Managing a loved one’s trust can feel overwhelming, especially when the first question you ask is, “What records am I supposed to keep, and who do I have to show them to?”

That feeling is normal. Most trustees aren’t professional fiduciaries. They’re spouses, adult children, siblings, or close family friends who were asked to step into a position of trust during a stressful season.

Texas law takes trust accounting seriously, but the goal isn’t to trap honest trustees. The goal is to create a clear paper trail so beneficiaries can understand what happened, and so trustees can show they acted carefully, fairly, and in good faith. If you approach the job with organized records and steady communication, trust administration becomes much more manageable.

This guide walks through trust accounting requirements texas trustees need to understand, in plain English. I’ll explain when a formal accounting is required, what it must include, where trustees often get confused, and how to avoid the mistakes that lead to disputes.

Your Role as Trustee Navigating Texas Trust Law

A new trustee often starts in the same place. You find the trust document, look at a pile of bank statements, maybe a deed, maybe mineral paperwork, and then realize people are now expecting answers from you.

That can feel like being handed the keys to a house you didn’t build. You didn’t choose the plumbing or wiring, but now you’re responsible for keeping everything working.

Your role is larger than “holding property.” You’re a fiduciary, which means Texas law expects you to act for the benefit of the beneficiaries, not for your own convenience. That includes protecting trust assets, following the trust terms, making sensible decisions, and keeping accurate records.

For many trustees, one of the most helpful early steps is understanding the full scope of trustee responsibilities after death, because accounting duties make more sense once you see how they fit into the broader administration process.

A trustee who keeps good books is in a much stronger position than a trustee who relies on memory. If a beneficiary asks why a bill was paid, why a distribution was delayed, or why an asset was sold, your records should answer the question without guesswork.

Why accounting protects you too

Some trustees think accounting is only for the beneficiary’s benefit. That’s incomplete.

A proper accounting also protects the trustee. It shows what came into the trust, what went out, who received distributions, what fees were paid, and what property remains. In other words, it tells the story of your administration.

Start with the basic duties

Early in the process, it helps to review a practical summary of trustee duties in Texas. That bigger picture matters because accounting isn’t an isolated chore. It’s one part of careful Texas trust administration, along with communication, investment oversight, distributions, and compliance with the trust’s terms.

A trustee who documents decisions as they happen usually avoids the panic that comes later when someone asks for proof.

If you’re new to this role, don’t aim for perfection on day one. Aim for order, consistency, and a clear system.

Understanding Your Core Duty of Accountability

Being a trustee is a little like being the guardian of a family vault. The property inside may include cash, a home, investment accounts, business interests, or royalty income. You may control access, but you don’t own the contents personally. You’re managing them for someone else under rules you didn’t create.

That’s why accountability sits at the center of fiduciary duty.

Duty to inform and duty to account are not the same

This is one of the biggest points of confusion for trustees.

Texas law recognizes a difference between the trustee’s broader duty to inform and the narrower duty to account. A Texas CPA resource discussing trustee duties explains that the common-law duty to inform is broader, is non-waivable under Texas Trust Code § 111.0035, and includes proactive updates about asset status and key decisions, while Texas Trust Code § 113.151 governs formal accountings. That distinction matters because many disputes begin when beneficiaries feel left in the dark even though a formal accounting is not yet due (Texas CPA discussion of trustee duties).

Here's a simple explanation:

| Duty | What it means in plain English | Example |

|---|---|---|

| Duty to inform | Keep beneficiaries reasonably updated about important trust matters | Telling beneficiaries that trust real estate was listed for sale |

| Duty to account | Provide a formal financial report with required details | Delivering a written accounting after a proper demand |

If you only focus on the formal accounting rules, you can still run into trouble. A beneficiary may not need a statutory accounting yet, but they may still expect reasonable information about what’s happening.

What beneficiaries usually want to know

Most beneficiaries aren’t asking for trouble. They’re asking for clarity.

They often want answers to practical questions like:

- What assets are in the trust

- Has any money come in

- What bills or expenses have been paid

- Have any distributions been made

- Why was a major decision made

If you communicate those basics clearly and calmly, you may prevent conflict before it starts.

Accountability is an ongoing habit

Formal accountings tend to get attention because they sound official. But the stronger habit is steady recordkeeping and regular communication.

Consider two trustees:

- Trustee A keeps trust money in a separate account, saves receipts, notes distributions, and sends periodic updates.

- Trustee B mixes trust mail with personal papers, pays expenses without labeling them, and waits until someone complains.

Trustee A can usually respond with confidence. Trustee B often feels attacked, even when the beneficiary’s request is lawful and predictable.

Practical rule: If a beneficiary asks, “Can you show me what happened?” your answer should come from records, not from memory.

A calm communication style goes a long way

The law sets the minimum. Good administration usually requires a little more.

You don’t need to narrate every small transaction. But you should notify beneficiaries of major developments, especially when the trust holds real estate, a family business, or income-producing property. Silence creates suspicion faster than most trustees realize.

That’s one reason trustees benefit from thinking like a careful manager, not just a signer on an account. A Texas trust administration lawyer can help define what must be disclosed, what should be shared voluntarily, and what needs to be documented in writing so your actions line up with your fiduciary duties in Texas.

When a Formal Trust Accounting Is Required in Texas

A formal accounting isn’t required every time a beneficiary asks a question. Texas law has specific triggers.

Under Texas Trust Code § 113.151, a beneficiary can demand a formal accounting from a trustee, generally not more than once every 12 months, and this framework is tied to Texas’s adoption of Uniform Trust Code principles in 2005 (Texas CPA article on trustee duties and accounting). The rule tries to protect both sides. Beneficiaries get oversight, and trustees get protection from constant, repetitive demands.

Beneficiary demand

This is the most common trigger.

If a beneficiary with the proper interest makes a valid demand, the trustee generally must provide a written statement of accounts within 90 days, unless a court allows more time. That demand right is usually limited to once every 12 months.

For trustees, that means timing matters. A request that feels informal may still deserve prompt attention. Don’t ignore it because it came by email or sounded casual. Review it, confirm whether it qualifies, and calendar the response deadline.

Trust termination

When a trust is ending, the need for transparency becomes more immediate.

Beneficiaries usually want to know:

- what assets remained at the end,

- what expenses were paid before closing,

- what distributions were made,

- and whether the trustee took compensation.

A final accounting helps close the file the right way. It reduces confusion, protects the trustee, and creates a clean record if questions arise later.

Change of trustee

A handoff between trustees is another key moment.

If one trustee resigns, dies, is removed, or is replaced, the incoming trustee needs a clear financial picture. The outgoing trustee also needs documentation showing what property was on hand and what actions were taken during that trustee’s administration.

Consider the scenario of passing a relay baton. If neither runner knows exactly where the baton is, the race goes badly.

What trustees should do when a request arrives

When you receive a request for an accounting, use a simple process:

- Confirm the requester’s status. Make sure the person is a beneficiary with the right to request information.

- Check the trust terms. The trust document may address accounting procedures or content.

- Review the timeline. Determine whether a formal accounting was already provided within the prior 12 months.

- Gather records immediately. Don’t wait until the deadline gets close.

- Decide whether counsel is needed. If the request is broad, disputed, or tied to tension among family members, legal review is wise.

A helpful resource on the demand process is this page on how to get trust accounting in Texas, which can also help trustees understand what beneficiaries may be expecting.

Why waiting is risky

A delayed response often makes a manageable request feel adversarial. Beneficiaries may assume records are missing, money was mishandled, or the trustee is hiding something.

If you need more time to assemble records, communicate that early and clearly. Silence usually creates more problems than the accounting itself.

For a trustee handling ranch property, a rental house, or royalty income, preparing a formal accounting can take time. But time spent organizing records is still better than defending a preventable court dispute later.

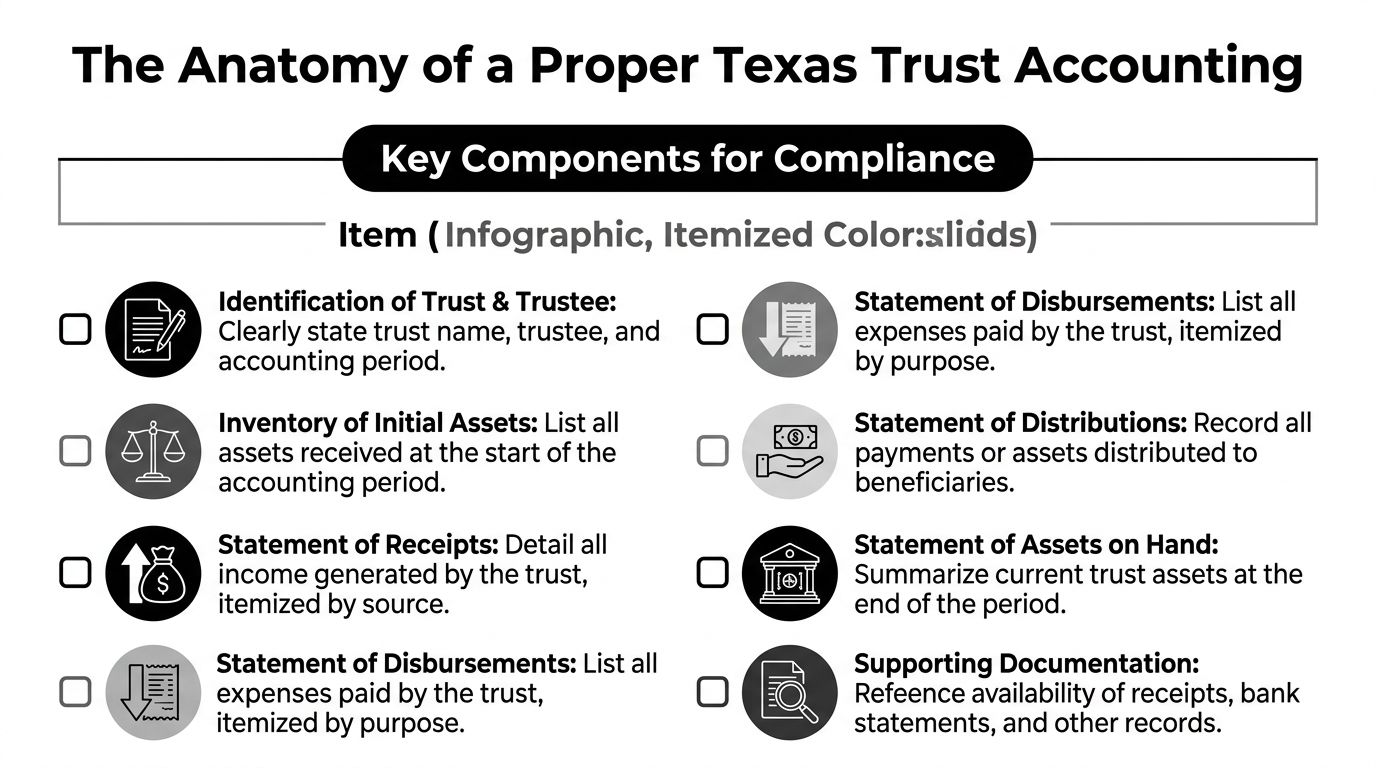

The Anatomy of a Proper Texas Trust Accounting

A proper accounting is more than a stack of bank statements. Bank statements show activity. A statutory accounting tells the story behind the activity.

Texas Trust Code § 113.152 requires specific content. A Texas trust administration resource explains that a compliant accounting must include seven key elements and that trustees must respond to a valid demand within 90 days (what a Texas trust accounting must include).

The seven required content areas

Here is the heart of a formal accounting under Texas law:

- All trust property that came into the trustee’s possession

- Complete receipts and disbursements

- Trustee compensation

- Agent fees

- Distributions to beneficiaries

- Property on hand at the end of the period

- Other material matters

That list sounds technical, so let’s make it practical.

What each item means in real life

| Required item | Plain-English meaning | Why it matters |

|---|---|---|

| Property received | What assets came under the trustee’s control | Shows the starting universe of trust assets |

| Receipts | Money or property coming in | Tracks income, sale proceeds, refunds, or other inflows |

| Disbursements | Money going out | Shows bills, taxes, repairs, professional fees, and other payments |

| Trustee compensation | Fees the trustee paid to himself or herself | Lets beneficiaries evaluate reasonableness |

| Agent fees | Payments to lawyers, CPAs, property managers, or others | Shows who was hired and what trust funds paid for |

| Distributions | Payments or transfers to beneficiaries | Confirms who received what |

| Property on hand | What remains at the end | Gives the current picture of the trust |

Why bank statements alone usually aren’t enough

A bank statement might show “withdrawal” or “deposit,” but it usually won’t tell the beneficiary whether the expense was a roof repair, property tax payment, reimbursement, trustee fee, or distribution.

That’s why many trustees run into trouble when they think, “I’ll just send monthly statements and be done.” In some settings, detailed corporate trustee statements may satisfy a court, but there is no blanket rule. If the statements don’t provide enough detail, the trustee may still be ordered to produce a full accounting.

A practical checklist for trustees

Before sending a formal accounting, ask whether it includes the following:

- Identity details such as the trust name, trustee name, and accounting period

- Asset list showing what property the trustee controlled during the reporting period

- Income entries such as rent, dividends, interest, royalties, or sale proceeds

- Expense entries with enough description to show the reason for each payment

- Compensation disclosure if the trustee took fees

- Professional fee disclosure for lawyers, accountants, appraisers, or managers

- Distribution summary listing what each beneficiary received

- Ending asset summary showing what remains in the trust

- Supporting records available if a court or beneficiary requests backup

If you need a non-legal foundation for organizing records, basic principles of bookkeeping can help you build the habit of categorizing deposits, expenses, and balances consistently. Trustees don’t need to become accountants, but they do need orderly records.

What “sufficient detail” usually looks like

Specificity matters. “Paid expenses” is too vague. “Paid Harris County property taxes for trust residence” is much better.

A good accounting usually identifies:

- date,

- payee or source,

- amount,

- and purpose.

That level of detail helps beneficiaries understand the transaction and helps trustees prove the transaction was proper.

A strong accounting should let an outside reader follow the money without having to guess what each entry means.

A simple example

Suppose the trust owns a rental house in Houston. During the accounting period, the trust receives rent, pays insurance, repairs a fence, pays the property manager, and makes a distribution to one beneficiary.

A proper accounting would not just attach the operating account statement. It would show each receipt, each expense, any professional fees, the beneficiary distribution, and the property still held at the end of the period.

That’s the difference between raw data and a legal accounting.

Common Trust Accounting Mistakes and How to Avoid Them

A common trustee scenario goes like this. You are trying to help your family, bills need to be paid, and the trust administration starts to feel like paperwork you can catch up on later. Then a beneficiary asks a pointed question, and suddenly small shortcuts look much more serious on paper than they felt at the time.

That is why this section matters. Many trust accounting disputes start with preventable habits, not bad intentions.

Mistake one, mixing trust money with personal money

This mistake creates confusion fast. A trust account should function like a separate container. Once trust funds and personal funds are poured together, it becomes hard to show which dollar belonged to whom and why a payment was made.

A trustee may tell himself, “I paid this from my own account for convenience.” The trouble comes later. Was it a trust expense or a personal one? Was reimbursement proper? Did every beneficiary benefit equally? Those questions are much harder to answer if the transaction did not start in a dedicated trust account.

How to avoid it: open a separate trust account and use it consistently. Deposit trust income there. Pay trust expenses from there. If you must advance money personally in an emergency, document the reason, keep the receipt, and record the reimbursement clearly.

Mistake two, confusing the duty to inform with the duty to account

Many trustees frequently get tripped up.

The duty to inform is broad. It usually means keeping qualified beneficiaries reasonably informed about the trust and its administration. The duty to account is narrower and more specific. It means providing a formal accounting when Texas law, the trust terms, or a proper beneficiary request requires one.

A short email update can help satisfy part of your duty to inform. It does not replace a formal accounting.

By the same token, sending a stack of bank statements does not automatically satisfy the duty to account. Texas courts usually expect an organized explanation of what came in, what went out, what is still in the trust, and records that support those entries. A bank statement shows movement. A trust accounting shows meaning.

How to avoid it: treat routine updates and formal accountings as two separate jobs. One keeps people informed. The other proves your administration with enough detail that an outside reader can follow the money.

Mistake three, treating memory like a recordkeeping system

Memory fades. Paper trails do not.

Many family trustees know exactly why they made a payment when they make it. Six months later, that same payment can look mysterious. Two years later, after a death, illness, or family disagreement, it may be impossible to explain without records.

Use a system you will maintain:

- Save monthly statements in one folder, organized by account and date.

- Keep invoices, receipts, and bills for each payment.

- Write a short note for unusual transactions, such as a loan payoff, property repair, tax deposit, or reimbursement.

- Track distributions by date, amount, recipient, and reason.

- Keep copies of letters or emails that explain major decisions to beneficiaries.

The tool matters less than consistency. A spreadsheet may be enough. Software may be better for a larger trust. Either way, your records should let someone else reconstruct the story without relying on your memory.

Mistake four, relying only on bank statements

This is one of the most common misunderstandings, especially for first-time trustees.

Bank statements are only part of the file. They are the scorecard, not the play-by-play. If a beneficiary requests a formal accounting, or a court reviews your work, you may need much more than monthly balances and canceled checks.

A stronger documentation file often includes:

- account statements,

- deposit records,

- invoices and receipts,

- settlement statements for sales or purchases,

- tax returns or tax payment confirmations,

- brokerage statements,

- appraisals or valuation records for unusual assets,

- closing documents for real estate,

- correspondence approving or explaining unusual distributions,

- and a ledger that ties each entry to a date, amount, payee or source, and purpose.

That checklist is where many trustees fall short. They keep raw financial data but not the supporting records that explain why each transaction was proper.

How to avoid it: build each transaction file as if a stranger may need to review it later. If the trust paid for a roof replacement, keep the invoice, proof of payment, and a note identifying which trust property benefited. If the trust made a distribution for health expenses, keep the request, the approval note, and proof of payment.

A short training break can help

Some trustees learn best by hearing the issues discussed aloud. This overview may help you spot weak points in your own process before they become disputes.

Mistake five, going silent when questions start

Silence often gets interpreted as secrecy, even when the trustee is acting with good intentions.

Some trustees avoid communication because they fear saying the wrong thing. Others hope the issue will settle down on its own. Usually, the opposite happens. A beneficiary who receives no explanation may assume the trustee is hiding something, even if the records are perfectly clean.

Regular updates can lower tension before it turns into formal demands. That is especially true when the trust owns real estate, a family business, mineral interests, or investments that require active decisions.

How to avoid it: send plain-language written updates at sensible intervals. You do not need legal jargon. A short report that explains major receipts, expenses, decisions, and expected next steps can prevent misunderstanding. Keep copies of those communications with your trust records.

Mistake six, waiting too long to ask for help

A trustee does not need to do every part of administration alone. In fact, knowing when to ask for help is part of doing the job well.

Early advice is often useful when:

- The trust owns complex assets, such as rental property, oil and gas interests, or a closely held business.

- Family relationships are strained, and routine decisions may be challenged.

- You inherited poor records from a prior trustee.

- You are unsure whether a request calls for a formal accounting or a more general informational response.

- Tax reporting and trust accounting do not line up cleanly, which happens more often than new trustees expect.

A lawyer can help you determine what Texas law requires, what the trust instrument changes, and what records will best support your decisions. A CPA or bookkeeper can help organize transactions into a format that is easier to defend. The Law Office of Bryan Fagan, PLLC is one example of a Texas firm trustees may consult for guidance on administration and accounting questions.

Can Trust Accounting Be Waived or Modified

This question usually comes from a tired trustee. “The trust says I have broad discretion. Doesn’t that mean I can limit what I have to provide?”

Sometimes the answer is partly yes. Sometimes it’s no.

The trust document matters, but it doesn’t control everything

Texas trust instruments can modify many administrative details. A well-drafted trust may shape how reports are delivered, what timing applies in some situations, or how much detail is expected beyond the default rules.

But the trust document doesn’t erase every fiduciary obligation. Some duties remain protected by Texas law, including the non-waivable duty to inform.

That means a trustee should be cautious about reading broad discretion language as permission to stay silent or vague.

Formal accounting and informal reporting are different problems

A trustee may be able to argue that a certain report format satisfies the trust terms. That’s different from arguing that no useful information needs to be shared at all.

This distinction matters most when the trust is silent or when a trustee has been sending account statements that show balances but not context.

The gray area with corporate trustee statements

Courts in Texas are sometimes asked whether standard corporate trustee statements satisfy the formal accounting requirements of §113.151. A fiduciary litigation discussion notes that there is no blanket rule, and courts may look at the trust’s terms and the level of detail provided. Trustees who rely on thin or generic statements may still be compelled to produce a fuller statutory accounting (discussion of corporate trustee statements and statutory accounting).

That issue matters to individual trustees too. If a bank or brokerage generated monthly statements, that doesn’t automatically mean your legal duty is satisfied.

Practical decision rules

If you’re trying to decide whether reporting can be modified, use these questions:

- Does the trust expressly address accountings or reports

- Are you still providing enough detail for beneficiaries to understand transactions

- Would an outside reader know why money moved, not just that it moved

- Are you relying on statements that lack explanations for fees, distributions, or decisions

If the answer to the last two questions is no, your current approach may be too thin.

The safer approach is to assume that minimal paperwork often creates maximal conflict.

A Texas estate planning attorney can help draft trust terms that reduce confusion on the front end. A Texas trust administration lawyer can help interpret those terms once administration begins, especially when a beneficiary argues that existing statements are not enough.

Remedies for Noncompliance with Accounting Rules

When a trustee fails to provide a proper accounting, the problem rarely stays small. Delay changes the posture of the case.

A beneficiary who feels ignored often moves from asking questions to seeking court intervention.

What can happen

Texas law provides remedies when a trustee doesn’t comply. The statutes identified in the verified material explain that failure to provide a proper accounting can lead to court action under Texas Trust Code § 113.151 and remedies for breach of trust under § 114.008, with attorney fees available under § 114.064.

That cause-and-effect chain is straightforward:

- No accounting after a proper demand may lead to a petition asking the court to compel one.

- Poor records or incomplete reporting may support a claim that the trustee breached fiduciary duties.

- A serious breakdown in trust may lead beneficiaries to seek surcharge, removal, or other relief.

Why proactive compliance costs less

A trustee usually spends less time and money organizing records early than defending poor administration later.

Even when the trustee acted in good faith, weak documentation makes defense harder. Courts and beneficiaries look for proof, not intentions.

For beneficiaries dealing with stonewalling or incomplete responses, this resource on a trustee refusing to provide accounting in Texas explains the dispute posture that can follow.

Courts are far more likely to trust a trustee who can produce organized records than one who says, “I know I handled it correctly.”

The practical takeaway

If you’re a trustee, don’t treat accounting as optional paperwork. Treat it as part of your legal protection.

If you’re a beneficiary, don’t assume confusion is harmless. Incomplete or delayed information can be a warning sign that warrants prompt legal review.

Get Trusted Guidance for Your Texas Trust Administration

Trust accounting gets easier once you stop viewing it as a mystery and start viewing it as a system. Keep trust funds separate. Track each transaction. Communicate important developments. Respond carefully when a formal accounting is requested.

That approach protects both the beneficiaries and the trustee.

When legal guidance makes sense

You should strongly consider speaking with a lawyer if any of these apply:

- The trust owns unusual assets such as business interests, ranch land, rental property, or mineral rights.

- A beneficiary has already questioned your actions or asked for detailed records.

- You replaced a prior trustee and inherited disorganized files.

- The trust document is unclear about reporting duties.

- You’re deciding how to modify a trust in Texas or whether the trust’s terms change default accounting rules.

- There’s overlap with probate, guardianship, or estate planning issues that affect administration.

Families often need more than one answer at once. A trust may connect to probate administration, incapacity planning, guardianship concerns, or long-term asset preservation. That’s why trustees and beneficiaries often benefit from coordinated help from a Texas estate planning attorney who understands both documents and disputes.

If you’re trying to act carefully, asking questions early is not a sign of weakness. It’s one of the best ways to fulfill your fiduciary duties in Texas and reduce the chance of conflict later.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including estate planning, probate, guardianship, asset protection, trust administration, and trust disputes.