A lot of Texas families reach this point the same way. A parent wants to avoid probate, protect a child's inheritance, or make things easier if illness strikes. Then the terms start piling up. Revocable. Irrevocable. Grantor. Non-grantor. Taxable entity. Form 1041.

That's when planning can start to feel heavier than it should.

The good news is that this choice becomes much easier once you focus on the practical question behind the legal labels. Do you want to keep control and simplicity during your lifetime, or do you want stronger separation for tax and long-term transfer planning? If you're trying to build your family legacy, that's usually the core decision.

Planning Your Legacy in Texas Can Feel Overwhelming

A Houston couple in their sixties may own a home, brokerage accounts, a family business interest, and life insurance. They want to protect each other, avoid unnecessary court involvement, and leave clear instructions for their children. Then they hear two lawyers use similar trust language in very different ways. One mentions a grantor trust. Another discusses a non-grantor trust. Both sound important. Neither sounds simple.

That confusion is normal.

In Texas, trust planning often sits at the intersection of the Texas Trust Code, the Texas Estates Code, and federal tax rules. Texas law governs how trusts are created, administered, modified, and enforced. Fiduciary principles also matter. Trustees owe duties of loyalty, prudence, and proper administration to the beneficiaries they serve. But the grantor versus non-grantor distinction turns mostly on federal income tax treatment and the level of control the person creating the trust keeps.

Why families get stuck on this choice

Individuals aren't really asking for a technical label. They're asking questions like these:

- Can I still change the trust later?

- Who pays the income tax?

- Will the assets still be part of my estate?

- Will this help protect assets for my children?

- How much work will the trustee have to do?

Those are the right questions. A calm planning process starts there, not with jargon.

Many trust decisions aren't about choosing a “better” trust. They're about choosing the trust that matches your family's actual goals.

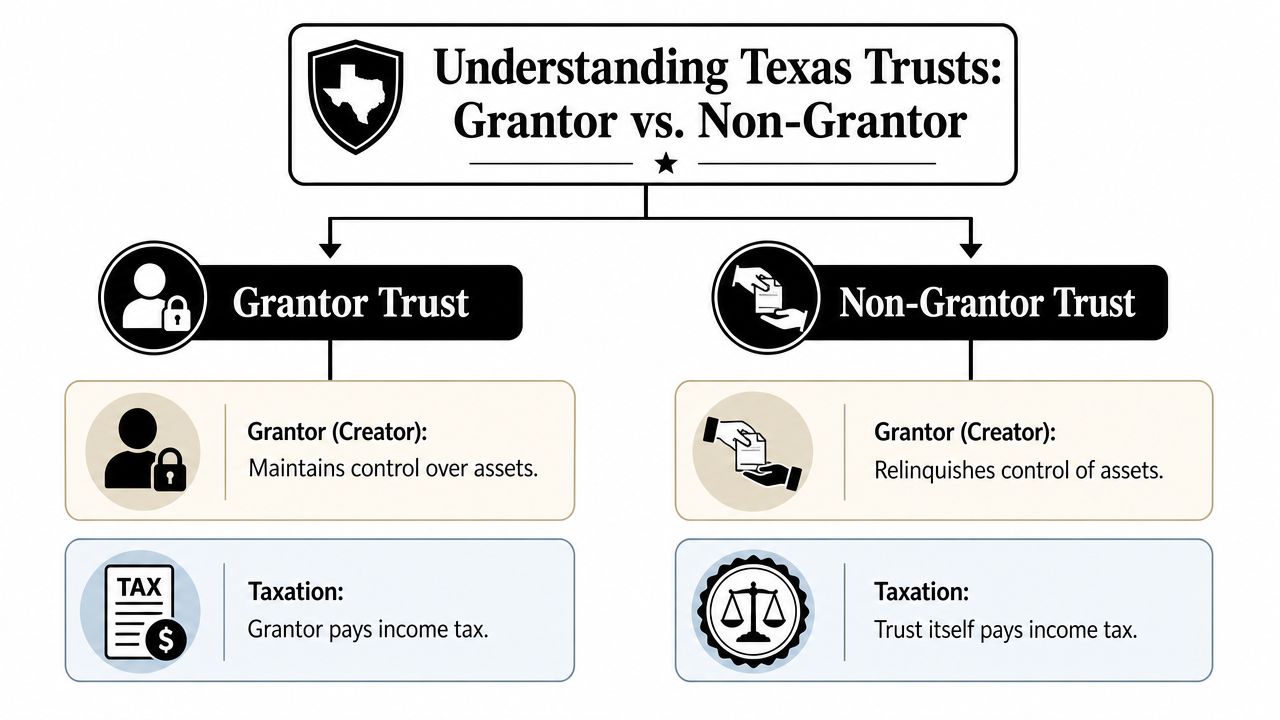

The Core Distinction Grantor and Non-Grantor Trusts

The simplest way to understand this is to think about who still owns the tax burden and who still holds the steering wheel.

A grantor trust is a trust where the person who created it kept enough control or retained certain powers so that, for federal income tax purposes, the IRS still treats the trust income as that person's income. A non-grantor trust is different. It's generally treated as its own taxable entity and usually files its own fiduciary income tax return on Form 1041, as explained in this discussion of what a grantor trust is in Texas and in the underlying federal tax distinction described by Triangle Estate Lawyers.

A simple analogy that helps

Think of a grantor trust like a separate folder holding your assets, but one the tax law still treats as closely tied to you. The folder helps organize ownership and planning, but the income tax still lands on your return.

A non-grantor trust is more like a separate legal bucket with its own tax identity. The trust can hold property for beneficiaries, and the tax system generally treats it as a separate taxpayer.

That difference matters because many families assume all trusts work the same once the paperwork is signed. They don't.

Texas law versus federal tax law

Here's where readers often get mixed up. Under Texas law, a trust can be validly created and administered under familiar estate planning principles. The Texas Trust Code governs trustee powers, fiduciary duties in Texas, accounting, beneficiary rights, and court involvement when disputes arise. The Texas Estates Code often becomes relevant when a trust works alongside a will, probate administration, incapacity planning, or guardianship-related concerns.

But whether a trust is grantor or non-grantor is not mainly a Texas label. It's a federal tax classification tied to retained powers and control.

The practical dividing line

If the person creating the trust keeps meaningful powers, such as the ability to revoke, amend, direct certain enjoyment rights, or otherwise preserve tax ownership, that often points toward grantor trust treatment. If those powers are given up, the trust is more likely to be treated separately for tax purposes.

Practical rule: If you keep control, you often keep the tax burden. If you give up enough control, the trust is more likely to become its own taxpayer.

That's why a grantor trust often fits families who want lifetime flexibility, while a non-grantor trust often fits families trying to create stronger separation between themselves and the trust assets.

Detailed Comparison Taxation Control and Asset Protection

The actual decision isn't just “What is this called?” It's “What changes for my family if we choose one structure over the other?” That's where side-by-side comparison helps.

Grantor Trust vs. Non-Grantor Trust at a Glance

| Feature | Grantor Trust | Non-Grantor Trust |

|---|---|---|

| Income tax treatment | Income is generally taxed to the grantor on the grantor's personal return | Trust is generally a separate taxpayer and typically files Form 1041 |

| Federal trust tax brackets | Doesn't use separate trust-level brackets in the same way because income is taxed to the grantor | Can reach the top federal income-tax rate quickly |

| Control | Grantor usually keeps meaningful powers or flexibility | Grantor generally gives up more control |

| Estate inclusion risk | Assets are often included in the grantor's estate | Assets are more likely to be excluded from the grantor's estate |

| Best fit | Lifetime flexibility and easy adjustment | Estate-tax goals and stronger separation |

| Administration | Often simpler from an income tax reporting standpoint | Often requires separate trust tax reporting and closer ongoing administration |

Taxation and why it matters so much

For many Texas families, this is the most important section.

For 2025, the top 37% federal income-tax rate for non-grantor trusts begins once taxable income exceeds $15,650, according to CLA's discussion of trust income tax implications. That same source notes that the 20% long-term capital-gains rate begins once trust taxable income exceeds $15,450 using 2024 figures, and that from 2025 through 2029, non-grantor trusts may deduct up to $40,000 of state and local income taxes under the SALT cap framework.

That compressed bracket structure is a major reason this choice matters. A trust doesn't need huge retained income to reach high tax rates.

A non-grantor trust can hit top federal tax rates much faster than an individual taxpayer. That doesn't make it bad planning. It means the tax cost has to be weighed against the estate and control benefits.

If a trust will hold rental property, marketable investments, or business interests that produce income, tax design matters from day one. Readers who want a deeper tax overview can review this page on trust taxation in Texas.

If your estate plan includes real property, it also helps to explore real estate trust benefits in a separate context, because ownership structure and tax treatment often overlap in practical planning.

Control and flexibility during life

A grantor trust usually appeals to people who want room to adapt. If your family situation changes, if a child develops special needs, if your asset mix changes, or if you want the ability to revise terms, grantor trust treatment often aligns with that mindset.

A non-grantor trust usually asks for a different posture. To get the separation benefits, the grantor often has to surrender enough control to let the trust stand apart.

That can feel uncomfortable. It also can be exactly what some families need.

Estate planning and asset separation

When the grantor retains powers, the trust assets are often more likely to remain tied to the grantor's taxable estate. When those powers are removed, the assets are more likely to stand outside the grantor's estate.

That tradeoff is often the heart of advanced estate planning. You're balancing flexibility today against separation tomorrow.

Asset protection and fiduciary administration

Families also ask whether one structure automatically gives “asset protection.” That question needs careful handling. Asset protection doesn't come from a label alone. It depends on drafting, funding, trustee conduct, distribution standards, and compliance with fiduciary duties in Texas.

A trustee has to administer the trust according to its terms, keep records, communicate appropriately with beneficiaries, and avoid self-dealing. Those duties matter under the Texas Trust Code whether the trust is grantor or non-grantor. A structure that looks strong on paper can fail in practice if the trustee treats trust property like personal property.

Common Use Cases When to Choose Each Trust in Texas

The easiest way to understand the strategic tradeoffs is to look at the kind of family each trust tends to help.

A family that wants flexibility

Consider a married couple in The Woodlands with adult children, retirement accounts, a brokerage account, and a homestead. They want a plan that allows easy management if one spouse becomes incapacitated. They also want to update terms later if family needs change.

A revocable trust often fits that goal, and IRS guidance confirms that revocable trusts are always grantor trusts, as discussed in the IRS guidance on abusive trust tax evasion questions and answers. That doesn't mean the trust is abusive. It means the IRS treats the income as belonging to the grantor for income tax purposes because the grantor kept the power to revoke.

For this couple, paying tax personally may help. It keeps reporting more straightforward and preserves lifetime control. If one child later needs added protections, the plan can often be revised.

A family focused on estate separation

Now take a different situation. A business owner in Dallas wants to move selected assets out of the estate and create stronger separation for future beneficiaries. That person is less concerned with changing the trust later and more concerned with long-term transfer planning and asset protection structure.

That scenario may point toward a non-grantor trust, especially when reducing estate inclusion and shifting tax responsibility away from the grantor are key goals.

The tradeoff is clear. The grantor gives up more control, and the trust often takes on its own filing and tax burden.

After you've seen the family examples, this short overview may help reinforce how these planning choices work in practice.

Where Texas families often land

Many families don't need an extreme answer. They need a trust design that matches a narrow purpose.

A few common patterns look like this:

- Lifetime management need: A grantor trust often makes sense when the family wants continuity, incapacity planning, and the ability to revise terms.

- Long-range transfer objective: A non-grantor trust often makes sense when the goal is to create meaningful distance between the grantor and the assets.

- Mixed planning goals: Some families use more than one trust strategy for different assets or different family concerns.

For these reasons, a Texas estate planning attorney becomes useful. The legal documents have to work with the family's tax goals, beneficiary needs, and trustee capabilities. The same is true for asset protection planning. The label only helps if the trust is drafted and administered in a way that supports the intended result.

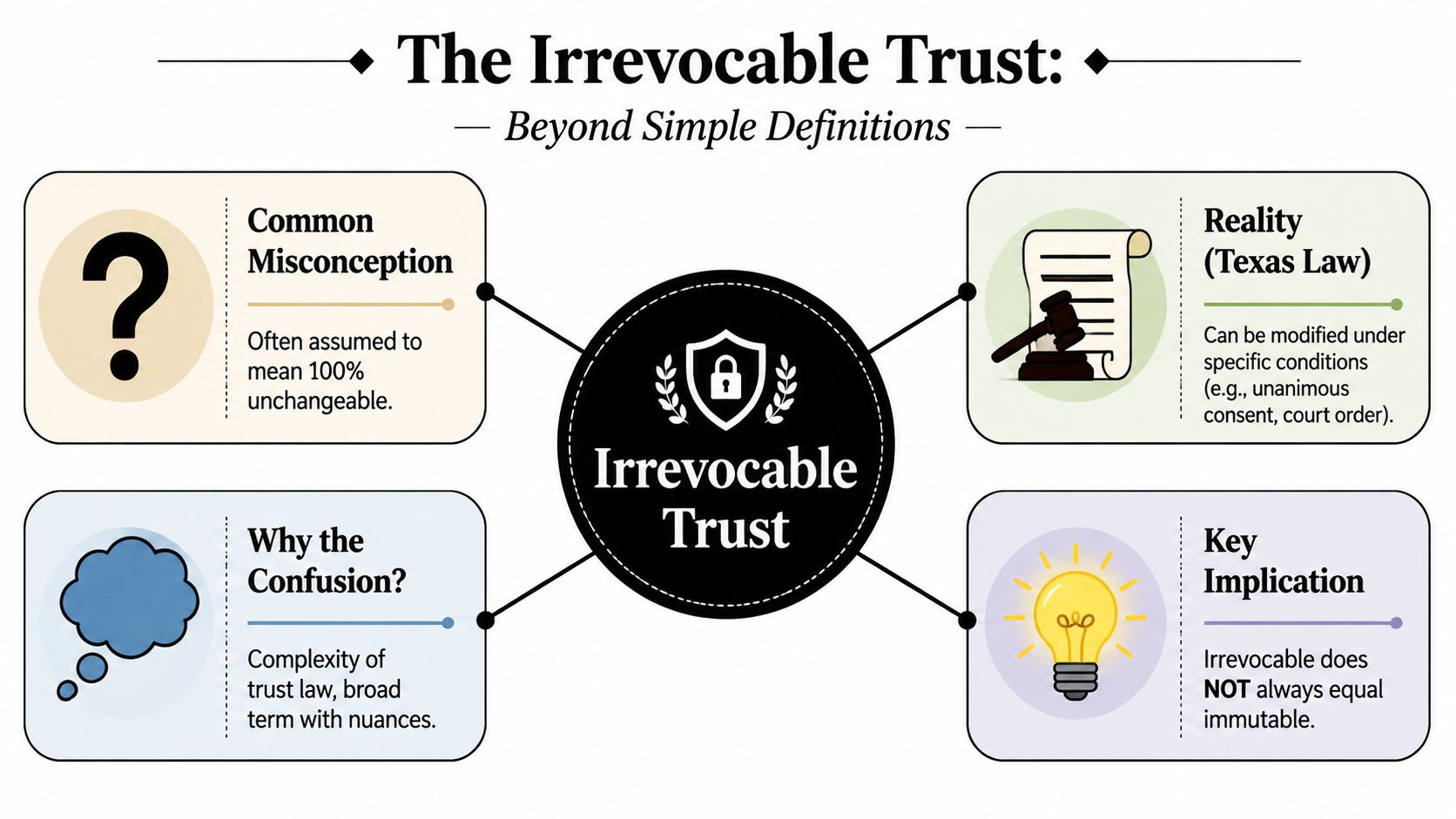

The Irrevocable Trust Dilemma A Common Point of Confusion

One of the biggest misunderstandings in trust planning is this: people hear the word irrevocable and assume it automatically means non-grantor.

It doesn't.

Why the label creates confusion

Under Texas law, an irrevocable trust generally means the grantor can't revoke or rewrite it at will. That's a state-law concept.

For federal income tax purposes, the question is different. The tax law asks whether the grantor kept certain powers or interests that cause the trust to be treated as a grantor trust anyway.

As described in this discussion of irrevocable trusts in Texas and in the tax analysis summarized by Koley Jessen, grantor status can arise from retained powers over revocation, beneficial enjoyment, investments, or substitution powers, even when the trust is irrevocable.

What that means in plain language

A trust can be:

- Irrevocable under Texas law, and

- Still a grantor trust for federal income tax purposes

That's not a drafting mistake by default. Sometimes lawyers structure a trust that way on purpose because the family wants estate planning benefits but also wants the grantor to keep paying the income tax.

Irrevocable describes whether the trust can be freely undone under state law. Grantor describes who the tax law treats as the income owner.

Those are separate questions.

Why careful drafting matters

Effective technical drafting becomes critical for any Texas trust administration lawyer or planning attorney. Small powers in the document can change tax treatment in a major way. If the draft accidentally gives the grantor too much retained influence, the trust may not produce the intended non-grantor result.

This also matters later in administration. Trustees need to know what powers exist, how distributions work, and whether trust actions could affect reporting obligations. Beneficiaries often assume the trustee can “just fix it later,” but trust modifications, court approval, consent arrangements, and tax consequences aren't casual decisions under the Texas Trust Code.

For families, the practical lesson is simple. Don't rely on the word irrevocable as a full answer. Ask what powers remain, who pays the tax, and how the trust is meant to function in real life.

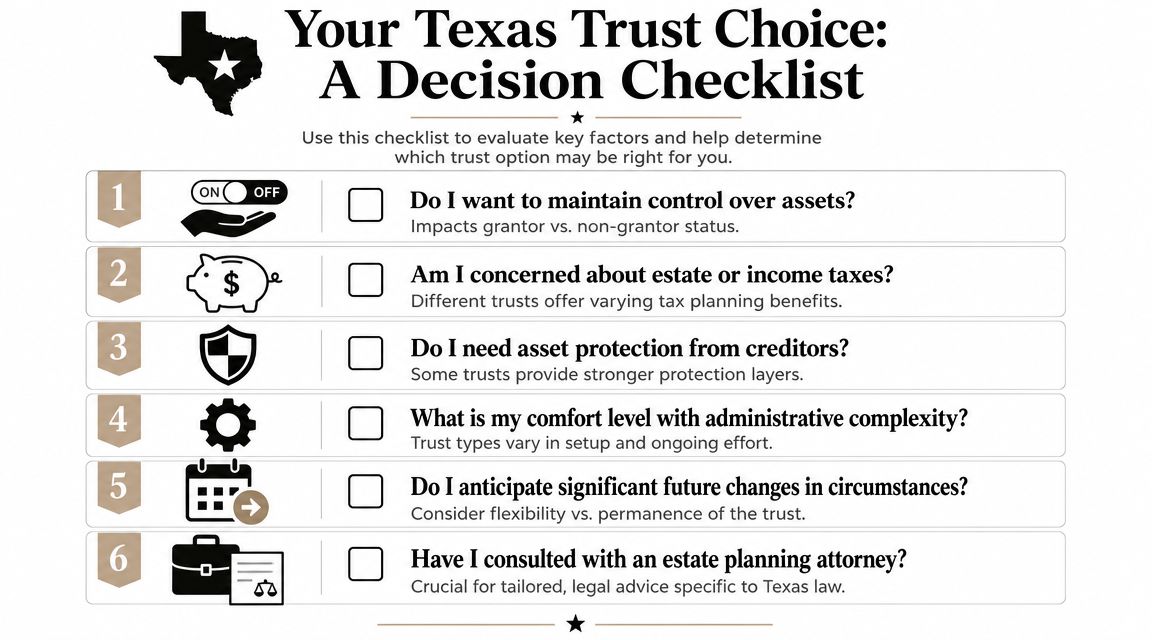

A Checklist for Choosing Your Trust Structure

Most families make this decision better when they stop asking, “Which trust is more advanced?” and start asking, “Which trust fits the job I need done?”

Questions worth answering before you sign anything

Do I want to maintain control over assets?

If keeping the ability to adjust terms, direct outcomes, or preserve flexibility matters most, a grantor-oriented structure may be the better fit.Am I more concerned about estate planning or current income tax treatment?

Some families are comfortable paying tax personally if that supports flexibility. Others care more about creating separation from the estate.Do I want assets moved out of my estate for long-term planning?

If permanent transfer and separation are the priority, a non-grantor design may align better.How much administrative work am I comfortable creating for the trustee?

Separate tax reporting, fiduciary accounting, beneficiary communication, and ongoing administration all matter in trust planning.Do I expect my family circumstances to change?

A child's maturity, remarriage, disability concerns, business succession, or blended family dynamics may make flexibility more valuable than strict separation.Who will serve as trustee, and are they prepared?

A trustee must follow fiduciary duties in Texas, keep records, act prudently, and communicate appropriately with beneficiaries. A well-meaning relative isn't always the right choice.

A helpful way to use this checklist

Bring your answers to a planning meeting. Don't worry about sounding technical. A good consultation is often more productive when the family can clearly say:

- what they want to protect,

- who they want to benefit,

- how much control they want to keep, and

- whether simplicity or separation matters more.

If you're also comparing probate avoidance, guardianship planning, or how to modify a trust in Texas, those questions should be part of the same conversation because the trust choice affects the larger estate plan.

How a Texas Estate Planning Attorney Can Help

This decision looks simple on the surface and highly technical underneath. That's why online definitions only go so far.

Often, the legal question is whether the grantor kept powers that matter under Internal Revenue Code rules 673 through 677. If those powers exist, the trust is usually a grantor trust and the assets are often included in the grantor's estate. If they don't, the trust is generally a non-grantor trust and the assets are more likely to be excluded, as summarized by Pendleton Square Trust's discussion of grantor and non-grantor trusts.

That's not just a tax question. It affects the entire planning structure.

A lawyer helps coordinate the trust terms with the Texas Trust Code, the Texas Estates Code, fiduciary duties in Texas, probate planning, beneficiary protections, and future administration. A Texas trust administration lawyer can also help trustees understand recordkeeping, beneficiary communication, tax filing responsibilities, and when court guidance may be needed. If the broader plan also involves probate, guardianship, or asset protection, those issues should be aligned rather than handled in isolation.

One option Texas families consider for this kind of work is Law Office of Bryan Fagan, PLLC, which handles estate planning, trust administration, probate, guardianship, and related asset protection matters in Texas.

If you're managing a trust or planning your estate, contact The Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.