Skip to content

Skip to content Managing a loved one’s trust can feel overwhelming, especially when the mail starts arriving with tax forms, bank statements, and questions from beneficiaries. Many new trustees worry they’re one mistake away from creating a tax problem, upsetting family members, or violating Texas law.

That anxiety is normal. You’re being asked to protect property, follow legal instructions, keep records, and make tax decisions that may affect other people for years. If you’ve found yourself searching for trust taxation texas because you need clear answers, you’re in the right place.

A common scenario looks like this. A parent dies, an adult child becomes trustee, and the trust owns a home, an investment account, and maybe mineral interests or family land. The trustee knows taxes matter, but they don’t know where to start. They’ve heard Texas is tax-friendly, but they’re not sure what that means in practice.

Texas law does give trustees important advantages. But those advantages work best when you understand both the Texas rules and the federal tax rules that still apply. Your role under the Texas Trust Code also includes fiduciary duties such as loyalty, prudent management, accurate records, and proper communication.

If you’re new to this role, it helps to first understand what a trustee does in Texas. Once that foundation is in place, the tax side becomes far less intimidating.

Introduction Navigating Your Role as a Texas Trustee

The first thing most trustees need to hear is this. You don’t need to know everything on day one. You do need a workable process.

A trustee’s job sits at the intersection of family responsibility and legal responsibility. Under the Texas Trust Code, trustees must act in good faith, keep accurate records, and administer the trust according to its terms. Under the Texas Estates Code, families may also deal with probate, pour-over wills, beneficiary rights, and estate administration issues that affect what property becomes part of the trust.

Why taxes feel harder than they are

Taxes create stress because the rules use unfamiliar labels. You may hear terms like grantor trust, non-grantor trust, distributable net income, principal, income, and fiduciary accounting. To a new trustee, that can sound like a separate language.

But the core questions are simpler:

- What kind of trust is this

- Who pays the income tax

- Did the trust distribute income to a beneficiary

- Does the trust need its own tax return

- Are there any cross-state issues that could create unexpected tax exposure

Most trustee tax problems don’t start with dishonesty. They start with confusion, delay, or incomplete records.

Your first practical mindset shift

Don’t think of tax compliance as a side task. Think of it as part of administration itself. A careful trustee tracks income, expenses, distributions, and asset ownership as part of regular trust management. That’s what helps you satisfy your fiduciary duties in Texas and avoid disputes later.

For many families, the biggest relief comes from learning that Texas does not add a state income tax layer for trusts. That doesn’t erase federal filing requirements, but it does simplify the tax situation. Once you know how the trust is classified and how distributions affect taxation, the path becomes much clearer.

Understanding the Basics of Trust Taxation

You open the year-end mail for the trust and find a stack of tax documents. A brokerage statement shows dividends. A tenant paid rent into the trust account. One beneficiary asked for a distribution. Another lives outside Texas. At that moment, the question is no longer whether taxes apply. The question is who must report what, and how Texas changes the strategy.

The starting point is simple. A trust can collect income, hold assets, and make distributions. The IRS therefore may treat the trust as its own taxpayer, much like a separate bucket that catches income before that income is taxed to someone. In some cases, the income stays in that bucket and the trust pays. In others, the income passes through to the grantor or to a beneficiary.

Why a trust gets taxed at all

A trust is a legal arrangement for holding property for someone else’s benefit. Once that property begins producing earnings, the tax system has to assign responsibility. Interest, dividends, rent, capital gains, and royalties do not go untaxed just because they sit inside a trust.

Federal trust income tax rules, mainly under Internal Revenue Code Sections 641 through 683, answer that assignment question. They determine whether the trust is ignored for income tax purposes, taxed as a separate entity, or allowed a deduction because income was distributed to a beneficiary.

A few terms make the system easier to read:

- Fiduciary income is money the trust receives, such as interest, dividends, rent, or royalties.

- Principal is the property already in the trust, such as cash transferred into the trust, real estate, or securities.

- Income is the earnings produced by that property.

- Taxable income is the amount that remains subject to tax after the applicable rules and deductions are applied.

Those labels matter because trustees often confuse income with principal. That confusion causes real problems. A beneficiary may be entitled to one, but not the other. The tax result can change based on that distinction.

Federal tax rules answer one set of questions. Texas law answers another.

Texas law tells you how to administer the trust. Federal law tells you how the income is taxed.

That division trips up many new trustees. The Texas Trust Code governs administration issues such as trustee powers, accounting, duties, and beneficiary rights. Federal tax law governs who reports trust income and whether the trust files its own return.

Texas then adds an important strategic benefit. Texas does not impose a state income tax on trusts. That does not mean a Texas trust is free from all tax concerns. It means you start without a Texas state income tax layer, which can make trust administration cleaner and planning more flexible.

That advantage matters most when a trust has connections outside Texas. If a trustee, beneficiary, trust asset, or source of income is tied to another state, that other state may still claim a filing requirement or try to tax some portion of the trust’s income. A Texas trustee should therefore ask not only, "Do we owe Texas tax?" but also, "Does another state have a reason to care about this trust?"

What this means in practice

A Texas trust with no state income tax can still face a costly surprise if the trust owns rental property in another state, earns income sourced to another state, or has enough contacts with a taxing state to trigger a return there.

That is the hidden planning point. Texas gives you room to work with, but it does not erase cross-state exposure.

A careful trustee usually starts with four practical questions:

| Question | Why it matters |

|---|---|

| What kind of income did the trust receive | Different types of income can be taxed and reported differently |

| Who is treated as the taxpayer | The grantor, the trust, or the beneficiary may report the income |

| Did the trust make distributions during the year | Distributions can shift taxable income away from the trust |

| Does another state have a connection to the trust | Trustee residence, beneficiary residence, asset location, or income source can create extra filing issues |

A simple example

Suppose a Texas trust owns an investment account in Dallas and a rental house in New Mexico. The trust receives dividends from the account and rent from the house. Texas does not impose a state income tax on that trust income. But New Mexico may still require filing and may tax the rental income sourced to property located there.

Now add one more fact. The trust keeps part of the income and distributes part to a beneficiary. You can see how the tax picture starts to split into layers. One set of rules decides whether the trust or the beneficiary reports the distributed income. Another set decides whether any state outside Texas can tax part of what the trust earned.

That is why trust taxation is easier to handle when you treat it as a series of assignments. First identify the income. Then identify the taxpayer. Then check whether any state outside Texas has a claim. Once you work through those steps, the rules stop feeling like a wall of jargon and start looking like an organized checklist.

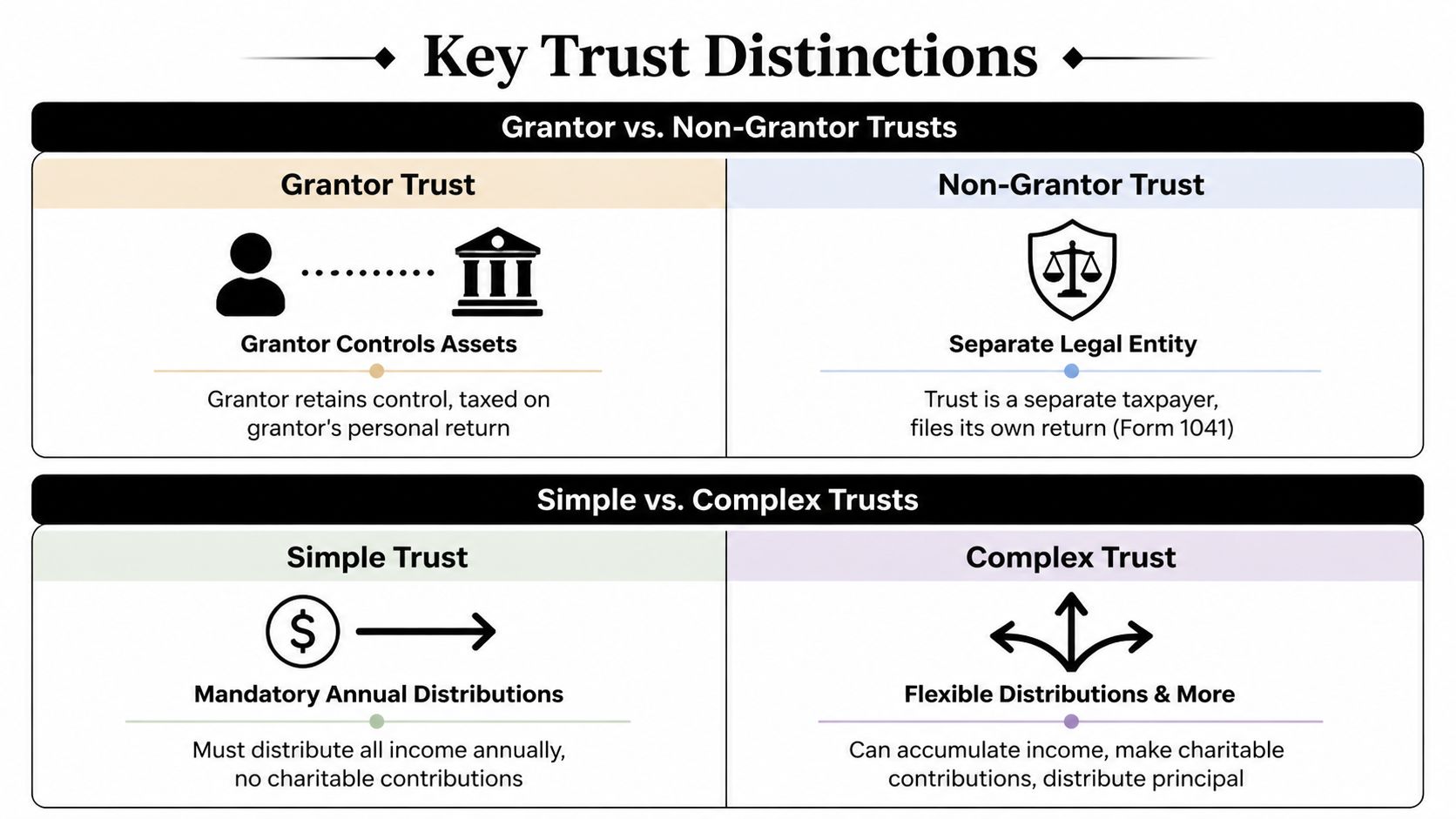

Grantor vs Non-Grantor and Simple vs Complex Trusts

Most trustee confusion starts with labels. The good news is that these labels answer one main question. Who pays the tax?

Some labels focus on the relationship between the trust and the person who created it. Others focus on how the trust handles distributions. Both matter.

For a deeper discussion of planning with irrevocable trusts, many trustees also review Texas irrevocable trust tax benefits.

Grantor trusts

A grantor trust is a trust whose income is taxed to the person who created it, rather than to the trust itself. Under IRC §§ 671-679, the grantor remains responsible for the income tax. The trust may still exist for legal and planning purposes, but the income is pulled back onto the grantor’s tax return.

This is why many revocable living trusts are easy from an income tax standpoint during the grantor’s lifetime. The trust may hold the assets, but the tax reporting still lands with the grantor.

Verified guidance also notes that grantor trusts can avoid compressed trust tax brackets. Trusts reach 37% at $15,200 of income, while individuals reach 37% at $609,350. In some planning situations, grantors in the 32% to 35% range funding growth assets may see 10% to 20% savings, as summarized in this grantor trust discussion.

Non-grantor trusts

A non-grantor trust is treated as a separate taxpayer. The trust itself may owe tax, or the beneficiaries may owe tax on distributed income, depending on what the trust distributes.

This is the category where trustees often need to focus carefully on Form 1041, beneficiary reporting, and year-end distribution decisions. If the trust keeps income instead of distributing it, the trust may pay tax at those compressed trust rates.

Practical rule: If you’re administering a non-grantor trust, don’t assume the trust should always retain income. Distribution timing can affect both taxes and fiduciary outcomes.

Simple trusts

A simple trust must distribute all income annually, doesn’t distribute principal, and doesn’t make charitable contributions during that year. In tax practice, this usually means the income moves out to beneficiaries and is reported accordingly.

Simple doesn’t mean easy. It just means the trust has tighter rules about what it must distribute.

Complex trusts

A complex trust has more flexibility. It may accumulate income, distribute principal, or make charitable contributions if the trust terms allow it.

That flexibility can help with planning. It can also create more decisions for the trustee. A complex trust often requires closer coordination with the drafting attorney and CPA so that distribution choices line up with both the trust document and the tax consequences.

A side-by-side comparison

| Trust type | Main idea | Who usually pays income tax |

|---|---|---|

| Grantor trust | Grantor keeps tax responsibility | Grantor |

| Non-grantor trust | Trust stands apart as taxpayer | Trust or beneficiary |

| Simple trust | Income must be distributed annually | Beneficiary on distributed income |

| Complex trust | Income may be retained or distributed | Trust, beneficiary, or both depending on distributions |

Where trustees usually get tripped up

A trustee may think these categories are exclusive, but they overlap. A trust can be non-grantor and complex. Another can be grantor and simple in operation, though the tax effect still follows grantor trust rules.

A real-world Texas example helps. Suppose a parent created an irrevocable trust for adult children. The parent no longer controls the trust, so it may be a non-grantor trust. If the trustee can either hold income for future needs or distribute it this year, it may also be a complex trust. That means the trustee has actual tax planning choices to make.

The trust instrument controls many of those choices. So does Texas fiduciary law. A trustee can’t use tax strategy as an excuse to ignore beneficiary rights or the terms of the trust.

Federal Filing Mechanics Form 1041 and Schedule K-1

When a trust needs its own federal income tax return, the key form is Form 1041. Think of it as the trust’s version of an individual income tax return.

For trustees, theory translates into paperwork. The form reports the trust’s income, deductions, and distributions. It also helps determine whether tax stays at the trust level or passes through to beneficiaries.

What Form 1041 does

Form 1041 gathers the trust’s financial story for the year. A trustee or tax preparer uses it to report items such as:

- Interest and dividends from bank or brokerage accounts

- Rental or royalty income from trust property

- Deductions and expenses tied to administration

- Distributions to beneficiaries that may carry out taxable income

For trusts owning Texas real estate, oil and gas interests, or a business interest, organized income and expense records are essential. Under the Texas Trust Code, that kind of accounting isn’t optional. It’s part of acting prudently and keeping beneficiaries informed.

Why distributions matter so much

A trust and a beneficiary generally shouldn’t both pay tax on the same income. The tax rules use a distribution deduction system to help prevent that result.

If the trust distributes certain income to a beneficiary, the trust may deduct that amount, and the beneficiary may report it instead. That’s why year-end decisions can change the tax result.

Verified Texas trust guidance notes that irrevocable trusts can remove assets from the grantor’s taxable estate and may reduce federal estate taxes under IRC § 2001, which can impose rates up to 40% on estates over $13.61 million. That same guidance also emphasizes annual CPA reviews and distribution planning under Texas Trust Code § 113.051 because undistributed trust income can be taxed at 37% at $15,200 in a non-grantor trust, as discussed in these Texas trust tax strategies.

What Schedule K-1 tells beneficiaries

After the trust return is prepared, the trustee may need to issue Schedule K-1 to each beneficiary who received reportable income. The K-1 tells the beneficiary what share of income, deductions, or credits they need to include on their own return.

That’s why beneficiaries often call trustees in tax season. They’re waiting for the K-1 so their CPA can finish their personal return.

A delayed K-1 can frustrate beneficiaries quickly. A trustee who keeps clean books throughout the year makes tax season easier for everyone.

A practical filing workflow

Many trustees benefit from a simple annual checklist:

Confirm the trust’s classification

Is it grantor or non-grantor. Does it need a separate trust return this year.Gather income records

Collect year-end statements, brokerage reports, royalty statements, rent records, and expense support.Review distributions

Identify what the trust distributed, when, and whether those distributions carry out taxable income.Coordinate with professionals

A CPA prepares the return, but the trustee provides the facts. A Texas trust administration lawyer helps if the trust language is unclear.Deliver beneficiary tax information promptly

If K-1 forms are required, send them on time and keep copies with the trust file.

A trustee who follows that workflow is much less likely to face disputes over taxes, accounting, or delayed reporting.

The Texas Advantage No State Income or Estate Tax

A new trustee often hears, “Texas has no state income tax,” and assumes the tax analysis ends there. In practice, that is only the starting point. For many trusts, Texas’s no-income-tax status creates planning choices that can preserve more wealth over time, but those choices only work if the trust’s administration stays aligned with Texas.

What the Texas advantage really means

At the state level, Texas does not impose a personal income tax, and Texas also does not impose a separate state estate tax. For a trustee, that usually means one less tax system to manage. You are generally focused on federal reporting, federal income tax rules, and the trust’s actual administration rather than preparing a separate Texas fiduciary income tax return.

That simplicity matters.

A trust that avoids state income tax drag may keep more of its earnings invested for beneficiaries. Over many years, that can make a real difference, especially for trusts that hold appreciating investments, business interests, ranch land, or mineral assets that produce ongoing income.

Texas’s tax climate also shapes strategy. Families sometimes choose Texas trustees, Texas administration, and Texas situs because the absence of state income tax can make long-term trust administration cleaner and, in some cases, less expensive.

The hidden catch: other states may still matter

A Texas trust is not automatically protected from every other state’s tax rules. State trust taxation works more like a map with overlapping borders than a single label on the front of the trust document.

Here are common examples:

A trustee lives in another state

Some states look at trustee residence when deciding whether a trust has enough connection to be taxed there.A beneficiary lives in a high-tax state

Depending on that state’s rules, beneficiary residence can affect filing duties or tax treatment.The trust is administered outside Texas

If records, decision-making, and day-to-day management shift elsewhere, the trust’s practical center may shift too.The trust owns out-of-state property or business interests

Real estate, operating businesses, and certain royalties can create tax obligations where the asset is located.

This is the point many families miss. “Texas trust” is not a magic shield. It is a favorable home base, but trustees still need to watch where the trust is being run and where its assets and people are located.

Trustee selection can affect taxes

Choosing a trustee is partly a family decision and partly a tax decision.

A useful way to view it is this. The trustee is not just the person signing checks. The trustee is often one of the facts a state will examine when deciding whether the trust has a taxable connection there. A well-meaning successor trustee who lives in a high-tax state may change more than the mailing address.

| Planning question | Why it matters |

|---|---|

| Where does the acting trustee live | Trustee residence can affect state tax exposure |

| Where are key trust decisions made | Decision-making location may influence nexus |

| Where are the beneficiaries located | Some states consider beneficiary residence |

| What assets does the trust own | Real estate, royalties, and business interests may trigger tax in other states |

For that reason, trustee selection should be discussed alongside tax planning, not after it.

The video below offers added background on Texas trust and tax planning.

Why families use Texas for long-term planning

Texas can be an attractive place for long-term trust planning because the state combines a no-income-tax environment with a clear statutory framework for trust administration. That combination can reduce friction for trustees and preserve flexibility for families who expect a trust to last for many years.

The practical opportunity is straightforward. If a family has a choice about trustee location, place of administration, or trust situs, Texas may offer a cleaner tax result than a higher-tax state. The practical risk is just as important. If the trust later drifts into another state through a new trustee, relocated administration, or concentrated assets elsewhere, part of that advantage may weaken.

For a trustee, the takeaway is reassuring. You do not need to master every state’s tax code on day one. You do need to recognize that Texas’s no-tax status is a planning benefit that should be preserved deliberately, with careful attention to who serves, where decisions are made, and where the trust’s connections really are.

Estate and Generation-Skipping Transfer Tax Considerations

Income tax is only part of the picture. Some trusts are also built to address transfer taxes, meaning taxes imposed when wealth moves from one generation to the next.

For many Texas families, the biggest transfer tax question is the federal estate tax. Texas doesn’t impose its own state estate tax, but federal law still matters for larger estates.

Federal estate tax and Texas planning

Verified guidance states that in 2026, the federal estate tax exemption is $13.61 million per individual, adjusted annually for inflation, and federal estate tax rates can reach 40% on amounts over that exemption. Texas has no state estate tax, unlike 12 states plus D.C. that have estate or inheritance taxes, according to this Texas trust and estate tax overview.

For families above or near that level, trust planning becomes more than probate avoidance. It becomes tax planning.

A revocable living trust may help avoid probate, but its assets are generally still included in the grantor’s taxable estate. An irrevocable trust, by contrast, can move assets out of the taxable estate if it is properly designed and funded.

Why irrevocable trusts matter here

Suppose a person owns appreciating assets and wants future growth outside the taxable estate. An irrevocable trust may serve that purpose because the grantor gives up enough control for the assets to be excluded from the estate.

That can matter not only for estate tax, but also for family governance. The trust can continue to manage property for children or grandchildren under clear terms, instead of passing assets outright.

Trust planning works best before there is a crisis. Once a person has lost capacity or died, many tax-saving options narrow quickly.

Families evaluating this type of planning often also benefit from reviewing portability and estate tax planning in Texas.

Generation-skipping transfer tax in plain English

The generation-skipping transfer tax, often called GST tax, is designed to prevent families from skipping a generation and avoiding transfer tax at each level. In simple terms, if wealth moves in a way that benefits grandchildren or later generations directly, GST tax may need attention.

Verified Texas trust guidance notes that trustees must also manage GST taxes at a 40% rate in applicable cases. That’s one reason high-value trusts often require careful drafting, exemption allocation, and long-term administration discipline.

A practical family example

A grandparent may want to leave assets in trust for children during their lifetimes and then continue the trust for grandchildren. That approach can promote creditor protection and family control. But if the trust is not structured carefully, the family may miss opportunities to use available transfer tax exemptions.

That’s where a Texas estate planning attorney and CPA often work together. The attorney focuses on structure and compliance with the Texas Trust Code and Texas Estates Code. The CPA focuses on tax reporting and exemption use. The trustee then carries out those decisions through proper administration.

Tax Planning Strategies and a Trustee's Fiduciary Duties

A trustee often starts tax planning with the wrong mental picture. It can feel like a side task for April, separate from distributions, investments, and beneficiary questions. Under Texas law, it is part of the main job. If a trustee misses an avoidable tax cost, that mistake can reduce what the trust preserves for the people it was created to benefit.

The Texas Trust Code expects trustees to act in good faith, keep accurate records, and manage property for the beneficiaries under the terms of the trust. Tax decisions fit inside those duties. In practice, that means a trustee should ask a simple question before major decisions: how does this choice affect both the trust’s taxes and the fair treatment of beneficiaries?

Your tax choices are also fiduciary choices

Texas gives trustees a real planning advantage because Texas does not impose a state income tax on trusts. But that advantage is not a free pass to ignore strategy. It changes the strategy.

A useful way to look at it is this. The absence of Texas state income tax removes one layer of cost, but federal income tax still matters, and other states may still enter the picture. If a non-grantor trust keeps income, the trust may pay federal tax quickly at compressed rates. If the trust distributes income to beneficiaries who are in lower tax brackets, the overall family tax burden may be lower. The trustee still has to follow the trust document, exercise discretion responsibly, and avoid favoring one beneficiary unfairly.

The hidden trap is cross-state contact. A Texas trust with a trustee in another state, a beneficiary in another state, or income-producing property outside Texas can raise state filing or nexus questions. Texas’s no-income-tax status is helpful, but it does not shield the trust from every other state’s rules.

A practical trustee roadmap

Good trust tax planning usually looks ordinary from the outside. It is built on timing, records, and disciplined review.

Read the trust document before making distributions

Distribution authority is the starting point. Some trusts require current income distributions. Others permit accumulation. A trustee cannot choose the better tax result if the trust terms do not allow that choice.Separate principal from income carefully

Trustees often get into trouble by treating every dollar received as if it works the same way. It does not. Rent, dividends, sale proceeds, royalties, and reimbursement payments can affect beneficiaries differently and may be accounted for differently under trust law and tax rules.Review year-end options before year-end arrives

Waiting until returns are being prepared often means the useful choices have already passed. A review late in the year can help the trustee decide whether distributions, expense allocation, or other administrative actions still make sense.Watch for out-of-state connections

This point matters more in Texas because trustees sometimes assume "Texas trust" means "Texas tax result." That label can be misleading. Trustee residence, asset location, business activity, and beneficiary residence may all matter.Write down the reason for key decisions

A short memo can do a lot of work later. If a beneficiary questions why income was distributed, or why it was retained, a written explanation helps show the trustee acted thoughtfully rather than casually.

Trustee reminder: Good records support tax reporting, but they also protect the trustee if a beneficiary later claims the decision-making was careless or unfair.

When to bring in professional help

Asking for guidance is often a sign of prudence, not weakness.

A trustee may need a Texas trust administration lawyer when:

- The trust language is unclear

- Beneficiaries disagree about distributions

- The trust owns a business, ranch, or mineral interests

- A trustee lives in one state and beneficiaries live in another

- There’s a question about modifying, terminating, or decanting the trust

- A dispute is forming over accounting or fiduciary conduct

A CPA can be especially helpful when the trust has investment income, royalty income, multiple beneficiaries, or questions about DNI and K-1 reporting. A Texas estate planning attorney and CPA often collaborate on these issues. The attorney addresses authority, fiduciary standards, and trust terms. The CPA handles reporting positions, return preparation, and the tax effect of distribution choices.

The Law Office of Bryan Fagan, PLLC handles trust administration, estate planning, asset protection, and probate-related matters in Texas, which may be useful when a trustee needs legal guidance along with tax preparation and beneficiary communication.

Trustee duties under Texas law

A trustee’s tax decisions should fit within broader fiduciary principles:

| Fiduciary principle | Tax-related example |

|---|---|

| Loyalty | Avoid favoring one beneficiary through careless tax choices |

| Prudence | Review tax consequences before retaining or distributing income |

| Recordkeeping | Maintain statements, receipts, returns, and K-1 copies |

| Communication | Provide beneficiaries with needed information in a timely way |

These duties often overlap with other family planning issues. A trust may hold property tied to probate administration, support a beneficiary after incapacity, or fit into a larger asset protection plan. For that reason, tax planning is rarely just about lowering a tax bill. It is also about carrying out the trust in a way that is legally sound and fair to the people involved.

What if the trust needs to change

Sometimes the best tax result is blocked by the trust’s existing terms. A trustee may then need to ask whether the trust can be modified, terminated, or adjusted under Texas law.

That question usually comes up for practical reasons, not academic ones. The family’s assets may have changed. The beneficiaries may now live in multiple states. The current distribution standard may create tax friction that did not matter when the trust was drafted. In those cases, the trustee has to balance tax efficiency with fiduciary limits, beneficiary interests, and the procedures allowed under the Texas Trust Code and, in some situations, the Texas Estates Code.

People searching for how to modify a trust in Texas are often dealing with exactly that kind of problem. The underlying concern is not solely taxes. It is whether the trust still fits the family’s current situation and whether the trustee has a lawful path to improve administration.

Conclusion Your Next Steps to Confident Trust Administration

The overwhelmed trustee from the opening usually changes in a predictable way. At first, they see only forms, deadlines, and risk. After they learn the framework, they start seeing categories, decisions, and manageable next steps.

That’s the primary goal in understanding trust taxation texas. Not to memorize every tax rule, but to know how the system fits together. Federal law usually drives income tax reporting. The type of trust controls who pays the tax. Texas offers unusual advantages because it doesn’t impose state income tax on trusts or a state estate tax. But cross-state facts can still create problems if no one is watching for them.

You also don’t have to carry the entire burden alone. Trustees often do their best work when they treat administration as a team effort involving legal advice, CPA support, organized records, and steady communication with beneficiaries. That approach protects both the trust and the trustee.

If you’re serving as a trustee, acting as an executor, receiving questions from beneficiaries, or evaluating a new estate plan, careful guidance can make the process calmer and clearer. The right legal support can also help with related concerns involving probate, guardianship, trust modification, and long-term asset protection.

The law expects care, honesty, and diligence from trustees. It does not expect you to guess.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process.