Skip to content

Skip to content A lot of Texas trustees never expected to be trustees at all. A parent dies, a family member becomes incapacitated, or a spouse leaves careful estate planning behind and names the person everyone trusts most. Suddenly, you're handling accounts, reading a trust document full of legal terms, answering beneficiary questions, and trying to make careful decisions with someone else's money.

That role can feel heavy fast. Most trustees worry about making a mistake, getting blamed by a beneficiary, or ending up in probate court. Those are real concerns. But there's another issue many new trustees don't see coming. In rare cases, trustee misconduct in Texas can become criminal, not just civil.

That doesn't mean every accounting error becomes a police matter. It doesn't. Most trust disputes still live in the world of civil remedies under the Texas Trust Code and related probate litigation under the Texas Estates Code. A trustee may be removed, ordered to repay money, required to account, or restricted by court order. Those are serious consequences, but they are different from criminal prosecution.

Still, criminal liability for trustees in Texas is rare but real. The danger usually appears when a trustee stops acting like a fiduciary and starts using trust property as if it were personal property, especially where the facts suggest intent, knowledge, or reckless disregard.

If you're serving as trustee now, the good news is that this risk is manageable when you understand the lines clearly. A careful trustee with good records, separate accounts, honest communication, and timely legal advice is in a very different position from a trustee who hides transactions, mixes funds, or “borrows” trust assets without authority.

An Unexpected Burden for Texas Trustees

A common story starts quietly. A daughter becomes trustee of her mother's living trust after her mother can no longer manage finances. The trust owns a house, an investment account, and a checking account used to pay bills. The daughter wants to do the right thing, but she's also juggling work, children, and the emotional strain of caregiving.

At first, the tasks seem practical. Pay the utilities. Renew insurance. Keep up with property taxes. Answer a sibling who wants updates. Then harder questions appear. Can she reimburse herself for time spent cleaning out the house? Can she move money between accounts? Can she sell an asset to a relative if the family agrees? Can she delay reports until things calm down?

Most trustees start with good intentions. That matters, but good intentions alone don't solve legal problems. Texas law treats a trustee as a fiduciary, which means the trustee must manage property for someone else's benefit, not for personal convenience or private gain. That's the baseline.

Practical rule: If you ever catch yourself thinking, “I'll just use this money for now and fix it later,” you're entering dangerous territory.

The reassuring part is that the legal system still recognizes the difference between confusion and dishonesty. Trustees often need guidance, not punishment. But the serious cases tend to follow familiar patterns. A trustee begins treating the trust like a family slush fund. Records get thin. Communication stops. Transfers happen without clear authority. By the time beneficiaries ask questions, the trustee may already be exposed.

That's why a new trustee should think like a manager and a recordkeeper from day one. A Texas trust administration lawyer can help you interpret the trust, understand your powers, and avoid decisions that create civil or criminal risk before they turn into a dispute.

The Foundation of Trust Law Understanding Fiduciary Duties

A trustee holds legal control, but not for personal use. Under the Texas Trust Code, that control exists for a limited purpose: to carry out the trust's terms for the beneficiaries' benefit. That basic separation matters because many criminal cases start with a trustee forgetting, or ignoring, that line.

The simplest way to view fiduciary duty is this. You are holding someone else's wallet, with written instructions attached. You may have broad authority to pay bills, sell assets, or invest funds, but the money is still not yours. The more a trustee treats trust property like personal property, the closer the conduct gets to the danger zone discussed later.

Loyalty comes first

The duty of loyalty is the anchor rule. A trustee must put the beneficiaries' interests and the trust's stated purpose ahead of personal convenience, family pressure, or side deals.

That rule answers many day-to-day questions. If the trust owns a rental house, leasing it to a friend at a discount is a problem unless the trust clearly permits it and the arrangement benefits the trust. Buying trust property for yourself raises an immediate self-dealing concern. Using trust funds to cover a personal bill is more than sloppy administration. It is the kind of act that can trigger questions about intent.

A good test is simple. Would this transaction still look proper if a beneficiary, a judge, and a forensic accountant reviewed it tomorrow?

Prudence is about process

Prudence does not require perfection. Trustees are not guarantors of results. Texas law expects reasonable care, skill, and caution in handling trust assets, which usually means using a sound process, staying within the trust's authority, and making decisions for trust purposes.

That distinction matters. A trustee can make a reasonable investment decision that turns out badly without becoming a wrongdoer. By contrast, a trustee who skips basic review, mixes funds, or acts for personal benefit creates a very different record.

Here is what prudent administration often looks like:

- Use separate accounts. Trust money belongs in trust accounts, not in a personal checking or savings account.

- Keep the paper trail. Save statements, invoices, appraisals, contracts, emails, and notes showing why you made a decision.

- Get qualified advice. A CPA, appraiser, financial advisor, or trust lawyer can help when the issue is outside your experience.

- Check your authority first. Before selling, distributing, borrowing, or reimbursing yourself, confirm that the trust document and Texas law allow it.

A careful trustee does not guess with other people's property.

Communication is part of fiduciary duty

Silence creates suspicion fast. Beneficiaries may assume the worst when questions go unanswered or records do not appear. Sometimes the underlying issue is only poor administration. Sometimes poor communication is the first visible sign of a more serious misuse of funds.

Texas trust disputes often grow from ordinary failures that could have been avoided with timely information and organized records. Clear communication also protects the trustee. If you can show what came in, what went out, why a decision was made, and where the authority came from, you are in a much safer position.

| Duty area | What it looks like in practice |

|---|---|

| Accounting | Keep organized records of income, expenses, distributions, transfers, and changes in asset value |

| Notice and information | Answer reasonable beneficiary requests and provide information the trustee is required to give |

| Administration | Follow the trust terms, respect limits on discretion, and act for the trust's stated purpose |

One final point matters for the criminal-risk analysis. Fiduciary duties are the baseline rules. Criminal exposure usually begins when a trustee does more than breach those rules by accident. Primary warning signs are a culpable mental state and a transaction involving fiduciary property that the trustee was not entitled to use in that way. Keep that framework in mind as you review any payment, transfer, sale, or reimbursement.

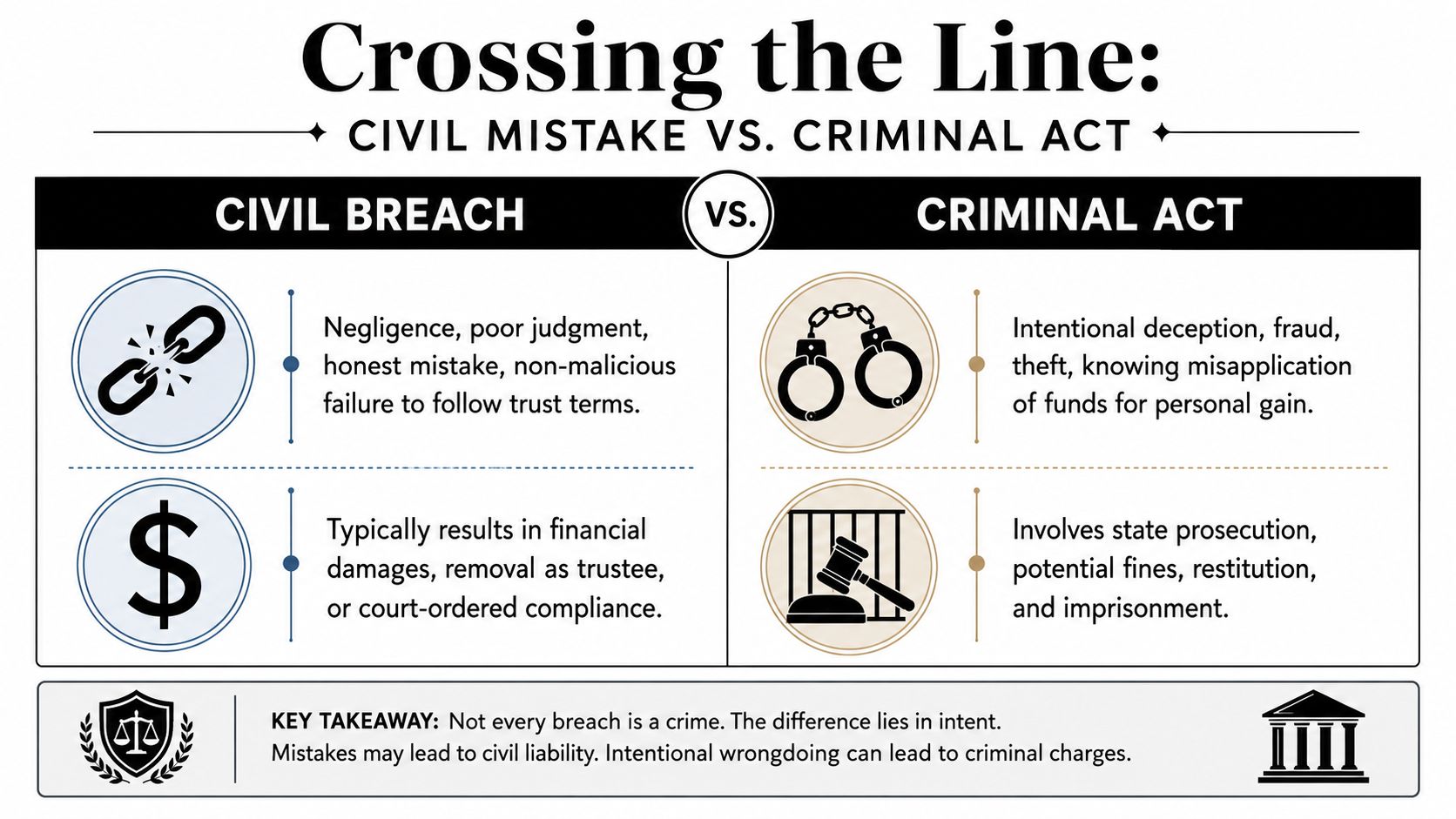

Crossing the Line From Civil Mistake to Criminal Act

The biggest point of confusion is this. A trustee can breach a duty without committing a crime. Texas law does not criminalize every bad decision, delay, or bookkeeping mess. The criminal line usually depends on mental state, sometimes called mens rea, and on whether the trustee misapplied fiduciary property.

Civil breach versus criminal conduct

Consider driving: an honest fender-bender and intentionally hitting a parked car are not the same event, even if both involve damage. Trust law works the same way. A trustee who misunderstands a reporting deadline may face civil consequences. A trustee who knowingly diverts trust money for personal use is in a different category.

The verified Texas standard is important. Misapplication of fiduciary property can create criminal exposure when the trustee acts “intentionally, knowingly, or recklessly” under Texas law, as discussed in this Texas criminal liability analysis for trustees and executors.

Here's the practical distinction:

| Situation | More likely civil | More likely criminal concern |

|---|---|---|

| Late report | Accounting delay, poor administration | Only if tied to concealment or falsified records |

| Bad investment | Negligence, imprudence | Only if done with improper purpose or knowing misuse |

| Using trust funds personally | Breach of loyalty at minimum | Strong risk if unauthorized and done intentionally, knowingly, or recklessly |

| Hidden transfer to yourself | Severe civil breach | Possible criminal investigation |

Why mental state matters so much

The state usually looks for evidence that shows more than sloppiness. Examples can include moving funds into a personal account, disguising a transfer on records, making unauthorized distributions to yourself, or telling beneficiaries false stories about where trust property went.

Recklessness can confuse people. It doesn't always require a signed confession or obvious theft language. A trustee can create serious trouble by consciously disregarding a substantial risk and moving forward anyway. In plain English, that's the trustee who knows the transfer is probably not authorized, knows the records are unclear, and does it anyway.

The age of the beneficiary can raise the stakes

Texas law also creates an elderly victim multiplier. If the offense is committed against someone 65 or older, the charge is upgraded to the next higher offense category, as explained in this discussion of criminal liability of trustees in Texas.

That means beneficiary age can materially change exposure. A trustee may focus only on the transaction itself, while prosecutors also focus on who was harmed.

For families dealing with an aging parent, a disabled settlor, or an elder beneficiary, that's a strong reason to get legal guidance early, keep authority in writing, and avoid any transaction that could look self-serving.

Common Criminal Offenses for Trustees in Texas

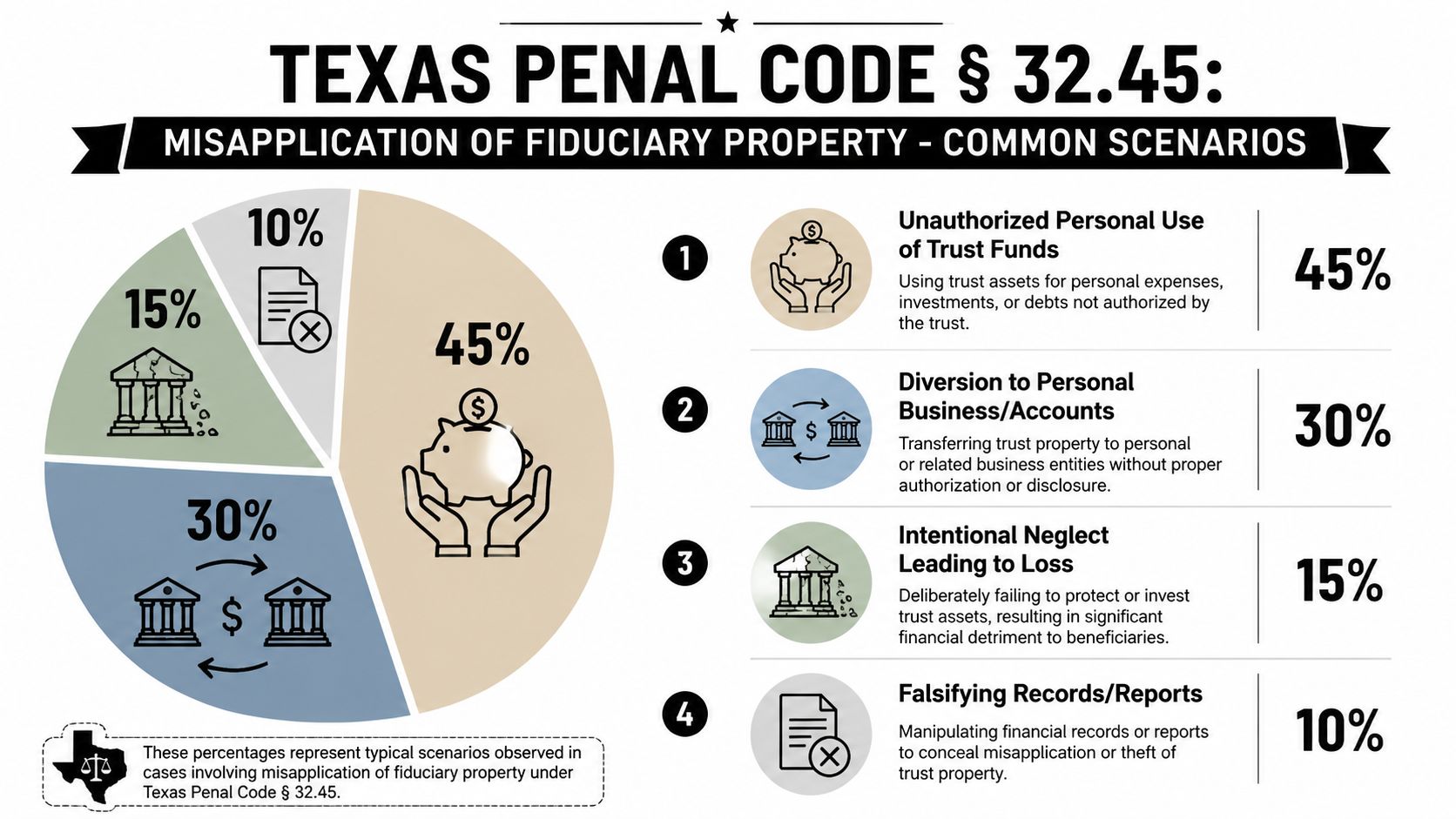

The main statute trustees need to know is Texas Penal Code § 32.45, often described as misapplication of fiduciary property. This is the statute that turns some trust misconduct from a civil breach into a criminal case.

The statute targets misuse of property held for others

A trustee holds property in a fiduciary capacity. That means the trustee is trusted to handle assets for someone else under legal duties. If the trustee misapplies that property with the required mental state, the issue may leave probate court and enter criminal court.

Texas treats this as a statute-based felony ladder, not just a routine breach claim. Under Texas Penal Code § 32.45, a trustee who “intentionally, knowingly, or recklessly” misapplies fiduciary property can face punishment that scales with value. Conduct involving less than $100 can be a Class C misdemeanor, while misapplied property worth $300,000 or more is a first-degree felony, and this framework has existed in Texas for over forty years, as summarized in this analysis of fiduciary property misapplication under Texas law.

That structure matters because trustees often underestimate how quickly exposure can escalate when multiple transactions are involved or a high-value asset is diverted.

Conduct that often creates risk

A trustee doesn't need to label a transaction “theft” for prosecutors to question it. Some of the most common danger areas are ordinary-looking transactions with hidden problems.

Examples include:

- Unauthorized personal use: Paying your own mortgage, taxes, legal fees, travel, or debts from trust funds.

- Improper transfers: Moving trust money into your own account or a related business without clear authority.

- False paperwork: Altering records, omitting transfers from reports, or creating misleading explanations.

- Self-dealing sales: Selling trust property to yourself or an insider on terms that don't protect the beneficiaries.

If you want a civil-law view of one of the most common warning signs, this discussion of trustee self-dealing in Texas is a useful companion issue. Self-dealing doesn't always become criminal, but it often provides the factual setting where criminal allegations begin.

Why trustees get tripped up by the word borrow

Many trustees use the word “borrow” casually. They mean they took money temporarily and intended to repay it. That description may feel softer inside a family. It usually does not soften the legal problem.

Danger zone checklist: If the trust document doesn't clearly authorize the transaction, the beneficiaries didn't validly consent, the money went to your benefit, and the books don't fully show what happened, assume you need legal advice before taking another step.

The trust isn't your line of credit. It isn't your emergency reserve. It isn't your business operating capital. Once a trustee starts using trust property that way, the analysis shifts away from administration and toward misuse of fiduciary property.

Red Flags and Real-World Scenarios

At 4:30 p.m. on a Friday, a trustee sees payroll due at her business, a trust account with available cash, and a plan to repay the money next week. That moment is where trustees get into real danger. The legal question is not whether repayment was planned. The question is what the trustee intended at the time of the transfer, whether the trust allowed it, and how much money was involved.

A good way to read these scenarios is to ask two separate questions. First, was this a bad fiduciary decision that creates civil exposure, such as trustee personal liability in Texas? Second, did the facts also suggest a criminal mental state, such as acting intentionally, knowingly, or at least recklessly with trust property? That second question is the danger zone.

Scenario 1. “I was only borrowing it”

A trustee moves trust money into a personal business account to cover a short-term cash shortage. There is no written authority in the trust. No informed beneficiary consent exists. The trustee expects to replace the funds after receivables arrive.

Trust law treats that move a lot like using a neighbor's stored property because you plan to return it later. The promised return does not erase the unauthorized use. For criminal risk, the facts that matter are the trustee's mental state and the amount involved. If the trustee knew the trust did not allow the transfer, or was aware of a substantial risk and did it anyway, the case starts to look less like poor administration and more like misapplication of fiduciary property.

Danger zone signals in this scenario:

- Money went to the trustee's own benefit

- No clear authority appears in the trust instrument

- No written consent came from all necessary parties

- The transfer was described casually as a “loan”

- The amount is high enough to draw serious attention from law enforcement

As the amount rises, the criminal exposure rises with it. That is one reason small “temporary” transfers can become very serious cases.

Scenario 2. The mixed account that ruins the explanation

A trustee deposits rent checks and trust income into a personal checking account “for convenience.” Later, the same account pays trust bills, groceries, and a credit card. The trustee may insist nothing was stolen. The records now tell a much messier story.

Commingling is like pouring two different liquids into one unlabeled bucket. After that, proving which dollar belonged to whom becomes difficult, and every withdrawal invites scrutiny. Commingling alone is not automatically a crime, but it often supplies the proof problems that make a prosecutor suspicious of intent, knowledge, or recklessness.

The red flag is not only the mixed account itself. It is what usually follows: missing support, after-the-fact explanations, and no clean way to show that trust funds stayed inside trust purposes.

Scenario 3. The family sale at a “friendly” price

A trust owns land. The trustee sells it to a cousin for less than market value because the family wants to keep the property close. No independent appraisal supports the price. The trustee does not fully explain the deal before it closes.

That fact pattern may begin as a loyalty problem, but criminal risk enters if the trustee hid material facts, arranged an indirect benefit, or manipulated documents to make the sale look ordinary. In other words, the mental state matters again. A bad judgment call is one thing. A sale structured to benefit an insider while disguising the harm to the trust is something else.

Scenario 4. Silence, delay, and money still moving

A trustee stops answering beneficiary questions, misses accountings, and keeps controlling distributions and transfers. By itself, poor communication is usually a civil problem. Combined with unauthorized withdrawals, false explanations, or altered records, it becomes much more serious.

Silence often matters because it is evidence. Honest trustees usually produce statements, invoices, and written reasons for decisions. Trustees who are hiding unauthorized conduct often stall for time.

A short checklist for spotting the criminal danger zone

If several of these are present at once, the risk is no longer just “trust administration went badly”:

- The trustee personally benefited from the transaction

- The trust document does not clearly authorize the act

- Beneficiary consent is missing, partial, or informal

- Records are incomplete, altered, or created after the dispute started

- The trustee's explanation changed over time

- Funds were moved through personal or business accounts

- The amount involved is large enough to raise the stakes significantly

- Basic safeguards were ignored, including the kind of separation and documentation reflected in church internal controls

One bad fact does not automatically create a criminal case. Several bad facts together, especially unauthorized personal benefit plus a culpable mental state plus a meaningful dollar amount, are what push a trustee into the danger zone.

A Trustee's Shield Best Practices to Avoid Criminal Risk

The best protection is boring, consistent administration. Trustees who follow systems are easier to defend than trustees who rely on memory, informal family understandings, or verbal side deals.

A practical framework comes from internal control thinking. Even outside the trust world, governance professionals stress basic segregation, documentation, and approval procedures. For a readable example of how organizations reduce misuse risk, see these church internal controls. The context is different, but the lesson carries over well. Good controls protect honest people.

Build your paper trail before trouble starts

Start with the trust document. Read it carefully. Then read it again with a lawyer if any provision is unclear. A trustee's authority comes from the instrument and Texas law, not from habit or family expectations.

Use systems that create proof:

- Separate accounts only: Every trust dollar should flow through trust-owned accounts.

- Written decision file: Keep notes, statements, invoices, contracts, emails, and approvals together.

- Distribution support: Match each distribution to trust language or a written legal basis.

- Fee records: If you pay yourself, document the authority and method used.

If you're concerned about exposure generally, this resource on trustee personal liability in Texas helps frame the broader civil side of the problem.

Slow down around self-interest

The highest-risk transactions usually share one feature. The trustee benefits, directly or indirectly. That doesn't automatically mean the action is forbidden, but it does mean you should pause.

Ask these questions before acting:

| Question | Why it matters |

|---|---|

| Does the trust expressly allow this? | Authority should be clear, not implied from convenience |

| Would every beneficiary understand and accept this if fully disclosed? | Transparency tests defensibility |

| Have I documented value and purpose? | Missing support makes even fair transactions look suspect |

| Have I asked legal and tax counsel first? | Advance advice is far better than damage control |

Here's a short video that gives additional context on trustee risk and fiduciary responsibilities:

Keep beneficiaries informed

Regular communication reduces conflict. It also shows you're acting like a fiduciary, not an owner. Even difficult news is better than silence.

Best practice: If a transaction would surprise a beneficiary, explain it in writing before it becomes a dispute.

That simple habit has prevented many trustee problems from becoming accusations.

Under Suspicion Steps to Take When Accused

Even careful trustees can get accused. Family conflict, unequal distributions, old grudges, and misunderstanding about trust terms can all trigger allegations. If the accusation includes fraud, theft, misapplication, or abuse of an elderly beneficiary, treat it as serious immediately.

What not to do

Your first instinct may be to explain everything at once. Don't. A rushed explanation can lock you into statements before your records are organized and before counsel understands the full picture.

Avoid these mistakes:

- Don't destroy or edit records: That includes texts, emails, spreadsheets, notes, and bank information.

- Don't call everyone involved: Conversations with beneficiaries, co-trustees, accountants, or investigators can complicate the case.

- Don't meet law enforcement alone: If investigators contact you, get counsel before answering questions.

What to do right away

Start preserving information. Pull the trust document, amendments, account statements, ledgers, tax returns, deeds, closing papers, emails, and written beneficiary communications into one secure place. Don't annotate them. Preserve them.

Then call an attorney with trust administration and fiduciary dispute experience. If criminal exposure is even possible, your legal team may also need to coordinate with criminal defense counsel. Timing matters here. Early legal intervention can shape how records are presented, how communications are handled, and whether a misunderstanding hardens into a formal allegation.

If you're unsure whether your situation has reached that point, this guide on when to hire a trust administration attorney in Texas is a good place to start.

Why silence can protect you

Silence is not an admission. It is often the smartest first step. Trustees sometimes damage their own position by trying to sound cooperative before anyone has reviewed the file carefully.

A lawyer's first job is usually practical. Secure records. Identify authority for each disputed act. Separate real problems from emotional accusations. Control communications. Decide what should be produced, when, and to whom.

That's not hiding. That's responsible legal protection in a high-risk fiduciary matter.

If you're managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including trust administration, probate, guardianship, asset protection, and fiduciary disputes. Whether you're a trustee trying to avoid costly mistakes, a beneficiary seeking answers, or a family needing a Texas trust administration lawyer or Texas estate planning attorney, our team can help you move forward with clarity and confidence.