Skip to content

Skip to content Managing a loved one's trust can feel overwhelming. You may be holding a folder full of account statements, property tax notices, insurance bills, and emails from family members, while wondering one basic question: what expenses can a trustee legally charge in Texas?

That question matters because a trustee has two duties at the same time. You have to protect the trust, and you have to treat beneficiaries fairly. If you pay trust expenses too loosely, beneficiaries may think you're helping yourself. If you pay too cautiously, you may end up covering legitimate trust costs out of your own pocket.

Texas law gives trustees room to be paid fairly and reimbursed for proper trust costs. It also expects careful records, honesty, and sound judgment. Most problems don't start with bad intent. They start with poor documentation, unclear communication, or mixing up compensation with reimbursement.

A newly appointed family trustee often worries about three things:

- Getting accused of taking too much

- Missing expenses that should be paid by the trust

- Not knowing how to explain charges to beneficiaries

Those concerns are normal. They're also manageable when you understand the rules and keep good records from the beginning.

Your Guide to Navigating Trustee Expenses in Texas

You have just stepped into the trustee role. A property insurance bill is due, the investment advisor wants instructions, and a beneficiary is already asking whether the trust can pay for repairs at the house. Before long, a simple question starts carrying a lot of weight: which expenses belong to the trust, and how do you show that you handled them properly?

That second question matters more than many first-time trustees expect.

Texas law generally allows a trustee to receive reasonable compensation if the trust instrument does not provide a different rule, and it also permits repayment of proper trust expenses. But the legal answer is only part of the job. A trustee also owes fiduciary duties. In plain terms, that means you must act with care, loyalty, and fairness, and you should be ready to explain your decisions with records that make sense to someone else reading them later.

A good way to approach trustee expenses is to treat every charge as if you may need to explain it to a skeptical but reasonable family member six months from now. If you cannot show what was paid, why it was necessary, and how it benefited the trust, the problem is often not the expense itself. The problem is the missing paper trail.

Here is the practical rule many family trustees need at the start:

Practical rule: If a cost was necessary to administer, protect, preserve, or account for the trust, it may be payable from the trust. If the cost mainly benefited you personally, it usually should not be charged to the trust.

Disputes often originate when a trustee pays a bill that seems obvious at the time, but saves no invoice, writes no note about the purpose, and gives beneficiaries no clear explanation. Later, the same payment can look suspicious even if it was perfectly proper. Clear documentation often prevents that shift in perception.

It helps to picture the trust as a separate financial household. Its bills should be identifiable. Its records should stand on their own. Your notes should answer basic questions without forcing beneficiaries, accountants, or a court to guess what happened.

From the beginning, keep four habits in place: read the trust terms carefully, separate compensation from reimbursement, save receipts and statements, and communicate charges in a way beneficiaries can follow. Those habits do more than keep the books tidy. They reduce misunderstanding before it turns into conflict.

Trustee Compensation vs Reimbursable Expenses

The easiest way to understand this is to think like a business manager. A manager can receive pay for doing the job. The business can also repay that manager for money spent on office supplies, travel, or filing costs. Those are not the same thing.

A trustee works the same way. Compensation is payment for your time, effort, judgment, and responsibility. Reimbursable expenses are repayments for trust-related costs you advanced or paid directly on the trust's behalf.

Why the distinction matters

This distinction affects more than bookkeeping. It shapes how you explain charges to beneficiaries, how you report them for tax purposes, and how a court may view your conduct if someone challenges your records.

Compensation often invites closer scrutiny because people naturally ask whether the amount is fair. Reimbursement usually turns on a simpler question: was the expense legitimate, necessary, and tied to trust administration?

A trustee should be able to show, in one sentence, why each payment belonged in either the compensation column or the reimbursement column.

Trustee Compensation vs. Reimbursable Expenses at a Glance

| Attribute | Trustee Compensation | Reimbursable Expense |

|---|---|---|

| Purpose | Pays the trustee for work, responsibility, judgment, and oversight | Repays the trustee for money spent for the trust |

| Common examples | Administration time, handling beneficiary issues, overseeing assets | Property taxes, insurance, travel, legal bills, accounting costs |

| How beneficiaries view it | Often questioned if the amount seems high or vague | Usually accepted if supported by receipts and a clear trust purpose |

| Documentation needed | Time records, fee method, explanation of duties performed | Receipts, invoices, mileage logs, account statements |

| Key legal question | Was the amount reasonable? | Was the cost properly incurred for the trust? |

| Tax treatment | Depends on how the payment is characterized and reported | Reimbursement generally restores money spent, not pay for services |

A simple example

Suppose you drive to inspect a trust-owned home after a storm. If you charge for your time spent managing the issue, that's compensation. If you paid for gas, tolls, or temporary locks for the property, those out-of-pocket costs are potential reimbursements.

If you hire a CPA to prepare trust tax filings, the CPA's invoice is a trust expense. If you spent hours gathering records, speaking with the CPA, and making judgment calls, your time may be part of trustee compensation.

The confusion usually starts when trustees bundle everything into one vague line item like “administration costs.” That invites questions. A better approach is to separate entries clearly:

- Compensation for trustee services

- Reimbursement for travel

- Reimbursement for legal invoice

- Reimbursement for property insurance payment

That cleaner system protects everyone involved.

Determining Reasonable Trustee Compensation in Texas

You have been handling a parent's trust for months. You paid property bills, fielded calls from beneficiaries, met with the CPA, and dealt with a leaking roof at a trust-owned house. Then the practical question shows up. How much can you pay yourself, and how do you explain it without starting a family fight?

Texas law gives trustees room, but not guesswork. Under Texas Trust Code Section 114.061(a), a trustee is generally entitled to reasonable compensation from trust assets unless the trust says otherwise. The hard part is not finding a single number. The hard part is choosing a method you can defend later with clear records and a sensible explanation.

That is why a family trustee should treat compensation like setting the price on careful, documented work, not like taking a draw from a family account. The fee has to fit the job, the trust, and the results. It also has to be communicated in a way that shows you are honoring your fiduciary role. A useful summary of Texas trustee duties and compensation standards explains the factors courts may consider, such as time spent, the nature of the assets, the responsibility involved, the trustee's skill, and the care shown in carrying out the trust.

What “reasonable” usually means in real life

Reasonable compensation is context-driven. A trustee overseeing one investment account with automatic statements usually has a lighter workload than a trustee managing rental property, mineral interests, tax filings, family conflict, or a lawsuit. Same title. Very different job.

That is where many new trustees get uneasy. They want a formula, but Texas law works more like a fairness test. Judges and beneficiaries often look at the full picture. What did you do? How difficult was it? Did the trust benefit? Would the amount make sense to an outside observer reviewing your records a year later?

A good way to approach this is to pick one fee method and write down why it fits the trust.

A practical checklist before you set your fee

- Read the trust first. Some trusts set compensation, limit it, or waive it.

- Choose a fee method that matches the work. Hourly fees often fit irregular or labor-intensive administration. A flat annual fee can work for a smaller trust with steady tasks. Percentage-based fees are more common when asset management is the main job.

- Describe your duties specifically. “Trust administration” is too vague. “Reviewed insurance renewal, met with plumber, prepared beneficiary update, coordinated 1041 tax documents” is far better.

- Account for complexity. A trust holding a house, business interest, or difficult family dynamics usually requires more judgment than a simple brokerage account.

- Compare the amount to what an experienced trustee or professional fiduciary might charge in your area. You do not need a perfect market study, but you do need a reality check.

- Write down your reasoning before you pay yourself. If your explanation is thin on paper, it will usually sound thin to a beneficiary.

That last step prevents problems.

Why compensation disputes usually start

Beneficiaries rarely object just because a trustee is paid. They object when the charge feels sudden, vague, or self-serving. A line item that says “trustee fee, $8,500” with no explanation tends to raise suspicion. A monthly or quarterly record showing dates, tasks, hours, and the method used is much easier to understand.

Compensation works a lot like home repair billing. If a roofer sends an invoice that only says “roof work,” you would have questions. If the invoice lists inspection, materials, labor, and photos of the damage, the charge is easier to evaluate. Trustee compensation is similar. Clear support does not guarantee agreement, but it makes disagreement much less likely.

This short overview helps explain the legal framework in video form:

A safer way to document and communicate compensation

If you are a non-professional trustee, consistency matters more than sophistication. You do not need a complicated billing system. You need records that another person can follow.

A strong process often looks like this:

- Keep a contemporaneous log. Record the date, task, time spent, and why the task mattered to the trust.

- Separate compensation from reimbursements. Your time is one category. Out-of-pocket costs are another.

- Use regular reporting periods. Monthly or quarterly summaries reduce the shock of a large charge appearing all at once.

- Explain your method in plain English. State whether you used an hourly rate, flat fee, or another approach, and why that method fits the trust.

- Preserve backup documents. Emails, invoices, statements, calendars, and meeting notes help show the work was real and trust-related.

The best fee record is usually the least dramatic one. It reads clearly, matches the trust's needs, and gives beneficiaries very little to guess about.

If you serve as both trustee and beneficiary, be extra careful. That dual role does not prevent compensation, but it does invite closer scrutiny. In that situation, clear disclosure and legal advice before paying yourself can prevent a much larger dispute later.

A Practical Guide to Permissible Reimbursable Expenses

Reimbursement is simpler than compensation, but it still requires discipline. A trustee can generally recover proper out-of-pocket costs incurred while administering and protecting the trust. The key word is proper.

Corporate trustees in Texas commonly charge 0.75% to 1.25% of annual asset value for compensation, plus 100% reimbursement for direct costs such as property taxes, insurance, and legal or accounting fees, which can range from $5,000 to $50,000 per filing. These expenses are also fully deductible to the trust on IRS Form 1041, according to this explanation of Texas trust fees and trust accounting practices.

Common expense categories trustees can often charge

Many reimbursable expenses fall into familiar groups. The trust paid for the benefit, not for the trustee personally.

- Property-related costs. This includes insurance, taxes, storage, maintenance, and necessary repairs for trust-owned real estate or personal property.

- Professional fees. Lawyers, accountants, tax preparers, appraisers, and similar professionals are often necessary to administer the trust correctly.

- Administrative costs. Postage, copies, bank charges, delivery fees, and document handling costs may be appropriate if they relate directly to trust business.

- Travel and inspection costs. If you must visit trust property, meet professionals, or handle trust administration in person, those direct travel expenses may be reimbursable.

- Taxes paid on behalf of the trust. Tax obligations tied to trust administration are generally trust expenses, not personal trustee costs.

What this looks like in real life

Suppose a trust owns a house in Texas after the settlor's death. The trustee may need to pay homeowner's insurance, utility bills while the property is being preserved, and a lawyer to review a sale contract. Those are classic trust expenses.

Or suppose the trust holds valuable items in storage while the family decides how they should be distributed. Storage fees may be reimbursable if the trustee can show that the cost preserved trust property.

If you'd feel uncomfortable explaining the expense line-by-line to every beneficiary in the same room, pause before charging it to the trust.

Expenses that often create confusion

Not every cost is clearly allowed just because it touches trust business. Some items need closer judgment.

Repairs versus improvements

Fixing a roof leak to prevent damage is easier to justify than installing luxury upgrades before a sale. Necessary repairs usually fit trust administration better than optional improvements. Major projects should be supported by written bids, a reason for the decision, and records showing how the project served the trust.

Personal convenience costs

If you buy a laptop mainly for your own use, charging it to the trust may be hard to defend. If the trust requires secure document handling and the expense is tied directly to trust administration, the facts matter, making judgment and documentation critical.

Mixed expenses

Some costs have both personal and trust components. A common example is travel combined with a family visit. In those cases, trustees should allocate carefully and only seek reimbursement for the trust-related portion they can support with records.

Good reimbursement practice is simple: save the invoice, note the trust purpose, and record the payment promptly in the ledger.

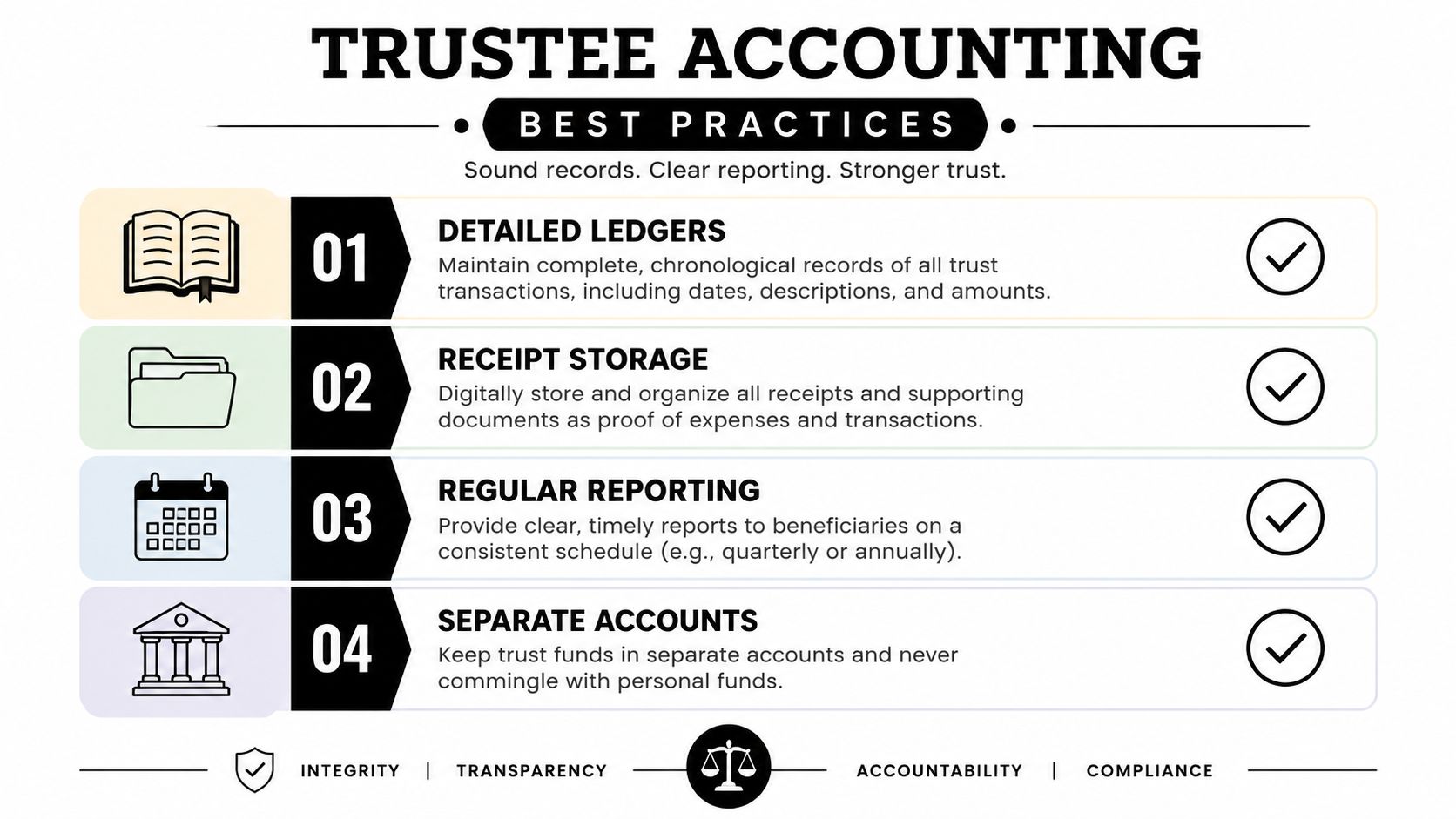

Best Practices for Accounting and Avoiding Disputes

Most trustee disputes don't begin with a shocking theft. They begin with missing receipts, vague ledger entries, delayed reporting, or beneficiaries who feel shut out. Good accounting is not busywork. It's one of the trustee's strongest forms of protection.

A useful starting point is to treat trust records with the same seriousness a careful business owner uses when managing business expenses. The systems are different, but the discipline is similar. Keep receipts, categorize transactions, and make sure every dollar has a clear purpose.

Four habits that prevent trouble

Beneficiaries usually calm down when the trustee's records are organized, timely, and easy to follow. They get suspicious when answers are delayed or incomplete.

- Use a separate trust account. Never mix trust money with your own money. Even innocent commingling creates risk.

- Keep a running ledger. Record every deposit, payment, reimbursement, and distribution as it happens.

- Save source documents. Receipts, invoices, statements, mileage notes, emails approving work, and tax filings all matter.

- Report regularly. Beneficiaries don't need a daily update, but they do need understandable accountings.

For trustees who want a stronger system, Texas fiduciary accounting guidance is especially helpful because accounting format often drives whether a dispute grows or fades.

How to describe charges clearly

A ledger entry like “miscellaneous trust costs” is weak. A ledger entry like “reimbursement for homeowner's insurance premium on trust-owned residence” is much stronger.

Use this format whenever possible:

- Date paid

- Who was paid

- Amount

- Trust purpose

- Category

- Receipt or invoice reference

That level of detail makes your records easier to defend and easier for beneficiaries to understand.

Clear records don't just prove honesty. They also show that the trustee took the job seriously.

Handling cybersecurity and digital asset expenses

Trust administration now includes assets and risks that older trust documents never mentioned. According to this discussion of modern Texas trustee expense issues, digital asset trusts have seen a 15% year-over-year increase, and trustees now face cybersecurity and digital asset management costs that courts may treat as extraordinary expenses requiring beneficiary notice under Texas Trust Code §113.021.

That matters if the trust holds online financial accounts, cryptocurrency, digital business assets, or sensitive personal data. A trustee might need secure password management, multi-factor authentication tools, device hardening, or cyber insurance. These may be proper expenses, but they deserve extra care in documentation.

A cautious trustee should do three things before charging those costs:

- Explain the risk in writing

- Connect the expense to a specific trust asset or duty

- Give beneficiaries advance notice when the situation is unusual

That communication step often lowers conflict. People react better when they hear about a modern security expense before they see it listed on an accounting.

Frequently Asked Questions About Trustee Expenses

Can I reimburse myself for travel to check on trust property?

Usually, direct travel costs tied to trust business may be reimbursable if they were necessary and documented. Keep mileage logs, parking receipts, toll records, and a short note explaining why the trip was needed. If the trip mixed personal and trust purposes, only the trust-related portion should be charged.

Can I charge for my time and also reimburse my expenses?

Yes, those are different categories. You may be entitled to compensation for your work and reimbursement for out-of-pocket trust costs, but they should never be blended together in one unclear entry. Keep separate records so beneficiaries can see what was pay for services and what was repayment of expenses.

Do I need court approval for every expense?

No. Trustees generally administer trusts without asking a judge to approve routine decisions one by one. But if an expense is unusual, high-risk, disputed, or not clearly covered by the trust's ordinary administration needs, legal advice is wise before you act.

What if a beneficiary objects to my fee?

Don't get defensive and don't ignore the objection. Start by reviewing your records. Ask whether your fee method was clear, whether your entries explain the work performed, and whether you gave enough information in advance. Many disputes become manageable once the trustee provides a detailed accounting and a calm written explanation.

If the objection has merit, correct the issue early. If it doesn't, your records will matter more than your opinion.

Can I charge the trust for legal advice I get as trustee?

Often yes, if the legal advice was necessary for trust administration rather than for your purely personal protection. Advice about distributions, tax filings, property issues, or interpreting trustee powers is often part of proper administration. Keep the invoice and note what trust issue the attorney addressed.

Are major home renovations reimbursable, or only repairs?

Repairs are usually easier to justify because they preserve trust property. Major renovations require more caution. If the work was necessary to protect value, comply with law, or prepare the property for prudent sale or use, it may be proper. Get written bids, keep photos, preserve contractor agreements, and note why the decision benefited the trust.

Can I pay myself first and explain later?

That's risky. A trustee should be able to explain compensation before or at the time it's taken, not only after someone complains. A simple written fee policy, supported by time entries or another reasonable method, can prevent misunderstandings.

What if the trust document is silent about expenses?

Silence doesn't necessarily mean you're stuck paying proper trust expenses personally. Texas law recognizes reimbursement for expenses properly incurred in administering the trust. Still, the safest course is to review the trust terms carefully and make sure each charge clearly served the trust.

How often should I provide an accounting?

The trust terms and circumstances matter, but more transparency usually helps. Regular accountings reduce suspicion because beneficiaries don't have to guess what's happening. Even when no one is asking questions, periodic reporting shows that you understand your role as a fiduciary.

When should I talk to a lawyer?

Talk to a lawyer early if you're dealing with any of these situations:

- A blended family or tense beneficiary relationships

- Real estate, business interests, mineral rights, or hard-to-value assets

- You're both trustee and beneficiary

- You want to know how to modify a trust in Texas

- A beneficiary has made a written objection

- You're unsure whether a charge helps the trust or helps you personally

Trustees often wait too long because they think asking for help makes them look uncertain. In reality, timely advice often prevents the very disputes people fear.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including trust administration, estate planning, probate, guardianship, asset protection, and resolving questions about trustee expenses before they become costly disputes.