Skip to content

Skip to content Managing a loved one’s trust can feel overwhelming, especially when you realize you’re not just helping with paperwork. You’re stepping into a legal role with real duties, real deadlines, and real consequences if things go sideways.

Many new trustees in Texas start in the same place. A parent dies, or becomes unable to manage affairs, and a son, daughter, sibling, or close friend suddenly becomes the person responsible for the trust. The trust may own cash, investments, a house, or business interests. Beneficiaries may have questions right away. Some may be patient. Others may want records immediately.

The good news is that trustee accounting obligations texas law imposes are understandable once you break them into pieces. At its core, accounting means keeping clear records and being prepared to show beneficiaries what came in, what went out, what remains, and why. Think of it less like solving a legal puzzle and more like maintaining a careful family ledger that may someday be reviewed by people with legal rights.

If you’ve just taken on this role, you don’t need panic. You do need a system. Texas law expects trustees to act carefully, with integrity, and transparently. When you understand those expectations early, you protect the trust, the beneficiaries, and yourself.

Your Guide to Navigating Texas Trustee Responsibilities

A common scene looks like this. You’ve found the trust documents in a binder or a safe. You’re reading terms that sound formal and dense. Meanwhile, bills still need to be paid, property may need attention, and one beneficiary has already asked, “Can you send me an accounting?”

That moment can make a careful person feel unprepared. It doesn’t mean you’re doing anything wrong. It means you’re now in a fiduciary role, and fiduciary roles come with structure.

Why accounting matters so much

A trust is supposed to hold and manage property for someone else’s benefit. The trustee controls the property, but the trustee doesn’t own it personally. That difference is where most of the legal responsibility comes from.

When trustees keep good records, several things get easier:

- Beneficiary communication stays calmer: Clear records answer questions before they become accusations.

- Tax and reporting work becomes manageable: You can find the supporting documents instead of reconstructing a year from memory.

- Disputes become less likely: People may still disagree, but organized records usually narrow the disagreement.

- Transitions are smoother: If a trustee resigns, dies, or becomes ill, the next person has a trail to follow.

What new trustees usually worry about

Most trustees don’t ask, “What’s the grand theory of fiduciary law?” They ask practical questions.

- What exactly do I have to track? Every asset, income item, expense, debt, and distribution tied to the trust.

- When do I have to share it? That depends on the trust terms, the circumstances, and Texas law governing beneficiary demands.

- How formal does it need to be? More formal than a stack of receipts in a drawer. Less mysterious than many people fear.

- What if the prior trustee left a mess? That’s a real issue, and Texas law has tools for it.

A trustee who keeps records as events happen will almost always have an easier time than a trustee who tries to rebuild the story later.

The Foundation of Trust Fiduciary Duty and Transparency

Trust accounting starts with one idea. A trustee is a fiduciary. That means the law expects the trustee to handle someone else’s property with loyalty, care, and honesty.

A simple analogy helps. If a close relative handed you the keys to a lockbox and said, “Please manage this for my children,” you’d understand two things immediately. First, the contents are not yours. Second, you’d better be ready to explain what you did with them.

Fiduciary duty in plain English

The trustee’s job isn’t to do whatever feels convenient. The trustee must act for the beneficiaries and according to the trust terms. That includes protecting trust property, keeping it organized, avoiding self-dealing, and sharing material information when the law requires it.

Accounting is one of the main ways a trustee proves that duty is being honored. Good accounting shows conduct. It shows whether the trustee collected income, paid proper expenses, preserved assets, and made distributions under the trust instead of from guesswork.

If you want a fuller discussion of the legal standard behind this duty, this overview of trust fiduciary duty is a helpful companion.

Transparency protects both sides

Some trustees hear “accounting” and think it only protects beneficiaries. That’s not the full picture. It also protects the trustee.

A beneficiary who receives a clear report has fewer unknowns. Unknowns are where suspicion grows. If the accounting is organized and supported, the trustee can often answer concerns with documents instead of emotion.

Practical rule: The more control you have over the records, the less control conflict has over you.

What transparency looks like in daily practice

Transparency doesn’t mean constant informal updates about every minor transaction. It means maintaining a system that can explain the trust’s financial story when needed.

That usually includes:

- Keeping trust property separate: Use separate accounts and avoid mixing trust money with personal money.

- Documenting each transaction: If trust funds came in or went out, you should know the date, amount, reason, and supporting paper trail.

- Tracking decisions: If you sold property, paid a major bill, or made a distribution, keep the documents that explain why.

- Communicating thoughtfully: When beneficiaries ask fair questions, respond carefully and consistently.

Why trustees get into trouble even with good intentions

Most accounting problems don’t begin with fraud. They begin with informality. A trustee pays a trust expense from a personal account to “keep things moving.” A distribution gets made before records are updated. Statements pile up unopened. Months later, no one can reconstruct what happened cleanly.

That’s why Texas trust administration is as much about habits as law. Consistent, transparent recordkeeping is the foundation. Everything else sits on top of it.

When and How Often You Must Provide an Accounting

Texas law gives beneficiaries a way to formally request an accounting. This is one of the clearest timing rules a trustee will face, so it’s worth understanding precisely.

Under Texas Trust Code § 113.152, trustees must provide a written statement of accounts to beneficiaries upon written demand, covering all transactions since the last accounting or the trust’s creation. Delivery is required within 90 days, and trustees generally aren’t required to account more than once every 12 months. This obligation is unwaivable for first-tier beneficiaries under § 111.0035, as explained in this discussion of Texas trust accountings: https://fordbergner.com/houston-estate-and-guardianship-litigation-attorney/trust-litigation/seeking-an-accounting-from-a-trustee/

What triggers the duty

The key trigger is a written demand from a beneficiary who has the right to request one. Oral requests may still deserve a thoughtful response, but the formal statutory obligation is tied to a written demand.

That means trustees should treat written beneficiary correspondence seriously. An email, letter, or other writing that clearly asks for an accounting may start the clock.

The timeline in a simple format

| Event | What it means for the trustee |

|---|---|

| Written demand arrives | Review it promptly and confirm the date received |

| Accounting period is identified | Cover transactions since the last accounting or since trust creation, whichever is later |

| Response deadline applies | Deliver the written accounting within 90 days unless a court allows longer |

| Repeat requests | Generally, you don't have to provide one more often than once every 12 months absent court order |

How trustees should respond in practice

A calm response plan helps.

- Record the date of the demand. Save the envelope, email, or letter.

- Identify who requested it. Confirm that the person is a beneficiary entitled to demand an accounting.

- Set the accounting period. Start with the last accounting date, or the trust’s creation if none exists.

- Gather records early. Don’t wait until the final weeks.

- Review for completeness. Missing statements and unexplained transfers create problems.

Trustees who want a practical overview of beneficiary requests may also find this resource useful on how to get trust accounting in Texas.

Where people get confused

The most common confusion is between routine updates and a formal statutory accounting. A trustee might say, “I already told them what’s going on.” But casual updates are not the same thing as a proper written accounting.

Another point of confusion is frequency. Beneficiaries do have rights, but the law also recognizes that trust administration takes time. That’s why Texas generally prevents repeated accounting demands more often than annually unless a court orders otherwise.

If you receive a written demand, treat it like a legal deadline, not a family conversation.

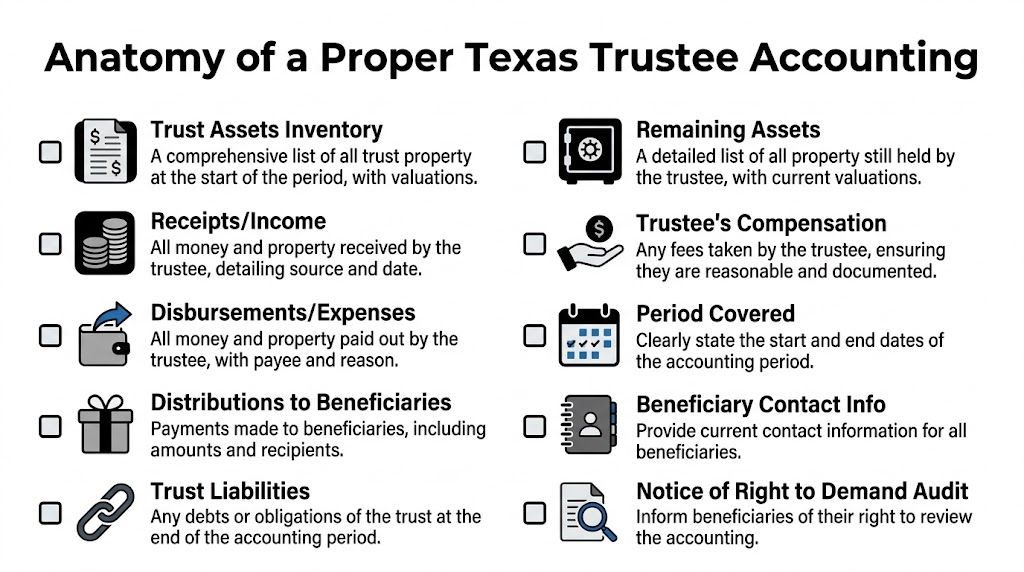

Anatomy of a Proper Texas Trustee Accounting

A proper accounting should tell a coherent financial story. If a beneficiary or judge looked at it, they should be able to understand what the trust owned, what the trustee received, what the trustee paid, what remains, and whether the trustee took compensation.

That sounds formal, but the building blocks are familiar. Bank statements, transaction registers, invoices, closing documents, receipts, and distribution records are the raw materials.

What belongs in the accounting

Texas law expects meaningful detail. A useful working checklist looks like this:

Core contents

- Trust property on hand

- Receipts and income

- Disbursements and expenses

- Distributions to beneficiaries

- Liabilities and debts

- Trustee compensation

- The period covered by the report

A practical accounting often includes these categories in this order:

- Opening assets: What the trust held at the beginning of the accounting period.

- Money in: Interest, dividends, rent, sale proceeds, refunds, or other incoming property.

- Money out: Taxes, repairs, insurance, professional fees, mortgage payments, and similar expenses.

- Beneficiary distributions: What was paid, to whom, when, and under what authority.

- Closing assets: What remains at the end of the reporting period.

- Outstanding debts: Bills or obligations still owed by the trust.

- Trustee fees: Any compensation taken by the trustee, with enough detail to evaluate it.

A plain-language example

Suppose the trust owns a rental house and a brokerage account.

A clean accounting might show the house and account value at the start of the period, monthly rent collected, insurance and repair expenses paid, taxes paid, distributions made to one beneficiary for health expenses under the trust terms, and the asset balances remaining at the end. If the trustee paid herself a fee, that should appear too.

What doesn’t work is a vague summary such as “rent came in, bills were paid, and some money was distributed.” Beneficiaries are entitled to more than conclusions. They’re entitled to a record.

Supporting documents matter

The accounting itself is the summary. The records behind it are the proof.

Texas trustees must maintain financial records, including bank statements, ledgers, and deposit slips, for at least five years after trust administration ends, and monthly reconciliations are strongly advised. That guidance is discussed in this Texas CPA resource: https://www.tx.cpa/docs/librariesprovider15/communications/today's-cpa/2023/january-february/tell-me-more-trustee-duties.pdf?sfvrsn=cbcaab1_3

A recordkeeping system that works

Trustees don’t need fancy software, but they do need discipline. Quicken, QuickBooks, spreadsheets, secure cloud storage, and scanned PDF statements can all help if used consistently.

A practical system usually includes:

- One dedicated trust folder: Digital or paper, but organized by account and month.

- Transaction log: A running ledger with date, payee or source, amount, category, and notes.

- Monthly statement review: Match statements to your ledger and resolve discrepancies.

- Distribution file: Keep support for each beneficiary payment.

- Asset file: Deeds, account statements, appraisals, and ownership records.

A short trustee checklist

Before sending an accounting, ask yourself:

- Can someone else follow it? If only you understand the report, it isn’t finished.

- Does every major number tie to a document? If challenged, can you support it?

- Have you separated trust transactions from personal ones? Mixed records create immediate credibility problems.

- Did you include trustee compensation? Fees should never be hidden or buried.

- Does the period covered make sense? The dates should be clear and complete.

A good accounting doesn’t just add up. It explains itself.

Common Accounting Pitfalls and How to Avoid Them

Many trustee problems are avoidable. They begin with shortcuts that seem harmless in the moment and become hard to explain later.

Mixing trust money with personal money

A trustee pays a property tax bill from a personal checking account because the trust account wasn’t set up yet. Then the trustee reimburses himself later. The intention may be innocent, but the paper trail gets messy fast.

The safer approach is simple. Open and use a separate trust account. If an emergency forces a temporary personal payment, document it carefully, keep receipts, and get legal advice about the cleanest way to handle reimbursement.

Treating family trust property too casually

This happens often with homes and small family trusts. A trustee lets a relative stay in the trust house without clear terms. Another family member pays for repairs and expects reimbursement. No one keeps records because “we all understand.”

That kind of informality causes disputes. Even among cooperative families, memory shifts. Put occupancy terms, repair payments, reimbursements, and approvals in writing.

Poor monthly habits

Some trustees don’t make bad decisions. They just fall behind. Statements accumulate. Receipts stay in a glove compartment. By the time a beneficiary asks questions, the trustee has to reconstruct months of activity.

A simple monthly routine prevents that:

- Download statements: Save bank and investment statements every month.

- Update the ledger: Record each deposit, bill payment, and distribution.

- Match numbers: Reconcile the ledger against the statements.

- Flag unusual items: Large repairs, property sales, or transfers should have supporting notes.

For trustees who want to tighten process and documentation, these internal controls best practices offer useful operational ideas that fit well with trust administration discipline.

Confusing principal and income

A trust may receive cash from different sources, but not all cash is treated the same way. Rent, dividends, sale proceeds, and return of capital can affect different beneficiaries differently depending on the trust terms and governing law.

If you’re handling a trust with investments, rental property, or multiple beneficiary classes, don’t guess. Ask the trust’s CPA or trust counsel how to classify receipts and disbursements.

Making distributions without enough support

A beneficiary may ask for an early payment “just this once.” A trustee may want to help and send funds quickly. If the trust allows discretionary distributions, the trustee still needs records showing the basis for the decision.

A short memo to file can help. Note the request, the trust provision relied on, what information you reviewed, and why the distribution fit the trustee’s duty.

A short practical discussion on trustee mistakes can be useful at this stage:

Letting the prior trustee’s mess become your mess

A successor trustee sometimes takes over and assumes, “I’ll just start from today.” That’s risky if records are incomplete.

Instead:

- Request all records immediately

- Create an inventory of what you received

- List what’s missing

- Avoid approving old transactions you can’t verify

- Get legal advice before signing releases or making final distributions

The best way to avoid trustee liability is to create a clear trail before anyone asks for it.

The Consequences for Failing to Meet Accounting Obligations

Trustees sometimes hope a beneficiary’s request will fade away. That is a mistake. Accounting duties are enforceable, and courts have tools to respond when trustees ignore them.

What can happen after a missed deadline

If a trustee fails to meet the 90-day accounting deadline after a beneficiary’s written demand, the beneficiary can file suit to compel the accounting under Texas Property Code §115.001(9). If a court finds a breach, it can order the trustee to personally pay the beneficiary’s attorney’s fees under §114.064, deny or disgorge trustee compensation, or remove the trustee under §113.082(3). That summary is discussed here: https://www.fiduciarylitigator.com/files/2015/10/Trustee-Duty-To-Disclose-In-Texas.pdf

Why delay creates bigger problems

At first, the issue may seem narrow. A beneficiary asked for records. The trustee delayed. But once litigation starts, the case often expands.

The court may begin looking at broader conduct, including:

- Whether trust funds were handled separately

- Whether distributions were proper

- Whether the trustee took compensation appropriately

- Whether records are missing because duties were neglected

- Whether the trustee should continue serving

That’s why accounting disputes can become removal cases. Lack of transparency causes people to question everything else.

Personal liability is the part trustees often underestimate

Some trustees assume any dispute will be paid by the trust. That is not always true. A court can shift financial consequences directly onto the trustee.

If you’re concerned about that risk, this explanation of trustee personal liability in Texas gives a useful overview.

A practical cause-and-effect view

| Trustee action | Likely consequence |

|---|---|

| Ignores written demand | Beneficiary may file suit |

| Provides incomplete records | Court scrutiny increases |

| Can’t support transactions | Trustee credibility weakens |

| Breach is proven | Fees, lost compensation, or removal may follow |

Courts usually respond better to an imperfect trustee who acted promptly and honestly than to a silent trustee who forced everyone into court.

The lesson isn’t to panic over every request. It’s to respect the role. Trustees who face record problems should deal with them early, document their efforts, and seek legal help before a simple accounting issue becomes a claim for breach of trust.

Navigating Special Accounting Scenarios in Texas

Some accounting situations don’t fit the ordinary pattern. These cases are where trustees and beneficiaries often need more careful legal analysis.

Informal accounting versus court-ordered accounting

Not every accounting begins in a courtroom. Many are handled informally. The trustee prepares a written statement, provides backup as appropriate, answers reasonable follow-up questions, and the administration moves forward.

A court-ordered accounting is different. That usually appears when there’s a dispute, a refusal to provide records, a request for judicial oversight, or a desire for a more formal resolution. The audience changes too. The trustee is no longer just explaining the trust to beneficiaries. The trustee may be explaining conduct to a judge.

Informal accountings can preserve relationships. Judicial accountings can create finality. Which one fits depends on the level of conflict, the trust terms, and the condition of the records.

When a prior trustee dies or becomes incapacitated

This is one of the most overlooked trust administration problems. The old trustee may have handled years of transactions, then died or became unable to continue. The successor trustee takes over but doesn’t know what happened before the transition.

Texas practitioners pay close attention to this because the successor trustee shouldn’t absorb unknown history without a baseline. Case law suggests the deceased trustee’s estate representative may bear the duty to account for the prior trustee’s tenure, and a successor trustee may demand that accounting under Texas Trust Code §113.151(b) to establish a clean baseline and avoid liability for the predecessor’s actions. That issue is discussed here: https://www.stuartgreenlaw.com/what-you-need-to-know-about-trust-accounting

Why the baseline matters

A successor trustee needs to know:

- What assets passed into successor control

- What liabilities were outstanding

- Whether distributions were already promised or made

- Whether funds are missing or undocumented

- Whether tax and reporting obligations were left incomplete

Without that starting point, the successor trustee may have trouble proving which problems belonged to the predecessor and which arose later.

What a successor trustee should do quickly

The first days matter. A careful successor usually needs to act in this order:

- Secure current accounts and property. Change access where needed and protect records.

- Request a final accounting from the predecessor or estate representative.

- Inventory what you received. List assets, statements, keys, passwords, deeds, and files.

- Create a missing-records list. Be specific.

- Document uncertainty rather than guessing. Unknown items should stay marked as unresolved.

- Delay final distributions if the history is unclear. A rushed closing can create new liability.

Successor trustees should resist the urge to “smooth things over” by filling gaps with assumptions. Assumptions become liabilities.

Beneficiary concerns in transition cases

Beneficiaries often feel anxious when they hear that a prior trustee failed to keep records or can’t finish the job. That concern is understandable.

The practical response is transparency. Explain the transition, identify what records are being requested, and avoid overstating what you know. A measured update is better than a confident but unsupported answer.

Frequently Asked Questions and Your Next Steps

Can a Texas trust document waive the duty to account completely

Not for core duties owed to first-tier beneficiaries. Texas law treats certain accounting and disclosure protections as non-waivable in that context. If a trust document appears to limit information rights, it still needs careful review against Texas fiduciary law.

I’m a beneficiary and I disagree with the accounting. What should I do

Start by identifying the exact issue. Is something missing, unclear, unsupported, or inconsistent with the trust terms? A focused written objection is more useful than a broad accusation.

Good next steps often include:

- Request clarification in writing

- Ask for supporting records tied to specific transactions

- Compare the accounting to prior statements or known assets

- Speak with a Texas trust administration lawyer if the answers don’t resolve the concern

How detailed do my trustee records need to be

Detailed enough that another person can follow the money. That usually means statements, ledgers, receipts, invoices, confirmations, closing papers, and notes explaining unusual transactions or discretionary distributions.

If a transaction would raise a reasonable question later, keep the support now.

What if I inherited poor records from the trustee before me

Don’t adopt those records as accurate without review. Identify what you received, what you didn’t receive, and what you need to request. Keep your own administration clearly separate from the predecessor’s period so you don’t blur responsibility.

Do I need a lawyer, CPA, or both

Sometimes one professional is enough. Many trusts benefit from both. A lawyer helps with fiduciary duties, beneficiary rights, demands for accounting, trust interpretation, and disputes. A CPA helps with tax reporting, classification issues, and organized financial reporting. In more complex trusts, that team approach prevents expensive mistakes.

If you’re managing a trust, planning your estate, or dealing with questions about probate, guardianship, or asset protection, getting specific advice early can save significant stress later. The role of trustee is manageable when you have a clean process and the right guidance behind it.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including estate planning, probate, guardianship, asset protection, trust administration, and fiduciary disputes.