Skip to content

Skip to content Managing a loved one’s trust can feel overwhelming, especially if you’ve just been told, “You’re the trustee now.” One day you’re helping with family paperwork. The next, you’re responsible for money, records, and decisions that affect other people.

Most new trustees in Texas worry about the same things. What do I have to track? Do I need to send yearly reports? What happens if a beneficiary asks questions I can’t answer right away? Those are fair concerns. Trust administration has legal rules, but it also has a practical side. Good habits matter just as much as knowing the statute.

A lot of confusion around annual trust accounting texas comes from one mistaken assumption. Many people believe Texas trustees must automatically send a formal accounting every year. Texas law is more nuanced than that. Still, a smart trustee often chooses annual reporting anyway, not because panic is necessary, but because prevention works better than cleanup.

Navigating Your Role as a Trustee in Texas

A common Texas scenario looks like this. A parent names an adult child as trustee of a family trust. The parent dies or becomes incapacitated. The new trustee finds a binder with the trust agreement, a few bank statements, maybe a deed, and a long list of responsibilities nobody fully explained.

That trustee usually isn’t trying to do anything wrong. They’re trying to be careful. But careful intentions alone won’t answer beneficiary questions, organize receipts, or separate trust funds from personal funds. A trustee needs a system.

Why accounting matters early

Trust accounting is one of the clearest expressions of a trustee’s fiduciary duty. If you can show what came into the trust, what went out, and why, you’re in a much stronger position. If your records are scattered across email folders, personal checking accounts, and handwritten notes, problems start small and grow.

Texas trustees who want a grounded overview of the job itself should understand what a trustee does in Texas. Accounting sits right in the middle of that job. It isn’t separate from administration. It is administration.

Practical rule: If you wouldn’t feel comfortable handing a document to a beneficiary or a judge, don’t rely on it as your only record.

What new trustees often miss

New trustees often focus on investment choices or distributions first. Those issues matter, but recordkeeping usually becomes the bigger source of conflict. A beneficiary may not object to a decision if the decision is explained clearly and backed by records. The same decision can trigger suspicion when the trustee says, “I know I paid that expense, but I can’t find the paperwork.”

A calm, organized trustee usually avoids disputes before they begin. That starts with understanding what Texas requires, and what smart trustees choose to do even when the law doesn’t force it.

What Is a Trust Accounting Under Texas Law

A beneficiary’s letter arrives on a Tuesday. It asks for a trust accounting. The trustee has been paying bills, collecting income, and making occasional distributions in good faith, but the records are spread across bank statements, email attachments, and a legal pad. That is the moment many trustees learn the difference between informal recordkeeping and a true accounting.

Under Texas law, a trust accounting is a formal report that shows how the trustee handled trust property during a stated period. It explains what the trust held, what came in, what went out, what was distributed, and what remains on hand. If you want a plain-English foundation first, review what trust accounting means for a Texas trustee.

Texas handles trust accountings differently from guardianships, and that difference matters. In a guardianship, court-supervised accountings are much stricter and usually mandatory because the court is actively overseeing the fiduciary. A private trust usually works under a demand-based system instead. Beneficiaries have a right to request an accounting, but trustees often get better protection by preparing one voluntarily each year even when no one has asked.

That point is easy to miss.

Many new trustees assume Texas requires an automatic annual trust accounting in every case. Texas generally does not impose that kind of built-in yearly reporting for private trusts. Instead, a beneficiary or other qualified person can make a written demand, usually no more than once in a twelve-month period, and the trustee then has a deadline to respond. So the legal minimum is demand-driven. The practical best practice is often annual.

Here is the simplest way to understand the rule:

| Issue | Texas trust rule |

|---|---|

| Automatic annual accounting | Usually not required by default |

| Who can trigger a formal accounting | A beneficiary or interested person with the right to request one |

| How often they can demand it | Generally not more than once in a 12 month period |

| When the trustee must respond | After a proper written demand, within the statutory deadline |

A trust accounting works like a financial map. A beneficiary should be able to follow the path of each major transaction without guessing why money appeared, disappeared, or changed form. A short email saying the trust is in good shape does not do that. Neither does a stack of uncategorized statements.

If your records are still in raw form, start by learning how to categorize your bank statements. That habit makes trust reporting far easier because an accounting is really organized transaction history with explanations attached.

A clear accounting usually pulls together bank activity, investment statements, income, expenses, distributions, and changes in trust assets. If the trust owns a rental property, a closely held business interest, or mineral interests, the job becomes more detailed, but the goal stays the same. The report should let a beneficiary see what the trustee did and why it was proper.

This is also why voluntary annual accountings are so useful. They lower suspicion before it grows. They force the trustee to catch missing records early. They create a regular habit of review, which is often the best defense if a dispute later develops. A trustee who can produce a clean yearly accounting usually looks careful and credible. A trustee who starts reconstructing years of activity after a conflict starts is already at a disadvantage.

A simple example helps. Suppose the trust holds a brokerage account and a rent house. During the year, the trust receives dividends and rent, pays insurance and repair costs, reimburses a tax payment, and makes one distribution for a beneficiary’s medical needs. A proper accounting gathers those events into one report that answers five practical questions: what the trust started with, what it received, what it spent, what it distributed, and what it still owns.

That level of clarity protects beneficiaries, but it protects trustees too. In practice, that is the smarter way to view annual trust accounting in Texas. It is not only a response to a beneficiary’s right. It is a recordkeeping discipline that helps prevent liability before trouble starts.

The Required Elements of a Formal Texas Trust Accounting

A formal trust accounting is a little like a year-end map of the trust. It should let a beneficiary trace where the property started, what came in, what went out, what was distributed, and what remains. For a trustee, that same map does something equally important. It creates a record that shows careful administration before anyone accuses you of guesswork, favoritism, or sloppy bookkeeping.

That preventive value matters in Texas trust administration. Unlike guardianships, where court-supervised accountings are much stricter and usually mandatory, trust accountings often become the focus only after a beneficiary asks questions or a dispute starts. A prudent trustee does not wait for that moment. A prudent trustee builds a report that would stand up to scrutiny if it were requested tomorrow.

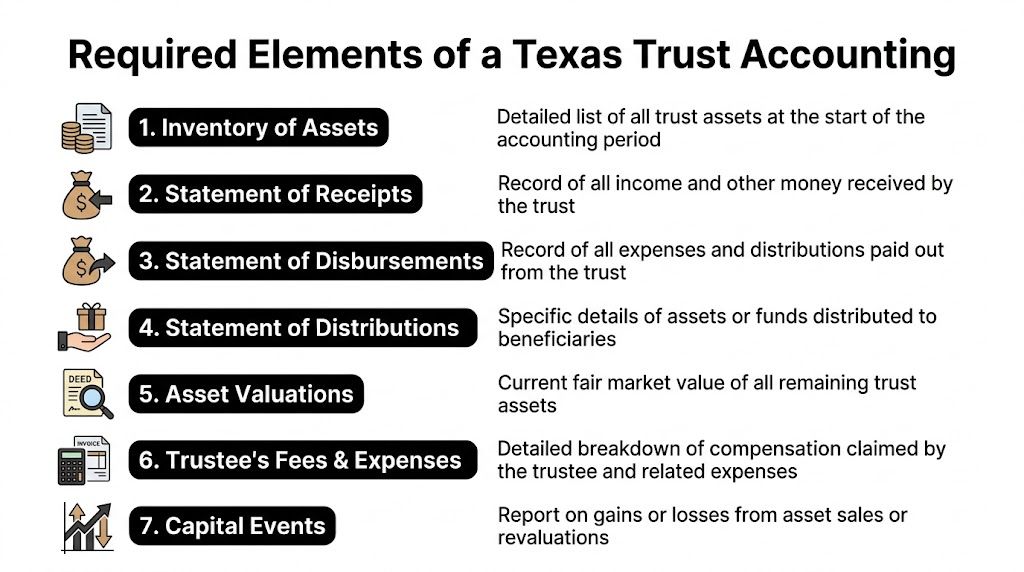

The seven items you need to cover

Texas law gives a practical list of what a formal accounting should include. If you are new to serving as trustee, use these seven items as a working checklist.

Trust property that came into your possession

Start with the property you received or controlled during the accounting period. That may include cash, securities, real estate, business interests, mineral interests, or personal property.Complete receipts and disbursements

Receipts are funds or property coming into the trust, such as rent, dividends, interest, sale proceeds, or refunds. Disbursements are payments going out, such as taxes, insurance, repairs, investment costs, and professional fees.Trustee compensation

If you paid yourself, show it plainly. Trustee compensation is one of the first places beneficiaries look when they are deciding whether the administration was fair.Agent fees

Payments to attorneys, accountants, bookkeepers, property managers, investment advisors, or other agents should appear separately enough to show what service was provided.Distributions to beneficiaries

List each distribution with the date, amount, and recipient. If distributions were unequal, your records should make the reason easy to understand from the trust terms or from written trustee decisions.Property on hand at the end of the period

This is the closing snapshot. It should show what the trust still owns after income, expenses, and distributions.Other material facts needed to understand the account

This category catches the details that make the report readable and fair. It often includes identifying information, explanations of unusual transactions, and a separation of principal from income.

Why the last category causes trouble

Many trustees do reasonably well with dollars in and dollars out. They run into problems with the phrase “other material facts” because it sounds abstract.

In practice, it means you should include whatever a reasonable beneficiary would need to understand the story behind the numbers. If the trust sold a ranch, changed brokers, made a non-cash distribution, or held property that does not show up neatly on a monthly statement, explain that clearly. If a beneficiary later reviews the report alongside Texas beneficiary rights to trust information and accountings, your accounting should answer ordinary questions without forcing that beneficiary to guess.

Here is what that usually means on paper:

- Trust identification with the trust name and current trustee

- Beginning asset listing organized by account or property

- Income entries separated by type, such as rent, interest, or dividends

- Expense descriptions specific enough to show the purpose of each payment

- Principal and income treatment shown separately when the distinction matters

- Ending asset listing that matches the closing balances and property held

A vague entry creates suspicion faster than many trustees expect. “Miscellaneous expense” tells a beneficiary almost nothing. “HVAC repair for trust-owned rental house” is far more useful.

A practical way to build the report

Do not start by worrying about polished formatting. Start with clean records.

A good accounting usually begins with bank statements, brokerage statements, invoices, closing papers, receipts, and distribution records. Then you sort each item into the categories the report must show. Trustees who keep records this way each month usually spend far less time and money preparing an annual accounting than trustees who try to reconstruct a year all at once.

| Step | What to gather |

|---|---|

| Bank activity | Statements, deposit records, checks, transfers |

| Investment activity | Brokerage statements, dividend records, interest entries |

| Property activity | Rent logs, repair invoices, insurance, tax bills |

| Distributions | Dates, amounts, and recipient details |

| Fees | Trustee compensation and payments to professionals |

If your records are scattered, it helps to learn how to categorize your bank statements before you draft the accounting. That kind of sorting makes it easier to separate income from transfers, and trust expenses from personal reimbursements.

A simple example

Suppose the trust owns a rent house and an investment account. During the year, the trust collects rent, receives dividends, pays property taxes, pays for a foundation repair, and makes one distribution for a beneficiary’s education expense.

A proper accounting would show each receipt and each payment separately. It would also show whether the repair was paid from trust cash, whether trustee compensation was taken, and what assets remained at year end. That level of detail protects the beneficiary’s right to understand the administration, but it also protects the trustee who may later need to prove that every transaction had a proper reason.

Detail matters more than presentation

Some trustees use spreadsheets. Others use bookkeeping software or reports generated by a bank or corporate trustee. The format can vary.

What matters is whether the accounting is organized, complete, and understandable. If a report leaves out fee details, lumps transactions together, or hides the difference between principal and income, it may create the very conflict it should have prevented. A careful annual accounting does the opposite. It shows diligence while the facts are still fresh and the records are still easy to verify.

Understanding Fiduciary Duties and Beneficiary Rights

A trustee does not manage trust property for personal convenience. A trustee manages it for the benefit of others, subject to the trust terms and Texas law. That is the heart of a fiduciary duty.

Beneficiaries often hear that phrase and assume it only means “don’t steal.” It means much more. A trustee must act loyally, keep good records, and keep beneficiaries reasonably informed. Accounting fits into all three duties because records are how a trustee proves careful administration.

The trustee’s side of the relationship

A trustee’s core obligations usually show up in everyday choices, not dramatic courtroom moments. Did the trustee keep trust funds separate? Did the trustee document distributions? Did the trustee answer reasonable requests with usable information?

Those questions are why fiduciary duties in Texas are practical, not abstract. If a trustee treats the trust like a personal extension of their own finances, conflict follows. If the trustee treats the trust like a separate legal responsibility with its own records, beneficiaries usually feel more secure.

For people on the beneficiary side, it helps to understand the rights of trust beneficiaries in Texas. The right to request information is one of the main tools that keeps the relationship balanced.

The beneficiary’s right to transparency

Beneficiaries do not control trust property the way trustees do. That imbalance is exactly why accounting rights matter. A beneficiary may have no direct access to the trust bank account, the trust brokerage portal, or the trustee’s bookkeeping system. Without information rights, the beneficiary would have to rely on blind trust alone.

A formal accounting gives the beneficiary a structured way to evaluate management. It also gives the trustee a structured opportunity to show competence.

When trustees communicate clearly, many disputes stay administrative instead of becoming personal.

Why guardianship rules help make this clearer

Texas shows its broader view of fiduciary accountability by treating guardianships even more strictly. Under Texas Estates Code § 1163.001, guardians of the estate must file a mandatory annual accounting with the court within 60 days after each one-year anniversary of appointment, as explained in this overview of Texas guardianship annual accounting obligations.

That comparison is useful. Trustees are usually not under automatic yearly court supervision. Guardians are. The difference tells you two things at once:

- Texas trusts rely more on beneficiary oversight

- Texas expects all fiduciaries to maintain serious financial discipline

A family dealing with incapacity issues often sees both systems up close. If your matter overlaps with a vulnerable adult or estate management, guidance on guardianship can be just as important as trust administration.

The recordkeeping mindset fiduciaries need

The strongest trustees adopt the same disciplined habits that other fiduciaries use. That means separate accounts, clear labels, consistent tracking, and no casual handling of other people’s money. If you want a non-legal operations example of the mindset involved, this guide on strict rules for handling trust accounts illustrates why separation and documentation matter so much.

A trustee who understands this early usually avoids the most common source of beneficiary tension. Silence plus unclear records. Once beneficiaries think information is being withheld, even ordinary transactions can look suspicious.

Common Trust Accounting Pitfalls and How to Avoid Them

A trustee usually gets into trouble the same way a homeowner gets water damage. Not from one dramatic event, but from a slow leak that was easy to ignore at first. Trust accounting problems often build that way. A reimbursement without backup. A transfer recorded too vaguely. A stack of unopened statements waiting for a better weekend.

The good news is that these are usually preventable problems. If you catch them early, you protect both the trust and yourself.

Pitfall one, mixing trust money with personal money

This is the mistake that makes every later explanation harder.

Trust property needs its own lane. Open accounts in the name of the trust, use them only for trust business, and never let trust funds pass through your personal account for convenience. Even a short detour can create doubt about whether the records are complete.

Rules governing lawyer trust accounts reflect the same basic discipline. Texas Disciplinary Rule 1.14 requires record retention and bars commingling, as described in this guide to trust accounting in Texas for small and mid-sized law firms. Trustees are not operating under that exact rule in ordinary trust administration, but the practical lesson is the same. Keep funds separate. Keep records organized. Make every transaction easy to trace.

Pitfall two, poor documentation

Many trustees know why they made a payment when they make it. The problem comes later, when memory has faded and a beneficiary wants proof.

A clean file should answer four simple questions. What was paid. Why it was paid. Which trust account it came from. Where the backup can be found.

Use a routine like this:

- Save the source document such as an invoice, receipt, statement, or written request

- Note the purpose of the payment in plain language

- Match the transaction to the bank or brokerage record

- File it where you can find it without searching through personal email

The tool matters less than the habit. A spreadsheet, bookkeeping software, or a careful folder system can all work if you use it consistently.

Pitfall three, undocumented distributions

Distributions often create the most family tension because they are visible and personal. One beneficiary receives money. Another notices. Questions follow.

That does not mean distributions are suspicious. It means they need context. If the trust allows distributions for health, education, maintenance, or support, your records should show how a particular payment fits that standard. Date, amount, recipient, and reason should all appear in one place.

A note that says, “Paid beneficiary,” leaves room for argument. A note that says, “Distribution for approved medical expense under trust terms,” gives the transaction a legal and factual frame. That small difference can matter a great deal if someone reviews the file later.

Here’s a helpful visual explanation of the habits that keep trustees safer over time.

Pitfall four, treating accounting as a reaction instead of a routine

Many trustees assume accounting becomes important only after a beneficiary asks questions. That mindset creates pressure fast. A trust accounting is much easier to prepare from current records than to rebuild after months or years of informal handling.

This is one reason voluntary annual accountings are such a useful risk-management practice in Texas. They help you catch errors while they are still small, show beneficiaries that trust business is being handled carefully, and reduce the chance that a later demand arrives in an atmosphere of suspicion. Guardians in Texas live under stricter, court-supervised annual accounting rules. Trustees usually do not. That freedom is helpful, but it also means the trustee must supply the discipline.

If you wait until conflict starts, the same records that would have looked orderly six months earlier can suddenly look incomplete.

Takeaway: The safest time to prepare an accounting is before anyone demands one.

Pitfall five, using vague trustee statements

Bank statements and year-end balances are useful, but they are only raw materials. They rarely explain the story of the trust.

A proper trustee report should let a reader follow the movement of money from start to finish. What came in. What went out. Why each significant payment was made. What assets remain. If a beneficiary has to guess at the purpose of major transactions, the report is too thin to calm concern.

A good test is simple. Hand the report to a person who knows nothing about the trust. If that person cannot follow the money without extra explanation, revise the report before sending it.

Pitfall six, waiting too long to get help

New trustees often delay getting advice because they think asking for help signals failure. In practice, it usually signals good judgment.

An accountant can help with transaction tracking and tax reporting. A lawyer can help you interpret distribution standards, respond to beneficiary requests, and correct weak procedures before they turn into liability issues. Outside help costs less when the records are still intact and the relationships are still workable.

Here is a practical prevention checklist:

| Risk area | Safer habit |

|---|---|

| Mixed funds | Open separate, clearly labeled trust accounts |

| Missing receipts | Save and index documents as transactions occur |

| Scrambled year-end records | Reconcile accounts and organize support throughout the year |

| Unclear payments | Add plain-English descriptions to each disbursement |

| Family suspicion | Provide regular, understandable reporting before conflict builds |

Proactive Accounting A Trustee’s Best Tool for Protection

A new trustee often reaches the same moment. A beneficiary asks a few pointed questions, the records are scattered across old emails and bank statements, and the trustee suddenly wonders whether silence has made a routine administration look suspicious.

The safer approach starts much earlier. A careful trustee does not wait for a written demand before getting organized. In Texas, a formal trust accounting is often triggered by a beneficiary request rather than required every year by default. That gives trustees a choice. They can wait and react, or they can provide clear annual reporting on their own and reduce the chance of conflict in the first place.

That choice matters because trust administration is different from guardianship administration. In a guardianship, court-supervised annual accountings are generally part of the job. A private trust usually works under a different standard. The court is not looking over the trustee’s shoulder each year. The trustee has to build the reporting habit personally. For many trustees, that voluntary discipline is one of the best forms of liability prevention available.

Why waiting creates avoidable risk

A written demand for an accounting changes the tone immediately. What might have been an ordinary question can become a deadline problem if the trustee has not kept usable records.

The law matters, but the practical lesson is simpler. Annual reporting prepared before any dispute gives the trustee a clean file, a timeline of decisions, and a chance to correct mistakes while they are still small. It is much easier to explain a transaction at year-end, with records in order, than months or years later after memories have faded.

Regular reporting also helps the trustee spot trouble early. Maybe a distribution was coded incorrectly. Maybe trustee compensation was taken without enough backup. Maybe one beneficiary received information another beneficiary did not. An annual review catches those issues before they harden into accusations.

What a voluntary annual accounting should do

A good voluntary accounting should answer the questions a reasonable beneficiary is already asking. Where did the trust start the year? What came in? What went out? What is left? Were there any unusual decisions that need a short explanation in plain English?

Many trustees prepare a yearly packet with:

- beginning and ending asset values

- income received during the year

- expenses paid from the trust

- distributions to or for beneficiaries

- a brief explanation of unusual sales, expenses, or allocation decisions

- supporting statements or schedules that let a reader verify the summary

The goal is not to impress anyone with formatting. The goal is to create a record that can be followed without a phone call to decode it.

A trustee can treat this like an annual physical for the administration. The report may confirm that everything is fine. It may also reveal small issues that are much easier to fix now than in litigation later.

Why this protects the trustee, not just the beneficiary

Many people hear "accounting" and think only about the beneficiary’s right to information. That is part of the picture, but it is not the whole picture.

Voluntary annual accountings also protect the trustee. They show diligence. They document consistency. They create a regular opportunity to disclose decisions instead of defending them years later. If a beneficiary objects, the trustee learns that sooner, while records are available and the facts are still fresh.

In many administrations, that is the actual value. Prevention costs less than repair.

The added value of receipts and releases

When the circumstances are appropriate, a trustee may ask beneficiaries to sign a receipt and release after reviewing the annual report. Done correctly, that document can confirm that the beneficiary received the information, had a chance to review the trustee’s actions for that period, and agreed not to pursue claims tied to disclosed matters from that time frame.

That step should be handled carefully. A release is not magic paper, and it should match the facts and the trust’s circumstances. Still, as part of a well-run reporting process, it can strengthen the trustee’s protection and reduce later arguments about what was disclosed.

Clear reporting often calms families

Trust disputes often begin with missing context, not missing money.

That is especially true when the trustee is a family member. A sibling, child, or cousin serving as trustee may make perfectly proper decisions, but relatives may still grow uneasy if information arrives late or only after repeated requests. A yearly accounting creates a neutral written record. It gives everyone the same baseline facts and leaves less room for family history to fill in the blanks.

For trustees searching for guidance on annual trust accounting texas, the practical takeaway is straightforward. Texas law may not require a formal annual trust accounting in every trust administration, but providing one voluntarily is often a wise habit. It helps the trustee stay organized, lowers the chance of surprise demands, and builds the kind of record that protects both the trust and the person serving it.

When You Need a Texas Trust Administration Lawyer

Some trustees can handle routine accounting systems on their own. Others shouldn’t try to. The challenge is knowing the difference early enough to avoid a preventable problem.

Signs that legal guidance is worth getting now

A trustee should strongly consider legal help when any of these issues are present:

- You’re serving for the first time and don’t know how to interpret the trust document

- The trust holds complex assets such as rental property, a family business, or hard-to-value property

- A beneficiary is already distrustful or keeps asking for information in a way that suggests conflict is building

- The trust terms are unclear about distributions, compensation, or successor trustee duties

- You received a written demand for accounting and need to respond correctly and on time

- The administration overlaps with probate, guardianship, or incapacity planning

- You’re considering changes to the trust and need advice about how to modify a trust in Texas

A Texas trust administration lawyer can help you build a compliant accounting process before trouble starts. A Texas estate planning attorney can also help families coordinate trusts with broader planning goals, including probate, guardianship, and asset protection.

Legal help is often about prevention

Many people call a lawyer only after relations break down. That is one use for legal counsel, but it’s not the best one. The more valuable use is preventive. A good attorney helps the trustee set up the right accounts, organize records, respond carefully to beneficiaries, and avoid small mistakes that can grow into expensive disputes.

That kind of support matters even more when the trustee is trying to preserve family relationships while carrying out legal duties. Trustees don’t just need answers. They need a process.

If your trust matter touches other planning concerns, it may also make sense to explore related legal support in estate planning, probate administration, guardianship matters, and asset protection so your overall plan works together instead of piece by piece.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process. Whether you need help with trust administration, probate, guardianship, or long-term asset protection, the firm can help you move forward with clarity and confidence.