Managing a loved one's trust can feel overwhelming, but with the right legal guidance, it doesn't have to be. Many Texas trustees and beneficiaries start in the same place. They have a trust document in one hand, a tax question in the other, and no clear sense of what gets taxed, who reports it, or when action is required.

A common first question is simple: if money comes out of a trust, is it taxable? Sometimes yes. Sometimes no. The answer usually depends on whether the distribution came from trust income or trust principal, how the trust is classified for federal tax purposes, and whether the trustee handled the distribution correctly.

Texas gives families an important advantage. There's no state income tax here, which can make trust distribution planning more efficient than it would be in many other states. Still, federal trust tax rules remain technical, and trustees must also satisfy fiduciary duties in Texas under the Texas Trust Code and related administration rules.

Navigating Trust Taxes in Texas A Guided Introduction

A new trustee often gets appointed during a hard season. Sometimes a parent has passed away. Sometimes a grandparent created a trust years ago, and now the family is trying to follow instructions while grieving, coordinating paperwork, and answering beneficiary questions.

Then the tax issues appear.

One beneficiary asks whether the distribution is taxable. Another wants to know why they received a Schedule K-1 instead of a check explanation. The trustee wonders whether they should keep income inside the trust or distribute it before year end. None of those questions means anyone has done something wrong. It usually means the trust has reached the point where careful administration matters.

Practical rule: A trust distribution is not taxed just because money changed hands. The tax result depends on what kind of money the trust distributed and how the trust accounts for it.

For many families, the confusion starts because the word distribution sounds broader than it is. In trust administration, one payment can represent income, principal, or a mix of both. Each category can be treated differently for federal tax purposes.

Texas trustees also carry legal responsibilities beyond taxes alone. The Texas Trust Code and general fiduciary standards require a trustee to act prudently, keep records, communicate appropriately, and administer the trust for the beneficiaries' benefit. That means tax reporting is part of a larger job. It isn't just form-filing. It's part of protecting the trust and the people who depend on it.

If you're trying to understand how trust distributions are taxed in Texas, the good news is that the rules become much more manageable once you separate the issues into clear parts.

The Texas Advantage No State Income Tax on Trusts

Texas starts from a favorable position. Texas has no state income tax, which means trust income planning often focuses on federal rules rather than a second layer of state income tax. That can simplify administration for trustees and reduce the tax drag beneficiaries might otherwise face.

For Texas residents, that matters in practical ways. A beneficiary who receives taxable trust income generally deals with federal income tax reporting, but not Texas state income tax on that same distribution. A trustee administering a Texas trust also avoids the extra complexity that can come with separate state fiduciary income tax systems.

Why this matters in real administration

When trustees decide whether to distribute trust income or retain it, they're balancing taxes, the trust's purposes, and beneficiary needs. Texas's no income tax environment gives that analysis a cleaner starting point. The trustee can focus more directly on federal trust taxation, cash flow, and fiduciary judgment.

Texas residents also benefit from the broader state tax structure. As explained in this discussion of whether Texas has an inheritance tax, families here often work within a more favorable state-level tax environment than families in many other states.

What the Texas advantage does not change

Texas does not remove federal trust taxation. If a trust earns income, federal rules still determine whether that income is taxed to the grantor, to the trust itself, or to the beneficiary. Texas also doesn't eliminate fiduciary responsibilities. Trustees still need sound accounting, proper records, and distribution decisions that match the trust instrument and Texas law.

A helpful way to think about it is this:

| Question | Texas effect |

|---|---|

| Is there Texas state income tax on trust income? | No |

| Do federal trust tax rules still apply? | Yes |

| Do trustees still owe fiduciary duties in Texas? | Yes |

| Can Texas's tax environment make planning more efficient? | Yes |

Texas doesn't make trust taxation disappear. It removes one layer, which gives trustees and beneficiaries a clearer field for planning.

That clearer field is one reason Texas remains attractive for families focused on preservation, administration efficiency, and long-term estate planning.

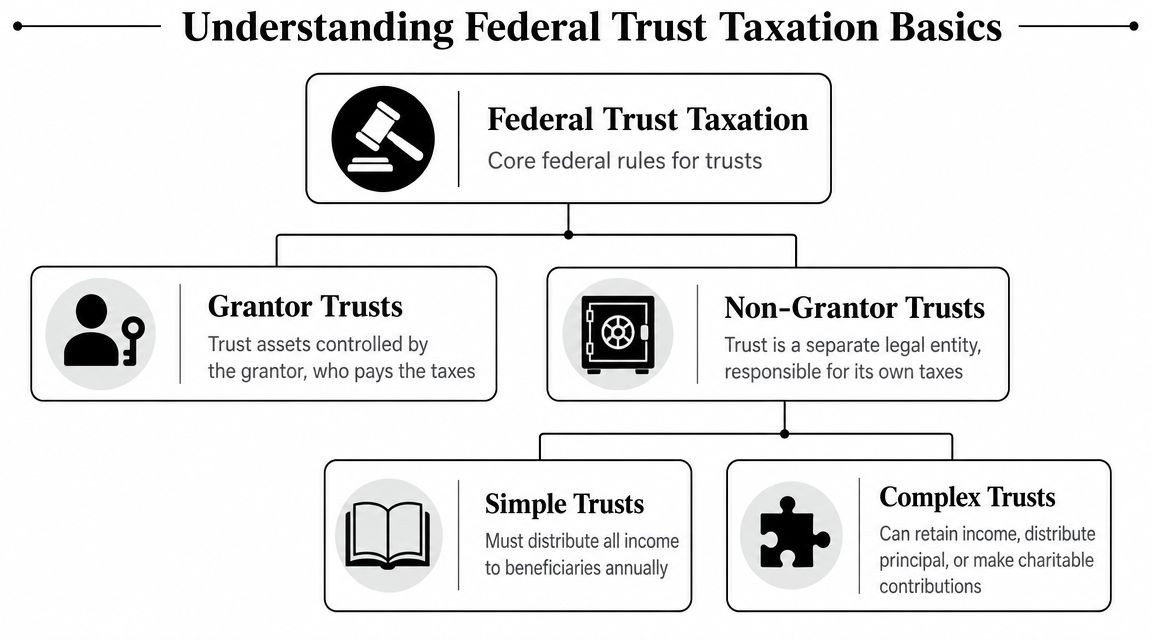

Understanding Federal Trust Taxation Basics

Before you can decide whether a distribution is taxable, you need to know what kind of trust you're dealing with. Federal law doesn't treat every trust the same. Some trusts are ignored for income tax purposes because the grantor pays the tax personally. Others are separate taxpayers that must file their own return.

Grantor trusts and non-grantor trusts

A grantor trust is one where the person who created the trust remains responsible for the income tax treatment. In everyday terms, the trust may exist for legal or estate planning reasons, but the IRS still looks through it to the grantor for income tax reporting.

A non-grantor trust is different. It stands as a separate taxpayer. It typically has its own taxpayer identification number and files its own federal fiduciary income tax return on Form 1041.

That distinction matters because non-grantor trusts can face steep federal tax pressure. According to this Texas trust taxation overview, irrevocable trusts in Texas can remove assets from the grantor's taxable estate, and federal estate taxes can reach 40% on estates exceeding $13.61 million under IRC § 2001. The same source notes that irrevocable non-grantor trusts file Form 1041 with separate tax identification numbers and face compressed federal income tax brackets, with the top 37% rate applying to income exceeding $16,000.

Simple trusts and complex trusts

Inside the non-grantor category, trusts are often discussed as simple or complex.

A simple trust generally must distribute all income each year and usually doesn't distribute principal. A complex trust has more flexibility. It may retain income, distribute principal, or make certain other distributions allowed by the trust terms.

That difference affects tax outcomes because the trustee's distribution decisions affect who ends up reporting taxable income.

A plain-English way to understand DNI

Many trustees get stuck on the phrase Distributable Net Income, or DNI. The term sounds abstract, but the idea is practical. DNI acts like a measuring line. It helps determine how much trust income can pass out to beneficiaries for income tax purposes.

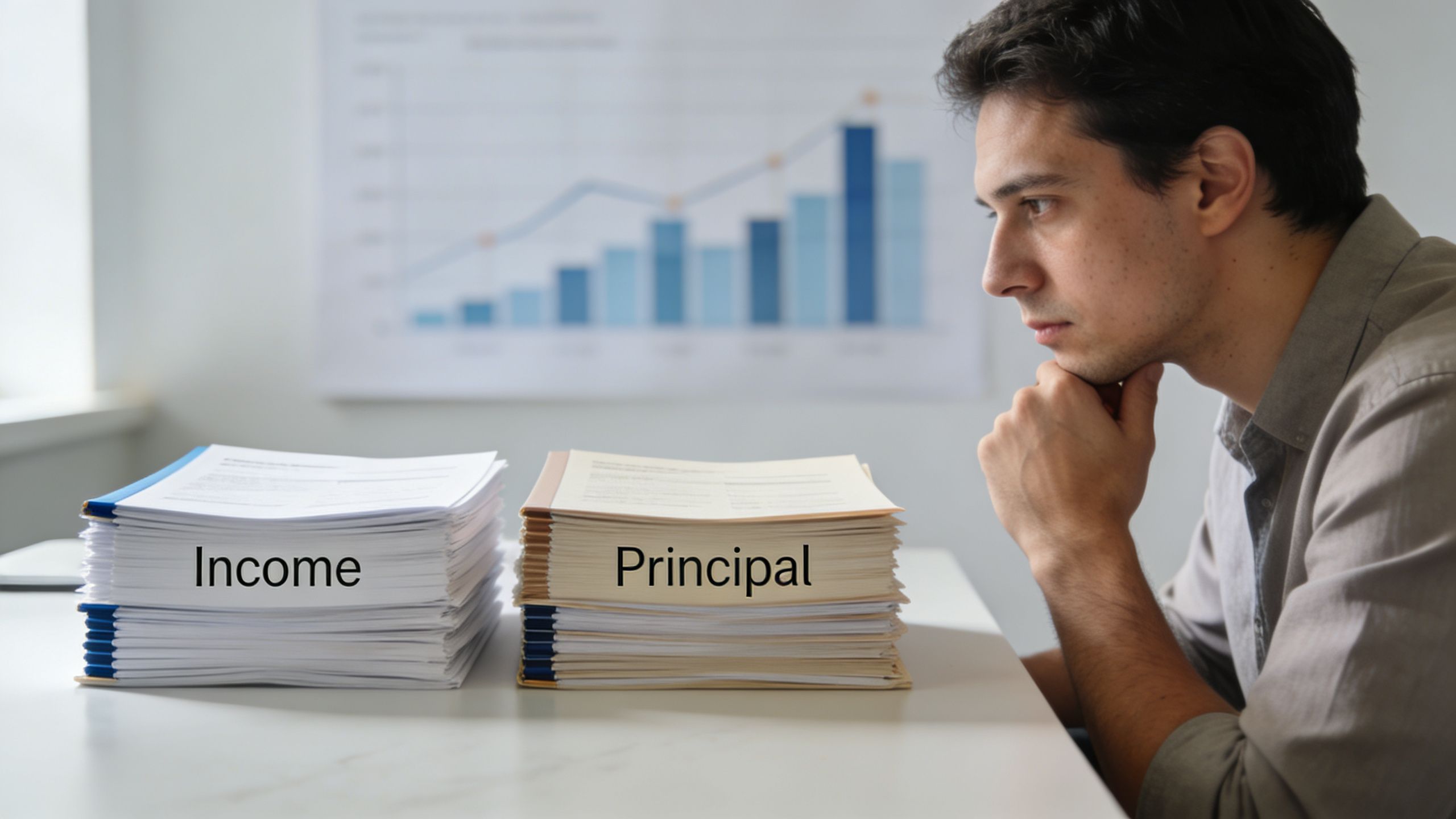

Think of a trust as a bucket with two compartments:

- Income compartment for items such as interest, dividends, or rent

- Principal compartment for the original property placed into the trust and other non-income amounts

DNI helps identify how much of the trust's taxable income can flow through to beneficiaries when distributions are made. It is not the same thing as the amount of cash distributed. A beneficiary can receive more cash than the taxable income portion.

Why trustees need this classification early

A trustee should identify the trust's tax character before making year-end decisions. That usually means reviewing:

- The trust instrument to see what the trustee must or may distribute

- Prior tax filings to confirm how the trust has been treated

- The trust's income sources so accounting matches tax reporting

- Fiduciary obligations in Texas so decisions remain consistent with the beneficiary's interests and the trust's purposes

The right classification affects filing, timing, and communication. It also shapes whether a family needs support from a Texas trust administration lawyer, a CPA, or both.

How Distributions Are Taxed to Beneficiaries

This is the question most beneficiaries ask first. If the trust sends you money, do you owe tax on it?

The most accurate short answer is this: income distributions are often taxable, while principal distributions generally are not.

Income and principal are not the same thing

A trust can hold cash, investments, real property, or business interests. Over time, those assets may produce income, such as interest or dividends. The trust also has its principal, which is the body of the trust property itself.

When a trustee distributes principal, that usually isn't taxable income to the beneficiary. When a trustee distributes current trust income, the tax result is often different. The beneficiary may need to report that income on a personal return, usually with information provided on a Schedule K-1.

This explanation of tax considerations for trust beneficiaries in Texas is useful for readers who want a broader beneficiary-focused discussion.

A concrete example of the distribution deduction regime

Federal trust taxation uses what many lawyers and accountants call the distribution deduction regime. The trust may deduct certain income distributions, and the beneficiary reports the income instead.

The example below shows why this matters. According to this discussion of whether a trust beneficiary pays tax, if a taxable trust earns $3,000 of income and the trustee distributes $5,000, the first $3,000 is taxable to the beneficiary, while the remaining $2,000 comes from principal and is not taxed as income. If only $1,000 is distributed, that $1,000 is taxable to the beneficiary and the remaining $2,000 is taxed at the trust level.

Here's that same idea in table form:

| Trust activity | Tax result |

|---|---|

| Trust earns $3,000 and distributes $5,000 | $3,000 taxable to beneficiary, $2,000 treated as principal |

| Trust earns $3,000 and distributes $1,000 | $1,000 taxable to beneficiary, $2,000 stays taxable to trust |

That's why beneficiaries are sometimes surprised. They may receive a distribution larger than the taxable amount. Or they may receive a smaller distribution and still hear that some trust income remained inside the trust.

Beneficiaries pay tax based on the character of what passed through, not simply on the size of the check.

Where the Schedule K-1 fits

When a trust distributes taxable income, the beneficiary usually receives a Schedule K-1. That form tells the beneficiary what type of income the trust passed through. The trustee doesn't just decide this informally. The trust's accounting records and tax return should support it.

Trustees should be careful here. Calling a payment a “principal distribution” in an email doesn't settle the tax issue if the trust's books and return show that current-year income passed out with the distribution.

For readers who prefer a visual explanation, this overview may help clarify the flow from trust income to beneficiary reporting.

Where readers often get confused

A few issues repeatedly cause confusion:

- Cash does not equal taxable income. A beneficiary may receive cash that is partly taxable income and partly principal.

- Principal isn't “free money” in every sense. It usually isn't taxable as current income to the beneficiary, but it still must be tracked correctly in fiduciary accounting.

- Basis matters when assets are sold. If a trust distributes an asset instead of cash, later tax consequences may depend on the asset's basis. That's a separate issue from whether the distribution itself is current taxable income.

- Capital gains need careful review. Trusts don't automatically treat capital gains the same way as ordinary trust accounting income. The governing instrument, accounting treatment, and tax reporting position all matter.

For a new trustee, the safest mindset is simple. Ask two questions before any distribution: what is this payment made of, and how will the trust report it?

The Trustee's Role and Filing Duties in Texas

A trustee is not just a check signer. Under the Texas Trust Code and general fiduciary principles, a trustee must administer the trust with care, loyalty, and discipline. Taxes are part of that duty, not a side task.

What a trustee usually needs to do

For a trust that is a separate taxpayer, the trustee generally needs to handle federal fiduciary income tax reporting. That includes Form 1041 and any beneficiary reporting documents required for taxable distributions.

Texas law also expects trustees to maintain clear records and account properly. The verified materials state that Texas Trust Code § 113.051 requires annual CPA reviews and strategic distribution planning to optimize tax treatment, and that the timing and structure of year-end distributions can materially change tax outcomes for both trusts and beneficiaries, as discussed in this review of grantor trust taxation for Texas residents.

A practical trustee checklist often includes:

- Track receipts and disbursements carefully. Separate income items from principal transactions.

- Review the trust document before distributing funds. The trustee's authority comes from the instrument first, then applicable law.

- Coordinate tax reporting. If the trust distributed taxable income, beneficiaries may need timely K-1s.

- Document discretionary decisions. Good records help show the trustee acted prudently and consistently.

Why records matter so much

Trust accounting is where many tax problems begin or end. If the books don't clearly show what the trust earned, what it retained, and what it distributed, the trustee can't confidently support the return.

That recordkeeping duty also ties directly to fiduciary duties in Texas. Beneficiaries are entitled to transparency consistent with the trust terms and Texas law. A trustee who can explain distributions with organized records is in a much stronger position than one working from memory, bank statements, and scattered emails.

Clean trust administration usually looks quiet from the outside. Behind the scenes, it depends on disciplined accounting, timely filings, and documented decisions.

When legal guidance helps

Some trusts are straightforward. Others involve mixed asset classes, family tension, or uncertain drafting. In those situations, trustees often benefit from a coordinated team that may include tax preparers and legal counsel. A Texas estate planning attorney or Texas trust administration lawyer can help interpret distribution standards, review fiduciary risk, and address disputes before they grow.

Trust administration also intersects with related planning areas, including estate planning, probate, guardianship, and asset protection. Families often need those issues reviewed together rather than in isolation.

Strategic Tax Planning for Texas Trusts

Good trust administration is not only about filing correctly. It's also about making thoughtful decisions before the tax year closes. In Texas, that planning can be especially effective because the state doesn't add an income tax layer on top of federal trust taxation.

Why retaining income can become expensive

For non-grantor trusts, federal tax brackets compress quickly. According to this discussion of tax strategies for Texas trusts, the 2026 projected federal income tax brackets for non-grantor trusts place the 37% rate on income over $16,000, and when trustees distribute that income, the trust may claim a distribution deduction while the beneficiary reports the income instead, potentially at lower personal rates. The same source explains that Texas's lack of state income tax makes these federal planning moves especially meaningful.

That doesn't mean trustees should always distribute income. The trust's terms still control, and the trustee must consider beneficiary needs, creditor protection goals, and the purpose of the trust. But it does mean that letting income sit inside a non-grantor trust without analysis can be a costly default.

Planning questions a trustee should ask before year end

A practical review often starts with a few direct questions:

- Has the trust earned income that could be distributed under the instrument?

- Would a distribution align with the trust's purpose and the beneficiaries' circumstances?

- Will retaining income inside the trust create unnecessary federal tax exposure?

- Are the records strong enough to support the intended tax treatment?

Those questions are often more useful than jumping immediately into jargon.

Common mistakes to avoid

Some of the most common administration problems are simple:

- Waiting too long to review year-end options. Timing can affect whether a distribution achieves the intended tax result.

- Confusing cash needs with tax efficiency. A beneficiary may need support, but the trustee still must classify the payment correctly.

- Treating all beneficiaries the same without reviewing trust language. Distribution standards often differ by person or purpose.

- Ignoring professional coordination. Tax, fiduciary, and drafting issues often overlap.

The Law Office of Bryan Fagan, PLLC offers services involving trust administration, tax planning, and related estate matters. For many families, that kind of legal review works best alongside a tax preparer who can model the reporting consequences.

A trustee's best tax move is rarely accidental. It usually comes from early review, careful classification, and a distribution plan that fits the trust document.

When families ask how trust distributions are taxed in Texas, the answer is often half law and half timing.

Get Trusted Guidance for Your Texas Trust

Trust taxation becomes easier once the moving parts are separated. Texas offers a meaningful advantage because there's no state income tax, but federal rules still determine whether trust income is taxed to the grantor, the trust, or the beneficiary. Trustees also have to honor fiduciary standards, maintain reliable records, and make distribution decisions that match the trust's terms.

That combination is why many trustees feel pressure. They're not only managing numbers. They're managing family expectations, legal duties, and deadlines.

A strong support team helps. Many trustees work with lawyers, financial advisors, and CPAs so tax reporting and fiduciary administration stay aligned. That's especially helpful when a trust holds investments, real estate, or assets that produce different kinds of income.

If you're a beneficiary, clear guidance can help you understand whether a payment is likely taxable income or a principal distribution. If you're a trustee, the right advice can help you prepare Form 1041 reporting, evaluate year-end distribution choices, and reduce the risk of preventable disputes.

If you're managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.

If you're managing a trust or planning your estate, schedule a free consultation with Law Office of Bryan Fagan, PLLC. The firm advises Texas families, trustees, beneficiaries, and fiduciaries on trust administration, estate planning, probate, guardianship, and asset protection, with guidance developed for your specific trust terms and tax concerns.