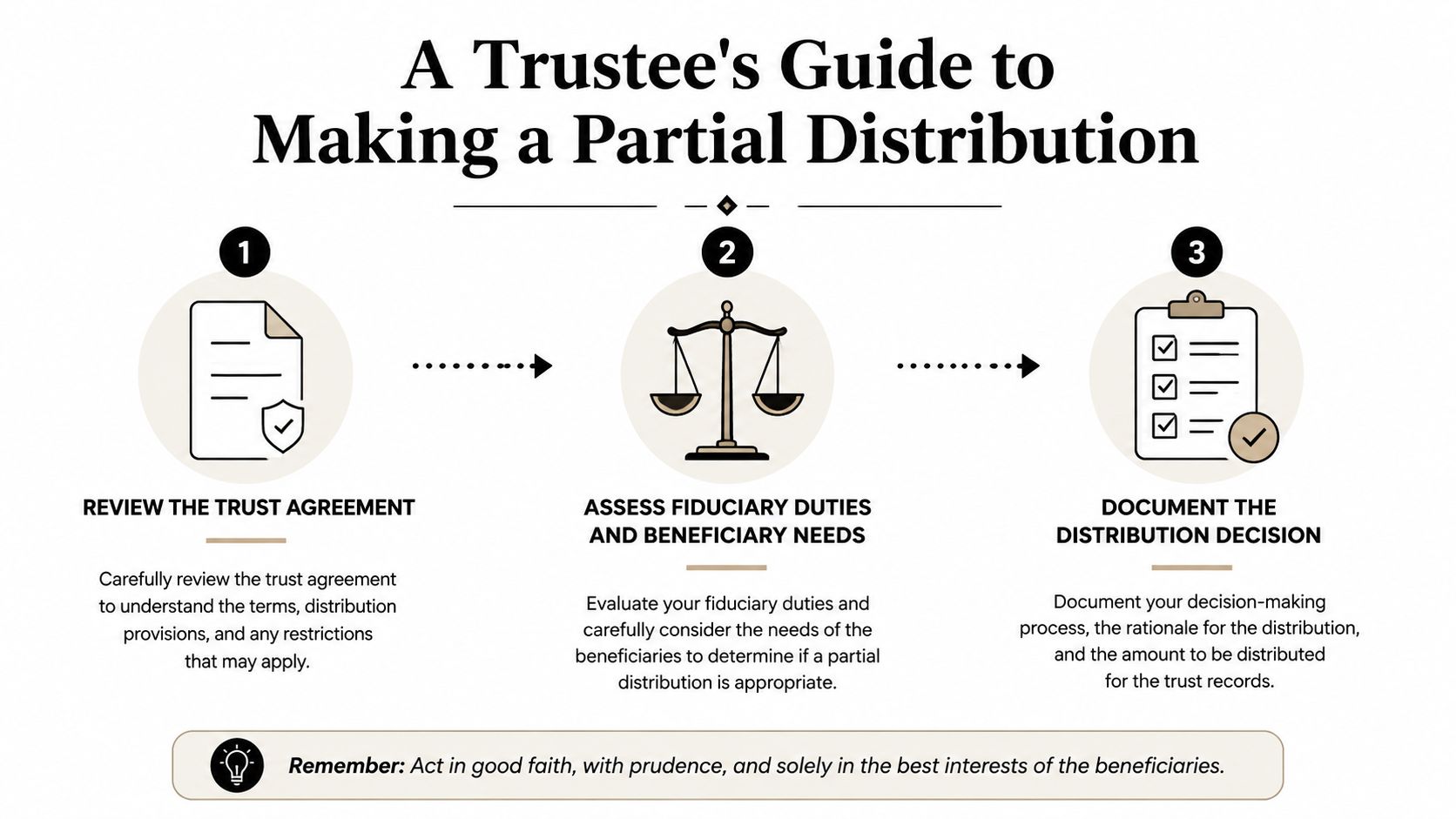

A Trustee's Guide to Making a Partial Distribution

A trustee should treat a partial distribution as a decision process, not a simple payout. Careful steps reduce risk, protect beneficiaries, and make it easier to explain why the trustee acted when they did.

Step one review the trust terms closely

Start with the trust instrument. Look for the distribution clause, any standards tied to support or maintenance, any mandatory income language, and any instructions about equalization among beneficiaries.

Don't stop at a quick skim. A trustee should also check for provisions about timing, reserves, tax payments, valuation, and powers over principal versus income. If the trust allows or requires different treatment for current and remainder beneficiaries, that has to be factored in early.

A trustee who wants a clearer picture of the role itself may also benefit from this overview of what a trustee does in Texas.

Step two evaluate the trust's financial position

Many trustees get into trouble by focusing on the beneficiary's request before doing the trust math.

Texas practitioners emphasize that even where a trustee has discretion, it must be exercised reasonably. Before making a partial distribution, the trustee should analyze the trust's liquidity, overall value, future appreciation potential, and the needs of all beneficiaries to avoid impairing the trust or forcing the sale of illiquid assets at a loss, as discussed in this Texas trustee guidance.

A useful working review often includes:

- Liquid assets: Cash, money market funds, and marketable securities that can be distributed without disrupting administration.

- Illiquid assets: Real estate, business interests, or concentrated holdings that may take time to value or sell.

- Known obligations: Taxes, professional fees, insurance, maintenance costs, and debts.

- Potential obligations: Unresolved tax items, claims, litigation risk, or expenses not yet billed.

Here's where trustee judgment matters. If a trust has plenty of cash, a partial distribution may be straightforward. If most value sits in real estate or a business interest, the trustee needs more caution.

Step three decide on a reserve

A reserve is the amount left inside the trust to cover expenses, taxes, and uncertainty. The exact amount depends on the trust's circumstances, not a one-size-fits-all formula.

The point is simple. If the trustee distributes too much too early, the trust may later need cash it no longer has. That can force an avoidable asset sale or create conflict when the trustee has to ask beneficiaries to return money.

Key judgment call: The trustee should keep enough in reserve so the trust can finish its work without scrambling for liquidity.

Step four compare the request against all beneficiaries' interests

A trustee can't look only at the person asking for money. The trustee has to consider everyone the trust is meant to benefit.

That doesn't always require identical treatment. Some trusts intentionally allow different treatment based on need or standards in the document. But the trustee should be able to explain why this distribution fits the trust's terms and doesn't unfairly prejudice another beneficiary.

This short video gives a useful overview of trustee decision-making in practice.

Step five document the file before sending funds

Before money moves, the trustee should build a record. That usually includes the request, the trust language relied on, the asset review, the reserve analysis, and the reason the trustee concluded the distribution is prudent.

This is one area where legal support can be practical rather than dramatic. A Texas trust administration lawyer, a CPA, and, when needed, the Law Office of Bryan Fagan, PLLC are examples of professionals a trustee may consult to review authority, documentation, and fiduciary risk before funds are distributed.

Step six pay the distribution and track it for final accounting

Once approved, the payment should be clearly identified as a partial or preliminary distribution. The trustee should record the date, amount, asset type, and beneficiary receiving it. Later, that payment must be reflected in the final accounting so everyone can see how earlier distributions affected the balance remaining.

A trustee who follows these steps usually makes better decisions, even when the answer is “not yet.” Beneficiaries may not like every outcome, but they are less likely to view the process as arbitrary when the reasoning is organized and transparent.

Documentation and Communication Checklist

Good trust administration depends on records. A trustee who makes a careful decision but leaves a thin paper trail may still face accusations of favoritism, delay, or poor judgment later.

Texas trustees can be held liable for delaying distributions without a justifiable reason, such as outstanding debts, tax issues, or the need to liquidate assets. The practical protection is to document the reason for making or delaying a distribution and to maintain a sufficient reserve to manage trust affairs, as explained in this Texas discussion of withholding distributions.

Documentation items to gather

Keep the file clear and chronological. A strong file often includes:

- Written beneficiary request: If the beneficiary asked for a distribution, keep the request in writing.

- Trust language excerpt: Save the exact provisions that authorize or limit the payment.

- Asset and liability summary: Show what the trust owns, what is liquid, and what obligations remain.

- Reserve analysis: Note why the trustee kept a certain amount in trust.

- Approval memo or trustee resolution: State the decision and the reasons for it.

- Proof of payment: Maintain copies of checks, wire records, or transfer confirmations.

- Receipt from beneficiary: Confirm that the payment was received and identified as a partial distribution.

Communication steps that reduce conflict

Communication isn't just courtesy. It's part of risk control.

- Explain timing clearly: Tell beneficiaries why some assets can be distributed now and others can't.

- Use neutral language: Avoid making one beneficiary sound more deserving unless the trust expressly requires that analysis.

- Address reserves directly: Beneficiaries often calm down when they understand money is being held for taxes, expenses, or unresolved issues.

- Follow up in writing: A short written summary after a phone call can prevent later misunderstandings.

| Phase | Action Item | Purpose |

|---|---|---|

| Before decision | Gather trust terms, asset list, and outstanding obligations | Confirm authority and financial capacity |

| Before payment | Create written reasoning and reserve analysis | Show fiduciary care and reduce liability |

| At payment | Label the transfer as a partial distribution | Avoid confusion about final entitlement |

| After payment | Notify relevant beneficiaries and update records | Promote transparency and accurate accounting |

| At final accounting | Reconcile the advance against remaining trust assets | Ensure fair final distribution |

Clear communication won't eliminate every disagreement, but silence almost always makes conflict worse.

This kind of checklist is also useful in related probate, guardianship, and asset protection matters, where records often become the difference between a manageable disagreement and a formal dispute.

Potential Pitfalls and How to Avoid Them

A partial distribution can feel simple at the moment a trustee signs the check. Then the actual questions show up. Did the trust keep enough back for taxes and expenses? Was this beneficiary entitled to receive money now, or did the trustee just create a fairness dispute that could have been avoided?

The safest approach is to treat a partial distribution like a measured release valve, not a finish line. Money can go out before the trust closes, but only after the trustee works through a few practical questions in the right order.

Paying too much too early

This is the mistake trustees make most often. Cash is sitting in the account, a beneficiary is asking for it, and the trust appears to have plenty. Appearances can be misleading.

Before sending funds, ask a simple question: what still has to be paid before this trust is ready for final distribution? That may include accountant fees, legal fees, property taxes, insurance, repairs, appraisal costs, fiduciary income tax filings, or a claim that has not been resolved yet. A house that has not sold can keep generating bills. A brokerage account can create tax reporting issues after the calendar year closes.

Reserves work like a buffer in the trust account. If the trust still has moving parts, the reserve should match those risks.

Treating beneficiaries without a clear standard

Trouble often starts when a trustee decides based on pressure instead of the trust terms. One beneficiary may have an urgent need. Another may insist that equal means immediate. A third may stay silent, then object later.

The trustee's job is not to satisfy the loudest person in the room. The job is to apply the trust's actual distribution standard. Some trusts call for equal shares. Others permit distributions for health, education, maintenance, support, or another stated purpose. If the trust gives discretion, that discretion still has to be exercised for a reason that can be explained and documented.

A useful test is this: could you explain the decision to all beneficiaries, side by side, using the same rule each time? If not, pause and reconsider.

Overlooking federal tax consequences

Taxes are one of the easiest areas to underestimate because the transfer itself can look straightforward. The accounting behind it often is not.

A partial distribution may shift taxable income from the trust to the beneficiary, depending on the trust's structure, the type of income involved, and the timing of the payment. In practical terms, a trustee should not ask only, "Can I distribute this?" The better question is, "What part of this payment may carry out income, and who will report it?"

That distinction matters because some payments are partly income and partly principal. A beneficiary may receive cash without realizing that only part of it affects the beneficiary's income tax reporting. The trust may also retain taxable income if the distribution does not carry all of that year's distributable net income. Texas does not impose a state income tax, but federal reporting still matters, and reserve planning should reflect that.

For broader background on preserving family assets while coordinating legal and financial decisions, some readers also review legal advice on asset management.

Ignoring character-of-property issues

Some assets carry extra baggage. A distribution of cash is one thing. A distribution of business interests, mineral interests, rental property, or appreciated securities can raise a different set of questions.

This comes up often when a beneficiary is divorcing, has creditor problems, or plans to retitle the asset quickly after receiving it. The trustee may not control those later events, but the trustee should keep clean records showing what was distributed, when it was distributed, and whether it represented income, principal, or a specific asset called for by the trust. Good records help everyone trace what happened if the asset's character becomes disputed later.

Delaying without a documented reason

Overcaution can create its own problem. A trustee who delays every distribution "just to be safe" can drift from prudence into inaction.

Texas trustees generally need a real administration reason for delay. Pending taxes, unresolved expenses, valuation problems, a sale that has not closed, or unclear trust language may justify waiting. General anxiety usually does not. Beneficiaries often sense the difference. If you want a practical explanation of where that line is, see whether a trustee can delay distributions indefinitely in Texas.

A sound decision-making framework is simple. Confirm authority under the trust. List the trust's remaining obligations. Set a reserve that fits those obligations. Review tax effects before money leaves the account. Then decide whether the timing is fair, defensible, and easy to explain in writing.

That is how trustees avoid the common traps. Not by guessing less, but by deciding more carefully.

When to Consult a Texas Trust Attorney

Some partial distributions are routine. Others are anything but routine.

Legal help becomes especially important when the trust language is unclear, a beneficiary challenges the trustee's judgment, the trust holds a business or hard-to-value asset, or tax and divorce issues may affect the distribution. A trustee should also get advice when personal liability starts to feel like a real concern instead of a distant possibility.

A lawyer can help in very practical ways. That may include interpreting the trust, reviewing reserve decisions, preparing a written distribution plan, coordinating with a CPA, or helping communicate with beneficiaries before a disagreement becomes a lawsuit. An experienced Texas estate planning attorney or Texas trust administration lawyer adds structure and protection to this process.

Families who are also thinking broadly about preserving wealth may find general resources on legal advice on asset management helpful for background reading. But when a trust is governed by Texas law, the trustee should get Texas-specific advice before acting.

If you're managing a trust, asking for a distribution, or trying to prevent a family conflict from getting worse, specific counsel matters. The right answer often turns on the exact trust language, the assets involved, and the trustee's documentation.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.