Managing a loved one's trust can feel overwhelming, especially when your own finances tighten at the same time. A trustee often has access to trust accounts, sees available cash, and wonders whether a short-term loan would really hurt anyone if it's repaid promptly.

That question comes up more often than many families expect. The problem is that trust law doesn't look at this the way a bank or a family member might. Texas law treats a trustee as a fiduciary first, which means the trustee's personal needs come second.

If you're asking can a trustee loan money from the trust to themselves, the safest starting point is simple. Usually, no. In Texas, a self-loan is usually viewed as self-dealing unless it fits within a narrow legal exception and is handled with careful documentation, full disclosure, and often court involvement.

A Trustee's Dilemma When Personal Finances and Trust Duties Collide

A common scenario looks like this. An adult child becomes trustee after a parent's death. The trust owns investment accounts, maybe a house, maybe cash. Then the trustee faces a personal emergency. A medical bill arrives, a business has a cash crunch, or a home repair can't wait.

From the trustee's point of view, the idea may seem reasonable. “I'm not stealing anything. I'll borrow it, sign a note, and pay it back.” That thought is understandable. It's also where many trustees get into trouble.

The confusion comes from wearing two roles at once. You may be a trustee, a beneficiary, and a family member. But Texas law separates those roles very carefully. Money in the trust isn't your personal reserve fund just because you control the account or expect to inherit from it later.

Practical rule: Access is not ownership. A trustee manages trust property, but manages it for the beneficiaries and under the trust's terms.

That's why even a well-meaning trustee can create a serious legal problem by moving trust money to a personal account, calling it a temporary advance, or planning to paper the deal later. Courts often view that sequence as backwards. The authority must exist first. The documentation must exist first. The protection for beneficiaries must exist first.

This matters even more in family trusts, where informal decisions are common. Families often say, “We all trust each other.” That may be true until accountings are requested, circumstances change, or one beneficiary feels left out. Then an undocumented “loan” can quickly become the center of a trust dispute.

The Fiduciary Duty of Loyalty and the Rule Against Self-Dealing

The fiduciary duty of loyalty is central to Texas trust law. In plain English, a trustee must put the beneficiaries' interests first and keep personal interests out of trust decisions. That sounds simple until the trustee is the one asking for the money.

Why self-loans are treated so harshly

A trustee self-loan puts one person on both sides of the transaction. As trustee, you are supposed to demand terms that protect the trust. As borrower, you want lower interest, looser deadlines, and less risk to yourself. Texas law treats that conflict with real suspicion because no trustee can negotiate at arm's length with themselves in the ordinary way.

That is why Texas Property Code § 114.061 generally treats self-dealing transactions as improper unless a valid exception applies. If you want a fuller explanation of how Texas courts view this obligation, this guide on fiduciary duties of trustees in Texas explains the rule in more detail.

A useful comparison is a referee who decides their own game. Even if that referee tries to be fair, the structure is flawed from the start. Trust law works the same way. The problem is not only bad intent. The problem is a conflicted position.

Good intentions usually do not solve it

Trustees often say the same few things when a personal loan from the trust seems harmless:

- I was going to pay it back

- I would have paid interest

- The trust was not going to miss the money

- I am a beneficiary too

Those facts may matter later on damages or remedies, but they usually do not erase the breach itself. Texas courts focus first on authority and process. The trustee needs legal permission before taking trust funds for personal use, not an explanation after the fact.

That point confuses many families. They assume a loan is different from a withdrawal because a loan gets repaid. Sometimes that is true in ordinary banking. In trust administration, the first question is whether the trustee had authority to enter the deal at all, and whether the deal was structured to protect the beneficiaries as if a stranger were borrowing the money.

Courts also look hard at timing. If trust money is transferred first and the paperwork appears later, the transaction already looks suspect. A promissory note signed after the fact often reads less like proper administration and more like damage control.

If you want to see how courts and practitioners discuss disputes over fiduciary conduct in the estate planning field, you can find caseledge reviews for estate planning.

The practical lesson is straightforward. A trustee cannot treat trust assets like a personal line of credit just because repayment seems likely. Under Texas law, loyalty means the trustee must protect the trust first, document authority first, and avoid self-dealing unless the law and the trust instrument clearly permit it.

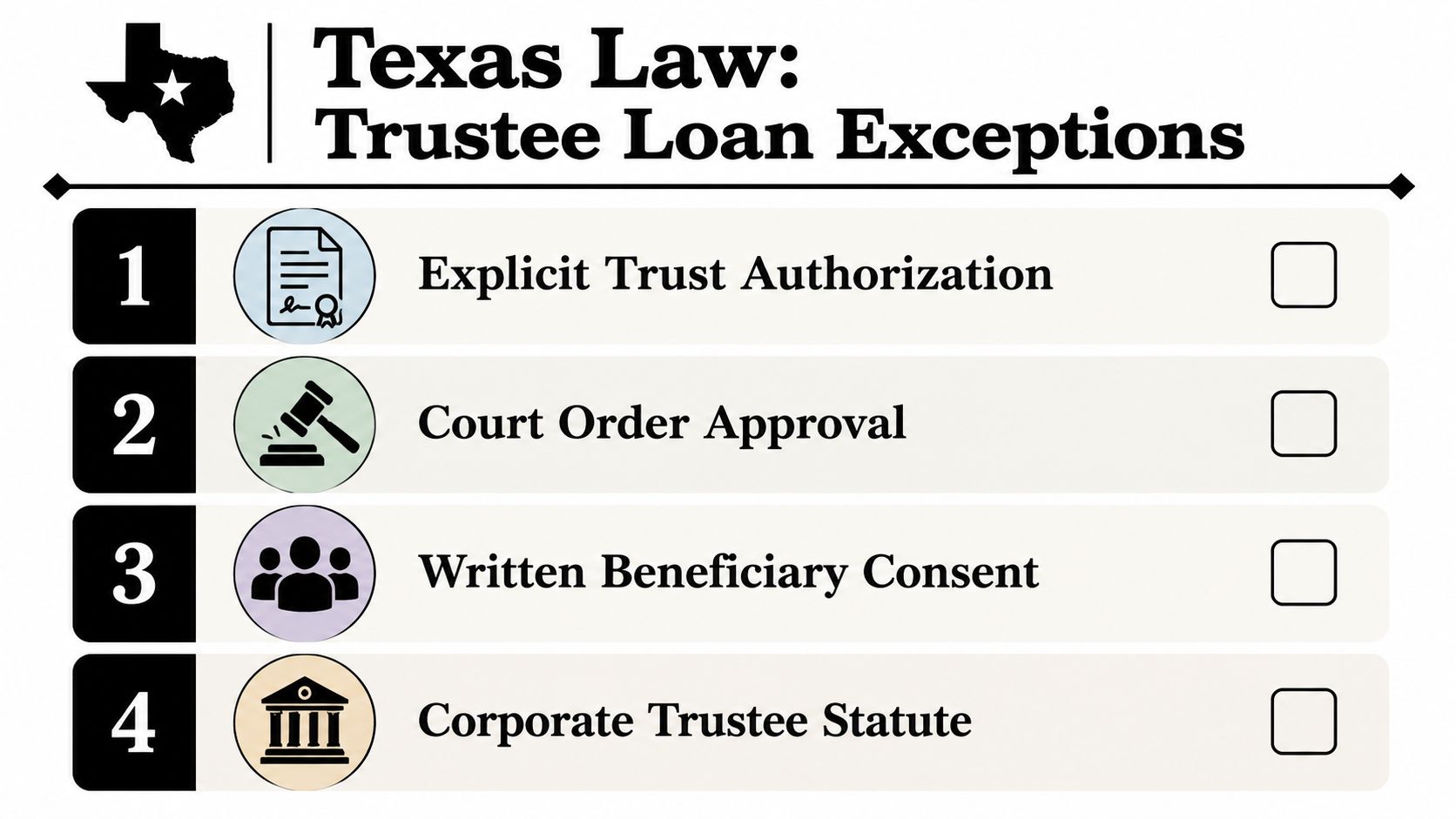

Navigating the Limited Exceptions Under Texas Law

The general rule is restrictive, but Texas law does leave a few narrow openings. The key word is narrow. A trustee shouldn't assume an exception applies just because the arrangement sounds fair.

Express authorization in the trust document

The first question is always the trust agreement itself. Trustees only have the powers the trust instrument gives them. Authority to borrow from the trust cannot be implied from broad management language or from a general power to make loans.

That means language allowing the trustee to invest assets, manage accounts, or lend trust money to others usually isn't enough. A self-loan needs clear, specific authorization.

The distinction matters because trustees possess only those powers explicitly granted by the trust instrument, and a self-loan requires documentation comparable to a third-party commercial loan, including financial information, repayment ability, collateral, and compliance procedures, as described in this discussion of express trustee powers.

A careful review should answer questions like these:

- Does the trust specifically permit loans to the trustee?

- Does it limit when or why those loans can happen?

- Does it require interest, collateral, or notice to beneficiaries?

- Does it name another person who must approve the transaction?

If the document is vague, that usually helps the beneficiaries, not the trustee.

Informed consent from all beneficiaries

Texas also recognizes a consent-based path. Under Texas Property Code § 114.063(b), a trustee may avoid a self-dealing challenge if all beneficiaries are competent, fully informed, and consent.

Many trustees make a second mistake at this stage. They get a casual “sounds fine” from one sibling and assume that solves it. It doesn't. Consent should be informed, complete, and written. Every material fact should be disclosed before money moves.

That means the beneficiaries should know:

| Issue | What should be disclosed |

|---|---|

| Loan amount | The exact amount requested |

| Terms | Interest rate, maturity date, payment schedule |

| Risk | What happens if the trustee can't repay |

| Security | Whether collateral is pledged |

| Effect on trust | Whether the loan affects distributions, liquidity, or investment plans |

If even one beneficiary is a minor, incapacitated, or otherwise unable to give legal consent, the process becomes much harder and may require court involvement.

A Texas example shows the risk. As noted in this Texas-focused discussion of trustee self-dealing, Texas Property Code § 114.061 prohibits self-dealing unless the trust authorizes it, while § 114.063(b) allows an exception if all beneficiaries are competent, fully informed, and provide consent. That same source notes a 2023 Texas probate court case, In re Estate of Jackson, in which a trustee was surcharged $150,000 for an unauthorized loan to himself.

For a more focused look at this issue, this page on trustee self-dealing in Texas is worth reviewing.

Full disclosure means more than naming the amount. It means disclosing the conflict, the terms, the risks, and the alternatives.

If you want to compare how courts and clients evaluate legal service issues in estate matters, resources like find caseledge reviews for estate planning can help you see how others approach trust and estate representation.

Court approval before any transaction

The third pathway is asking a court for approval. This is often the cleanest legal route when the trust language is unclear or beneficiary consent isn't available. It is also the most formal.

A trustee who seeks court approval should expect scrutiny. The court will want to know why a self-loan is necessary, whether it benefits the trust or at least protects the beneficiaries, and whether the terms are fair enough that an independent lender might accept them.

In practice, that usually means gathering a full package of documents, such as:

- The trust agreement and any amendments

- A written petition explaining the request

- A promissory note with market-style loan terms

- Collateral documents if any property secures repayment

- Financial records showing ability to repay

- Notice materials for all beneficiaries

This is not a do-it-yourself situation. A trustee who asks for approval after already taking the money is in a much weaker position than a trustee who seeks permission first.

A practical point trustees often miss

Even if one of these exceptions might apply, the process must still look and function like an arm's-length business transaction. Informality is the enemy here. A handwritten note, a verbal promise, or a transfer described later as a “temporary loan” won't usually inspire confidence in court.

The High Stakes of an Improper Trustee Loan

Improper trustee loans don't just create awkward family conversations. They can create personal liability, litigation, removal, and major financial exposure for the trustee.

A broader litigation pattern supports that concern. A 2023 analysis of over 5,000 trust litigation cases found that 42% were tied to self-dealing, including improper loans. The same source describes a 2020 Dallas Probate Court case, In re Trust of Smith, in which a trustee was ordered to repay a $750,000 self-loan plus $300,000 in punitive damages.

What a trustee may face

When a self-loan goes wrong, courts have several remedies available. They can order the trustee to repay money, pay additional damages, and step aside from the role.

The consequences often include:

- Repayment from personal funds if trust money was used improperly

- Surcharge liability for losses tied to the breach

- Punitive or other enhanced damages in more serious misconduct cases

- Removal as trustee and appointment of a replacement

- Attorney fee exposure for both sides of the dispute

If you're concerned about that risk, this explanation of trustee personal liability in Texas helps show how quickly a trustee's personal finances can become involved.

Why repayment alone may not save you

A trustee sometimes says, “I already paid it back, so the issue is over.” Courts may disagree. The breach often occurs when the trustee puts personal interest ahead of fiduciary duty, not only when the trust suffers an unrecovered loss.

That's why beneficiaries often focus on records. Bank statements, checks, transfer logs, emails, and accounting gaps can all become evidence. A transaction that felt informal inside the family can look very different once a judge reviews it line by line.

This short video gives added context on how these disputes can unfold in real life.

An improper trustee loan is rarely judged by your intent alone. It is judged by authority, process, disclosure, and loyalty to the beneficiaries.

Safer and Practical Alternatives to a Trustee Self-Loan

A common trustee problem looks like this. You need cash for a short-term personal issue, the trust account is funded, and you tell yourself you will repay every dollar with interest. In Texas, that is the moment to stop and look for a cleaner path.

The safer options usually depend on one simple question. Are you trying to access money because the trust allows you to receive it, or because you control the account as trustee? Texas law treats those as very different situations. Your right as a beneficiary comes from the trust terms. Your authority as trustee comes with duties and strict limits.

Compare the alternatives before touching trust funds

A practical way to sort this out is to compare the available paths as if you were advising someone else. That mental shift helps. Trustees often make better decisions when they stop viewing the trust as a family reserve and start viewing it as property they manage for others.

| Option | Why it may be safer | Main caution |

|---|---|---|

| Beneficiary distribution | Uses a right created by the trust, if the trust permits it | Must match the distribution standard and trust terms exactly |

| Commercial bank loan | Keeps the transaction at arm's length | Approval, rate, and collateral terms may be demanding |

| Resignation and successor review | Lets an independent trustee evaluate the request | Only helps if the trust and facts support the transaction |

| Use of personal assets | Avoids fiduciary conflict with trust property | May strain your personal cash flow or other assets |

Four options that usually reduce risk

1. Review whether a distribution is allowed.

If you are also a beneficiary, start with the trust language. Does it allow mandatory distributions, discretionary distributions for health, education, maintenance, or support, or some other present right to receive funds? A proper distribution is not a disguised loan. It is more like using the correct door instead of climbing through a window. The trustee still has to follow the written standard and document why the distribution fits.

2. Borrow from a third-party lender instead.

A bank, credit union, or private lender has no fiduciary duty to the trust beneficiaries. That distance matters. You may pay more in interest, but you avoid the core problem of using a position of trust for personal benefit.

3. Consider whether a successor trustee should evaluate the request.

Sometimes the conflict is the actual problem, not the need for money itself. If the trust document allows a change in trustees, an independent successor may be able to review whether any transaction is permitted under Texas law and under the trust terms. That does not automatically make a loan proper, but it removes your direct control from the approval process.

4. Use other personal borrowing channels and document them carefully.

Home equity credit, securities-backed lending, or a family loan outside the trust may be less risky than touching trust assets. If you want a starting point for what formal loan terms usually look like, tools that support AI-assisted legal document drafting can help you understand the basic structure. For any transaction connected to a trust, though, form documents are not enough. The trust instrument and Texas fiduciary rules still control.

The best alternative depends on the hat you are wearing

If you are serving only as trustee, the practical answer is usually simple. Keep your personal borrowing separate from the trust.

If you are both trustee and beneficiary, slow down and separate those roles on paper before making any move. A beneficiary may have a real right to receive money. A trustee does not get to create that right by calling a personal withdrawal a loan. That distinction is where costly mistakes often begin.

Protecting the Trust and Yourself with Professional Guidance

A trustee's job often looks straightforward from the outside. Pay bills, manage assets, keep records, make distributions. In practice, even one decision can carry personal risk if it mixes family relationships with fiduciary authority.

That's exactly why the question can a trustee loan money from the trust to themselves needs a careful Texas-specific answer. The broad rule is no. The exceptions are narrow. And the paperwork, disclosures, and legal standards are far stricter than typically assumed.

A short checklist before taking any action

Before moving a dollar, a trustee should stop and work through these steps:

- Read the trust document carefully for any express authority or restrictions

- Separate your beneficiary rights from your trustee powers

- Avoid any transfer that hasn't been documented and approved first

- Communicate openly with beneficiaries when disclosure is required

- Keep trust funds separate from personal funds at all times

Trustees who slow down and get advice early usually avoid the costliest mistakes.

This issue also connects to other parts of estate planning and administration. Families often need help coordinating trust decisions with estate planning services, probate guidance, and guardianship matters, especially when a beneficiary is a minor or an incapacitated adult.

A trustee doesn't need to guess through this. Careful legal review can often identify whether a distribution is possible, whether court approval is necessary, or whether the safest answer is to avoid the transaction entirely.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process. Whether you need help as a trustee, beneficiary, or family member, we can help you understand your duties, avoid self-dealing problems, and move forward with confidence.