You've worked hard to build your Texas real estate portfolio. Maybe it started with one rental house, then a duplex, then a small commercial property or a few LLC interests tied to different deals. Growth feels good, but it also creates pressure. If something happens to you, if a property needs fast decisions, or if title and ownership aren't lined up correctly, a solid portfolio can become messy very quickly.

That's why investors start asking a different kind of question. Not just how to buy the next property, but how to hold what they already own in a way that protects control, supports management, and makes succession easier. A trust can do that, but only if it's built for the realities of active investing.

Many investors think of a trust as a probate-avoidance document. That's only part of the story. For a real estate investor, a trust can also function as an ownership and management structure. It can define who has authority to sign, lease, refinance, sell, retain reserves, and step in when the primary decision-maker can't continue. Under the Texas Trust Code and related fiduciary rules, that authority must be clear, and the trustee's duties must be practical enough to match the assets being managed.

Texas law also matters at the execution level. The Texas Estates Code shapes the broader estate-planning framework around incapacity, death, and property transfer, while trust administration depends on fiduciary discipline, proper titling, and clean records. In plain English, the paperwork has to match the way the properties are owned and operated.

If you're searching for how to structure a trust for real estate investors Texas, the answer isn't one document or one template. It's a system. The right system gives you continuity, cleaner administration, and fewer surprises for your family, business partners, and beneficiaries.

An Introduction to Securing Your Real Estate Legacy

A real estate portfolio creates two things at once. It creates opportunity, and it creates moving parts. Rent has to be collected, repairs approved, taxes paid, insurance maintained, loan documents reviewed, and decisions made when a property underperforms or a tenant defaults.

For many Texas investors, the trouble starts when legal ownership and operational control drift apart. A property may be managed like a business asset, but titled like a personal asset. Or the investor may have a trust in place, but the trust reads like a basic family estate document and says very little about income property, reserves, leasing authority, or successor decision-making.

That's where trust structuring becomes useful. Not as abstract planning, but as a way to create order. A properly designed trust can identify who manages the portfolio, what powers they have, who benefits from the assets, and how decisions should be made under normal conditions and during a transition.

Why investors need more than a basic estate-planning document

A trust for an investor should answer practical questions:

- Acquisition authority Who can take title to newly purchased property, and in what name?

- Operations authority Who can sign leases, approve repairs, hire managers, and deal with title companies or lenders?

- Cash management rules Who decides whether rental income is distributed or held back for repairs, vacancies, or capital improvements?

- Succession protocol Who steps in if the original decision-maker becomes incapacitated or dies?

These are fiduciary questions as much as estate-planning questions. Under Texas fiduciary principles, a trustee has to act loyally, prudently, and according to the trust instrument. If the instrument is thin, vague, or copied from a general form, it may not give enough guidance for active real estate.

A trust works best when it reflects how the portfolio actually operates, not how a generic form assumes a family account should operate.

What usually works and what usually doesn't

A workable investor trust has clear powers, current records, and a defined process for property transfers and administration. It treats the portfolio as a managed asset base.

What usually doesn't work is a trust that's signed and forgotten. Investors often assume the document itself does the job. In practice, the trust has to be funded, updated, and administered in a way that matches each property's title history and ongoing management.

That's the difference between a trust that looks complete in a binder and one that protects a Texas portfolio.

Choosing the Right Trust Structure for Your Texas Properties

Every trust structure solves a different problem. Investors get into trouble when they choose a trust based on a slogan like “avoid probate” or “protect assets” without asking how the structure will function during purchase, ownership, refinancing, and succession.

A goal-based way to choose

A better starting point is your actual goal. Do you want flexibility and probate avoidance? Stronger separation from personal ownership? Privacy in title? Or are you trying to build a long-term succession vehicle for income property held across several entities?

Here's a practical comparison:

| Trust option | Best fit | Main advantage | Main trade-off |

|---|---|---|---|

| Revocable living trust | Investor who wants control and continuity | Flexible management and smoother succession planning | It may not deliver the same level of asset-separation goals an investor expects from a more restrictive structure |

| Irrevocable trust | Investor focused on stronger long-term asset structuring | Can create firmer separation between the grantor and the assets | Reduced flexibility and more need for careful drafting |

| Land trust | Investor focused on title privacy and transaction handling | Can be useful in ownership structuring and privacy planning | Must be handled carefully in Texas transactions and not treated like a one-size-fits-all liability solution |

Revocable living trusts for control and continuity

A revocable living trust often fits investors who still want day-to-day control. They may be buying and holding rental property, want a successor trustee ready to step in, and want to avoid leaving a tangle of probate and title issues behind.

This structure often works well when the investor is also coordinating a full estate plan with powers of attorney, a will, and beneficiary planning. It's especially useful when the trust instrument gives the trustee express authority to acquire, lease, encumber, sell, and reinvest in real estate, rather than holding assets passively.

Irrevocable trusts for stronger separation

An irrevocable trust is a different tool. It may make sense when the investor's objective is more than convenience. The trade-off is obvious. More separation usually means less direct personal control.

For some families, that trade-off is acceptable because the trust is meant to preserve a portfolio across generations rather than function as the grantor's personal operating account. But this only works when the client understands that an irrevocable trust isn't just a stronger version of a revocable one. It changes the relationship between the creator, the trustee, and the property.

Land trusts and the Texas transaction problem

Texas investors also hear about land trusts, often in discussions about privacy or assignment strategy. In these discussions, oversimplified online advice frequently causes problems. Texas guidance highlights an important distinction between a trust used as an estate-planning wrapper and a trust used as an investor ownership or transaction tool. It also notes that the transaction structure matters. For example, an investor-buyer's LLC may sign the contract, the trust should be separately executed, and the closing should be treated as its own transaction rather than collapsed into a later beneficial-interest assignment, as discussed in Texas land trust guidance for investor transactions.

That nuance matters because title companies, lenders, and liability planning don't always respond well to improvised structures.

Practical rule: If your trust choice depends on how a closing will actually be handled, review the structure before you sign the contract, not after title work starts.

If you're evaluating whether a land trust fits a purchase or holding plan, it helps to review the issues with a Texas land trust attorney.

The Critical Steps to Funding Your Real Estate Trust

A trust doesn't protect real estate just because you signed it. Until property is transferred into the trust, the trust is mostly a set of instructions waiting for assets.

The practical sequence is well established. Guidance on Texas trusts explains that the process is to define the property set and investment objective, choose the trustee and successor trustee, draft the trust instrument with management and distribution powers, execute it properly, and then fund it by recording a deed that transfers each parcel into the trust. That same guidance warns that the major risk point is funding discipline, especially when later purchases aren't retitled into the trust. See the discussion in this Texas trust formation overview.

Start with the operating objective

Before drafting, decide what the trust is meant to do. Some investors want continuity if they become incapacitated. Others want a central holding structure for multiple properties. Others want the trust to hold LLC interests rather than direct title to every parcel.

That choice affects drafting. A trust that holds active rentals should authorize the trustee to acquire, lease, encumber, sell, and reinvest real estate. It should also address property records, accounting, and authority for operational decisions.

This visual breaks down the funding process in a practical order.

Funding means deeds, title review, and repeatable process

For Texas real estate, funding usually means preparing and recording a deed for each property that is being transferred into the trust. In a multi-property portfolio, each parcel has its own title path, and each one needs to be handled correctly.

A simple example helps. If an investor owns three rentals personally and signs a new trust agreement, nothing changes in the county land records until those three properties are deeded into the trust. If the investor buys a fourth rental later but forgets to vest title in the trustee, that property may sit outside the structure entirely.

That's why investor trusts need a mandatory acquisition protocol. New closings should include vesting instructions. Refinances should trigger a trust review. Title documents should be checked every time.

For investors who want a deeper look at deed transfer mechanics, this guide on how to transfer property to a trust is a useful starting point.

Build a funding checklist that survives real life

Most trust failures are not dramatic legal failures. They're administrative failures. The investor buys quickly, refinances under pressure, or changes entities and never updates title to match.

A practical checklist should include:

- Closing instructions Direct the title company on exactly how title should vest.

- Recorded deed review Confirm the filed deed matches the intended trust ownership.

- Property schedule updates Add each new asset to the trust's internal records.

- Refinance review Check whether the lender or title company requires temporary or permanent changes.

- Accounting alignment Make sure rent, expenses, and reserves are tracked to the proper owner.

Investors who utilize borrowed funds or partner capital also need transaction discipline outside the trust itself. If your acquisitions involve private capital, joint ventures, or creative financing, it helps to understand broader strategies for OPM real estate so your deal structure and trust structure don't conflict.

A short video can also help make the transfer process easier to visualize.

Selecting a Trustee and Understanding Fiduciary Duties in Texas

The trustee is where legal design becomes real-world performance. A strong trust with the wrong trustee can produce delay, conflict, poor recordkeeping, and bad decisions on repairs, leasing, or beneficiary distributions.

Guidance on trust setup consistently stresses one point. A trust needs a trustee who can administer property, plus a dependable backup. It also notes that many trusts fail in practice because owners don't keep up active administration after signing the documents, as described in this overview of how to set up a trust and maintain it properly.

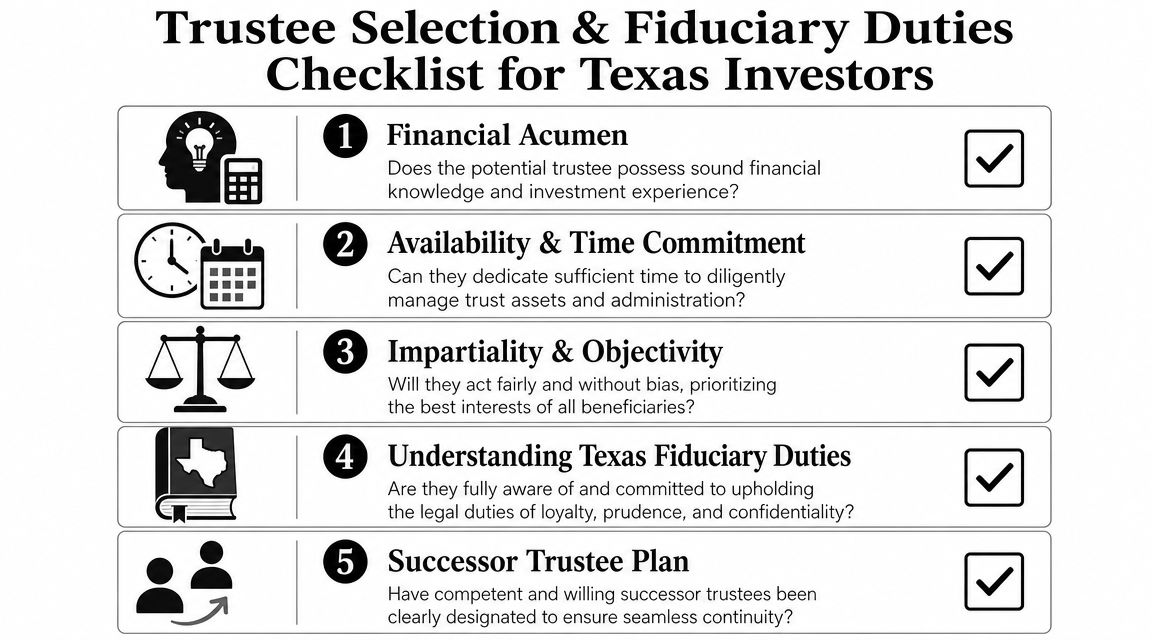

Who should serve as trustee

For a real estate investor, the trustee needs more than honesty. They need judgment. They may have to respond to tenant issues, approve a roof replacement, decide whether to keep reserves, communicate with beneficiaries, and coordinate with accountants, managers, or attorneys.

A family member can work if that person is organized, financially capable, and able to stay neutral. A professional fiduciary or corporate trustee may be better when the portfolio is larger, beneficiary interests are likely to conflict, or the assets require consistent administrative discipline.

A successor trustee matters just as much. If the named backup can't handle active real estate, the transition can become the very crisis the trust was meant to prevent.

Fiduciary duties in Texas in plain English

Under the Texas Trust Code, a trustee is a fiduciary. That means the trustee must act in the interests of the trust and its beneficiaries, not personal convenience.

The core duties usually include:

- Duty of loyalty The trustee must avoid self-dealing and put trust interests first.

- Duty of prudence The trustee must make careful, informed decisions about management, expenses, and risk.

- Duty of impartiality If there are multiple beneficiaries, the trustee must treat them fairly according to the trust terms.

- Duty to account and communicate The trustee should maintain records and provide appropriate information as required by the trust and Texas law.

A rental-house example makes this clearer. Suppose the trust owns income property and one beneficiary wants more cash distributions while another wants the trustee to retain earnings for repairs. The trustee can't favor the loudest person. The trustee has to follow the trust instrument, keep records, and make a prudent decision for the asset and all beneficiaries.

A trustee for real estate isn't just a signer on paper. That person is running a fiduciary system with legal duties attached to every major property decision.

For investors looking for a Texas trust administration lawyer or advice about fiduciary duties in Texas, trustee selection is often the most important conversation in the entire planning process.

Advanced Strategies for Investor Trusts and Asset Protection

A Texas investor buys a new rental in an LLC, leaves an older duplex in a revocable trust, and collects rent in a personal account because the bank setup is still pending. Six months later, a refinance, an insurance claim, and a beneficiary dispute expose the problem. The documents do not match the way the portfolio is being run.

That is the point where structure stops being theory.

Trust ownership versus trust governance

Investor trusts work best when ownership, control, and day-to-day operations are assigned on purpose. In some portfolios, the trust holds title directly. In others, the trust holds the membership interests of an LLC, and the LLC owns the property. That second approach often fits active investors better because leases, vendors, bank accounts, and property-level liability stay at the entity level while succession and beneficiary rights stay in the trust.

The trade-off is administrative discipline. More layers can mean better separation, but they also mean more documents, more title review, and more chances for a closing team or lender to ask questions. Texas investors should use extra structure only when it solves a defined problem, such as multi-property management, blended families, staggered inheritance, or a need for continuity if the primary decision-maker becomes unavailable.

The real issue is cash flow control

The operational side is where many trust plans fail. A trust that owns investment property needs written rules for rent collection, reserve retention, capital repairs, and distributions. If the document only addresses death and succession, the trustee is left making business judgments without much direction.

That creates friction fast.

A vacancy, roof replacement, delinquent taxes, or rising insurance premiums can force a choice between preserving the asset and making beneficiary distributions. Good drafting gives the trustee a framework before that pressure arrives.

A well-built investor trust should answer questions such as:

- Who receives rent first. Does income go into a trust account, an LLC operating account, or another designated account tied to the ownership structure?

- How reserves are handled. Can the trustee hold back cash for repairs, taxes, insurance, and vacancy periods without getting beneficiary approval each time?

- Who approves major projects. Is the trustee free to replace HVAC systems, roofs, or plumbing lines, or is beneficiary consent required above a stated dollar amount?

- How distributions are calculated. Are beneficiaries entitled to current cash flow, or only net cash flow after debt service, reserves, and known expenses?

- How records are kept. If the portfolio has multiple houses or commercial units, can the trustee show property-by-property performance and justify decisions clearly?

A trust that holds income property should direct the trustee how to run it, not merely identify who benefits from it.

Liability structuring requires more than a trust

A trust can help with succession, management authority, and beneficiary protection. It is not a substitute for liability segregation. If one property creates a serious claim, the ownership chain matters. So do insurance limits, entity boundaries, indemnity language in leases, and whether funds were kept separate in practice.

Texas investors often try to make one structure do four jobs at once. They want probate avoidance, privacy, liability protection, financing flexibility, and easy operations from a single document. That is usually where the plan starts to break down. A trust may be the right place to hold LLC interests. The LLC may be the right place to operate the property. Insurance still covers a different category of risk.

If you are considering a more protective structure, this discussion of Texas asset protection trusts and how they work is a useful starting point. The right answer depends on the asset mix, debt, family dynamics, and how actively the portfolio is managed.

Acquisition and closing protocols matter

Experienced investors know the risk is not just in the document set. It is in the closing instructions.

Before a purchase, the investor should know exactly who is signing the contract, who will take title, whether the earnest money source matches the buyer entity, and where post-closing rent will be deposited. Those details affect title commitments, lender underwriting, insurance issuance, and later resale. In Texas, a structure that makes sense on paper can still create closing friction if the title company sees inconsistent vesting or incomplete authority documents.

For active portfolios, I usually want an acquisition protocol that answers four practical questions before the contract is signed: whose name goes on the offer, whose tax reporting applies, which account handles receipts and expenses, and whether the trust or LLC documents give clear authority for the transaction. Investors who skip that step often spend more time fixing avoidable title and bookkeeping issues later.

Where coordinated legal work fits

Coordination matters here. A Texas estate planning attorney, real estate counsel, CPA, lender, and title professionals may all need to align before the structure works the way the investor expects. For instance, the Law Office of Bryan Fagan, PLLC handles trust creation, administration, and related asset-protection planning in Texas, which can help when one legal plan needs to cover succession, fiduciary authority, and portfolio administration together.

Common Pitfalls and When to Consult a Texas Trust Attorney

Most trust problems aren't caused by exotic legal doctrine. They come from ordinary mistakes made at ordinary times. An investor is busy, a closing moves fast, a refinance changes title assumptions, or a family member gets named trustee without understanding the job.

The mistakes that cost investors the most

Some problems show up again and again:

- Using the wrong structure A revocable trust, irrevocable trust, land trust, and LLC each solve different problems. Trouble starts when an investor chooses one for privacy, liability, probate avoidance, and transaction flexibility all at once.

- Ignoring administration A trust that isn't actively maintained becomes unreliable when a crisis hits.

- Naming the wrong trustee A person may be trustworthy but still not capable of managing active rental property under fiduciary standards.

- Leaving operational gaps If the trust says nothing about reserves, repairs, or leasing authority, conflict often follows.

- Treating title issues as clerical In real estate, title is substance. If ownership records don't match the plan, the plan may fail when it matters most.

When legal review is worth it

You should strongly consider legal review before any of these events:

| Situation | Why review matters |

|---|---|

| Buying a new property | Title should vest correctly from the start |

| Refinancing | Loan and title requirements can affect trust ownership |

| Adding family beneficiaries | Distribution and control issues become more sensitive |

| Moving properties into LLCs | The trust and entity plan need to match |

| Preparing for incapacity or succession | Successor authority should be clear before an emergency |

A good planning meeting isn't just about drafting. It's about pressure-testing the trust against the way you invest. That includes the Texas Trust Code, the Texas Estates Code, deed practice, fiduciary obligations, and the administrative reality of managing real property over time.

If you're looking up how to modify a trust in Texas, or trying to decide whether your current setup still fits your portfolio, that's often a sign the structure needs professional review rather than another online template.

The right legal advice can also reduce disputes before they start. Clear trustee powers, clean accounting standards, beneficiary communication rules, and a consistent acquisition protocol tend to make trust administration calmer for everyone involved.

If you're managing a trust, building a real estate portfolio, or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance on estate planning, probate, guardianship, asset protection, and trust administration so you can protect your properties, your family, and your long-term goals with clarity.