Managing a loved one’s trust can feel overwhelming. Many people accept the role of trustee because a parent, spouse, or sibling trusted them, then discover they’re expected to keep records, answer questions, and stay within Texas law while family emotions run high.

If you’re a trustee, you may be wondering whether your notes, bank statements, and email updates are enough. If you’re a beneficiary, you may be asking a simpler question: “Why can’t I just see what happened to the trust assets?rdquo; A formal accounting trust texas issue often starts there. Not with fraud, but with uncertainty, silence, or records that don’t tell the full story.

Texas law gives both sides a framework. It tells trustees what they must provide when a proper demand is made, and it gives beneficiaries a way to ask for meaningful information. Used well, a formal accounting can reduce suspicion, clarify decisions, and protect a family’s legacy.

What a Formal Trust Accounting Means in Texas

Being named trustee often feels like both an honor and a weight. You’re supposed to manage property for someone else’s benefit, and you’re expected to do it carefully, fairly, and transparently. One of the clearest ways Texas law measures that transparency is through a formal trust accounting.

More than a bank statement

A formal accounting isn’t just a list of transactions from a checking account. It’s a legal report that traces the financial life of the trust over a defined period. Think of it as a map that shows where the trust property started, what came in, what went out, what remains, and why.

Under Texas law, private trusts usually do not require an automatic annual accounting. Instead, Texas uses a demand-driven system. A beneficiary can make a written demand, which triggers the trustee’s duty to provide a detailed report that complies with Texas Trust Code requirements. A formal accounting under this framework functions as a “year-end map” of the trust property, which is different from guardianship matters where court-supervised accountings are mandatory, as explained in this discussion of annual trust accounting under Texas law.

That difference matters. Trustees often assume they only need to produce records if a judge orders it. Beneficiaries often assume the trustee must send a yearly package automatically. In many private Texas trusts, neither assumption is quite right.

Why families confuse informal updates with formal accountings

A trustee might send an email saying, “The trust paid property taxes, made one distribution, and still holds the brokerage account and the house.” That may be helpful, but it usually isn’t the same as a statutory formal accounting.

Here’s the practical distinction:

| Type of report | What it usually looks like | Legal value |

|---|---|---|

| Informal update | Email, spreadsheet, summary, conversation | Helpful for communication, but limited protection |

| Formal accounting | Structured report showing trust property, receipts, disbursements, and balances | Designed to satisfy Texas statutory requirements |

An informal report can calm concerns. A formal accounting can do much more. It creates a record that shows the trustee took the duty seriously and can help beneficiaries evaluate whether the trust was managed properly.

Practical rule: If the report wouldn’t let a stranger follow the trust property from the start of the period to the end, it probably isn’t detailed enough to function as a true formal accounting.

What this means in real life

Suppose your mother created a trust. After her death, your brother became trustee. The trust owns a house, an investment account, and some cash. You ask, “What happened this year?rdquo; If he replies, “Everything is fine,” that’s not an accounting. If he sends a document that lists beginning assets, income received, expenses paid, distributions made, and the remaining property on hand, that’s much closer to what Texas law expects.

For trustees, a formal accounting is often protective. For beneficiaries, it’s often clarifying. For both sides, it can reduce the kind of confusion that turns family administration into family litigation.

Beneficiary Rights and Trustee Duties for Accountings

A common family conflict starts like this. A son is serving as trustee because his mother trusted him, not because he is an accountant. His sister, who is also a beneficiary, asks for “the trust records.” He feels accused. She feels shut out. Both may be acting in good faith, yet the tension rises because neither side is sure what Texas law requires.

Texas law gives certain beneficiaries the right to request an accounting, and it places real recordkeeping and disclosure duties on trustees. Those rights and duties exist to protect trust property and reduce suspicion before a family dispute turns into a lawsuit.

Who can ask, and how to ask in a way that gets results

A beneficiary who is entitled to an accounting usually needs to make the request in writing. That point matters. A hallway conversation, a group text, or a vague email often creates confusion about what was requested and when.

A better approach is a written request that identifies the trust, states the time period at issue, and asks for a formal accounting rather than “everything.” For beneficiaries trying to avoid immediate court action, precision often works better than anger. A clear written demand creates a record, gives the trustee a fair chance to respond, and helps everyone focus on the same question: what happened to the trust property during the relevant period?

A helpful starting point is reviewing how a demand for trust accounting in Texas is typically framed and delivered.

That step can protect both sides. Beneficiaries show they are asking for something concrete. Trustees get a clearer roadmap for what they need to gather.

What the trustee’s duty looks like in real life

A trustee’s duty to account grows out of broader fiduciary duties. The trustee must act loyally, manage trust property with care, and treat beneficiaries fairly according to the trust terms. An accounting is one of the main ways a trustee proves those duties were taken seriously.

For a family member serving as trustee without a CPA, this can feel overwhelming. That reaction is normal. Texas law does not expect a trustee to be a forensic accountant. It does expect the trustee to keep records that allow beneficiaries to follow the money and property.

In practical terms, a trustee should be able to explain:

- What property the trust held during the period

- What money came in, such as rent, dividends, interest, or sale proceeds

- What the trust paid out, including bills, taxes, repairs, distributions, and fees

- Whether the trustee paid compensation to himself or herself

- Why major transactions occurred, especially if they affected one branch of the family more than another

An accounting works like a family financial map. If the map has large blank spaces, beneficiaries often assume the worst. Sometimes the actual problem is not theft. It is poor records, missing backup, or a trustee who waited too long to organize the file.

What beneficiaries can do before filing suit

Beneficiaries do not have to jump from concern straight to litigation. In many cases, a few practical steps make the problem clearer and sometimes resolve it.

Start by confirming the fiduciary’s role. Is this person acting as trustee, executor, or both? Families often blend those roles together, but the legal duties are not the same.

Next, send a written request that is specific and reasonable. Ask for the accounting for a defined period. Ask that major transactions, distributions, and trustee compensation be identified clearly. If prior summaries were incomplete, say what is missing. A beneficiary who says, “I need the beginning assets, income received, expenses paid, distributions made, and assets on hand at the end of the period,” is much harder to dismiss than one who says, “You’re hiding something.”

Then give the trustee a fair opportunity to respond. If the trustee answers, but the report is incomplete, follow up in writing and identify the gaps. That record matters if the dispute later reaches court.

Trust accounting and estate accounting are different jobs

Families are often dealing with grief, probate, and trust administration at the same time. Confusion is common.

Trust accountings are governed by the Texas Trust Code. Estate accountings are governed by the Texas Estates Code. A person may wear both hats after a death, but the duties attached to each hat are different. An executor reports on estate property. A trustee reports on trust property.

That distinction matters in practical terms. If a beneficiary demands “the accounting” from the wrong fiduciary, the response may be delayed or incomplete because the request itself was aimed at the wrong role. If you are the trustee, you also need to answer in the correct capacity. A probate inventory does not substitute for a trust accounting.

A practical example

A father dies with a pour-over will and a living trust. His daughter is executor of the estate. His son is trustee of the trust. Their younger brother asks both of them for “all financial records.”

The daughter may be collecting estate assets, handling creditor issues, and working under probate procedures. The son may be managing a trust-owned brokerage account and rental house. Same family. Different duties. Different records.

For beneficiaries, the lesson is simple. Direct the request to the right person, in the right role, and ask for the right report.

For trustees, the lesson is just as important. If you are a family trustee with no accounting background, do not wait for the conflict to grow. Gather statements, receipts, closing papers, tax documents, and distribution records early. If you cannot explain the trust activity clearly, get legal or accounting help before silence starts to look like concealment.

Statutory Requirements for a Texas Trust Accounting

A formal trust accounting is the trust’s ledger and explanation rolled into one. Under Texas law, it should let a beneficiary follow what came into the trust, what went out, what changed form, and what remains. For a family trustee, that can feel like being asked to reconstruct a checkbook, an investment file, and a property history at the same time.

Writers discussing trust accountings have described the work as “very burdensome” and said it can take “many hours,” especially for nonprofessional trustees, and they also report that 70-80% of trust disputes grow out of poor communication rather than fraud [https://www.tx.cpa/news-publications/todays-cpa-magazine/issues/article/january-february-2023/2023/01/11/tell-me-more-tell-me-more]. That does not change the legal standard, but it helps explain why clear records often prevent family conflict before anyone mentions court.

What the accounting needs to show

The easiest way to understand the statute is to read it like a timeline. The accounting should show the trust’s starting point, the important activity during the reporting period, and the ending position.

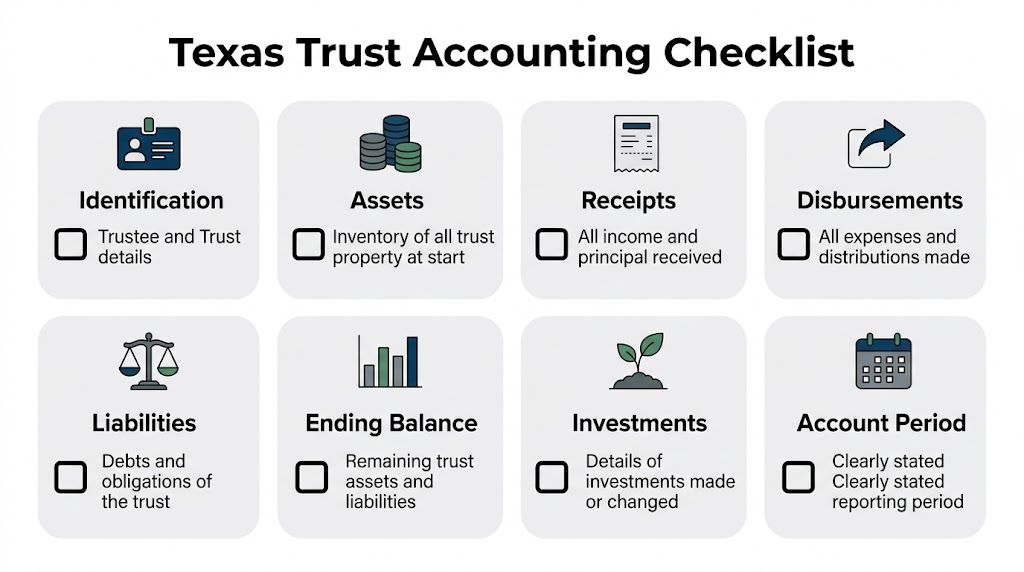

A proper Texas trust accounting generally includes:

Trust and trustee identification

Name the trust, identify the acting trustee, and state the period covered by the accounting.Property on hand at the beginning of the period

List the assets the trust held at the start, such as cash, securities, real estate, business interests, mineral interests, or personal property.Receipts

Show what came into the trust. That may include rent, dividends, interest, sale proceeds, refunds, or other income and principal receipts.Disbursements

Show what went out. Common entries include taxes, insurance, repairs, professional fees, mortgage payments, and distributions to beneficiaries.Liabilities

Identify debts, unpaid expenses, or obligations that still affect the trust.Trustee compensation and reimbursements

If the trustee paid themself a fee or reimbursed personal funds advanced for trust expenses, the accounting should say so clearly.Changes in assets or investments

If an asset was sold, transferred, retitled, or reinvested, the accounting should reflect that change.Property on hand at the end of the period

Show what remains after all activity during the reporting period.

That list matters because a beneficiary is entitled to more than a stack of statements. Statements are raw ingredients. An accounting is the finished report.

If you want a practical explanation of what trustees usually need to gather and how beneficiaries often frame the request, this guide on how to get a trust accounting in Texas can help.

What this looks like in a family trust

Take a common family example. The trust begins the year with a rent house, a brokerage account, and $18,000 in a trust checking account. During the year, the trustee collects three months of rent, pays insurance and plumbing repairs, sells the house, deposits the net sale proceeds, and later makes a health-related distribution to one beneficiary because the trust permits it.

A proper accounting should let the reader trace each of those steps without guessing. The house should not vanish from the asset list without explanation. The report should show that it was sold, when it was sold, and how the proceeds were handled. If the cash balance drops, the accounting should identify whether the reduction came from taxes, repairs, distributions, trustee compensation, or something else.

That level of clarity protects everyone. A careful trustee can show faithful administration. A concerned beneficiary can review the report without assuming the worst from an unexplained transfer.

Common points of confusion

Family trustees often run into the same trouble spots, and each one creates suspicion faster than many trustees expect.

| Issue | Why it causes trouble | Better approach |

|---|---|---|

| Mixed records | Trust and personal expenses end up in the same folder or account | Keep a separate trust account and separate files from the beginning |

| Missing descriptions | Entries only say “transfer” or “expense” | List the payee, date, amount, and purpose |

| No asset values or descriptions | Beneficiaries cannot tell what property existed or whether it was preserved | Include beginning and ending descriptions that identify each asset clearly |

| Unexplained large transactions | A sale, withdrawal, or fee appears without context | Add a short note and keep the supporting document with the accounting file |

A sound accounting should answer the next reasonable question before the beneficiary has to ask it.

If you are a trustee without a CPA

Many family trustees worry that they are already behind because they are not accountants. Usually, the first job is simpler than that. Get the records into order before you try to make them elegant.

Start with the documents that tell the story:

- Bank statements for each trust account

- Brokerage statements for trust investments

- Closing papers for any sale or purchase involving trust property

- Invoices and receipts for taxes, insurance, repairs, and professional fees

- Distribution records showing who received funds, how much, and why

- Prior asset lists or trust schedules if any were prepared earlier

A spreadsheet is often enough if it is accurate and tied back to the source documents. The goal is not polished formatting. The goal is traceability. If a beneficiary asks, “What happened to the house sale proceeds?rdquo; your records should let you answer that in minutes, not weeks.

If you are a beneficiary reviewing an incomplete accounting

A beneficiary does not need to file a lawsuit the moment an accounting arrives with holes in it. Start by checking whether you can follow the money and the assets from beginning to end. If you cannot, identify the gap with precision.

For example, ask whether the accounting shows:

- the beginning assets,

- each major receipt and disbursement,

- an explanation for asset sales or transfers,

- trustee fees or reimbursements,

- and the ending assets still held by the trust.

If one of those pieces is missing, your next step is usually a focused written follow-up, not a broad accusation. Ask for the missing category, the dates involved, and the backup needed to make the report understandable. That approach often resolves the problem faster and creates a cleaner record if court action later becomes necessary.

How to Request or Prepare a Formal Accounting

When families search for formal accounting trust texas, they usually want to know one practical thing. What do I do next?

The answer depends on your role. A beneficiary needs to make a proper written request. A trustee needs to gather records and respond in a way that effectively resolves the issue instead of deepening it.

If you are the beneficiary

A good request is firm, specific, and professional. It doesn’t need drama. It needs clarity.

A practical path for making the request

Confirm the trust exists and identify the trustee

Make sure you’re directing the request to the acting trustee, not a sibling who used to help, a family friend, or the executor of a separate estate.Put the demand in writing

A letter is usually better than a text. Identify yourself, the trust, and your request for a formal accounting.Keep the request focused

Ask for a formal accounting for a defined period. If you’re concerned about something specific, such as the sale of a house or unexplained fees, say so calmly.Send it in a way you can prove

Beneficiaries often protect themselves by using a delivery method that creates a record of receipt.Keep a copy of everything

Save the letter, proof of delivery, and any response.

If you want a clearer sense of the process before sending the letter, this guide on how to get trust accounting in Texas is a useful practical reference.

If you are the trustee

A trustee’s first instinct is sometimes defensive. That’s understandable, especially when the demand comes from a suspicious or upset family member. But defensiveness usually makes the problem worse.

Start by asking a calmer question: “Can I prove what happened with trust property?rdquo; If the answer is yes, the next task is presentation. If the answer is no, the task is organization.

A workable response process

Gather every account record

Pull statements for trust bank accounts, investment accounts, and any property-related accounts.Build a transaction list

Show money in, money out, transfers, and distributions. Add dates and descriptions.List assets separately from cash activity

Real estate, business interests, and personal property need to be described even if they don’t appear like ordinary checking account transactions.Match unusual entries to backup documents

A large legal fee, roof repair, or trustee reimbursement should tie to an invoice, receipt, or written explanation.Review for readability

If a beneficiary can’t tell what “ACH transfer” means, rewrite the description in plain language.

A calmer response often starts with a simple sentence: “I’m preparing the records and want to provide a complete accounting rather than a partial one.”

A short overview can also help families understand the broader role accountings play in administration:

When trustees should get help

Some trusts are manageable with organized records and careful review. Others are not. A trust that owns rental property, a family business, mineral interests, or mixed investment accounts may require help from a CPA, fiduciary accountant, or Texas trust administration lawyer.

That isn’t a sign of failure. It’s often the responsible choice.

A side-by-side view

| Role | First priority | Common mistake | Better move |

|---|---|---|---|

| Beneficiary | Make a clear written demand | Sending emotional accusations | Ask for a defined formal accounting |

| Trustee | Preserve and organize records | Responding with fragments or silence | Prepare one coherent report |

| Both sides | Reduce uncertainty | Treating every question as a personal attack | Focus on records, timing, and clarity |

Families often repair trust breakdowns when one side stops arguing about motives and starts organizing facts.

Common Accounting Mistakes and Penalties for Trustees

A common Texas trust dispute starts in a much more ordinary place than many families expect. A son serving as trustee uses his personal spreadsheet instead of a formal ledger. A daughter asks why $25,000 left the account. He knows the money went to roof repairs on trust property, but he cannot find the invoice, the check image, or the note he meant to save. What felt like simple family administration now looks suspicious because the paper trail is thin.

That is how many accounting problems begin. Not with fraud, but with disorganization, delay, and incomplete explanations. For a family member serving as trustee without a CPA, that distinction matters. Good intentions do not replace records.

Four mistakes that create serious trouble

Mixing trust assets with personal funds

Trust property should move through trust accounts, not a trustee's personal checking account, not a joint family account, and not a business account used for unrelated expenses. A trustee needs a clean lane for trust money.

The easiest analogy is a set of labeled folders. If every trust transaction stays in the trust folder, you can answer questions. If receipts, deposits, and reimbursements are scattered across three drawers, you may still know what happened, but proving it becomes difficult.

This mistake often shows up in everyday ways. A trustee pays a trust bill with personal funds and forgets to document the reimbursement. Or trust income gets deposited into the wrong account "just for now." Temporary shortcuts often become permanent record problems.

Ignoring or delaying a proper accounting request

Silence creates pressure fast. Beneficiaries usually assume the worst when a written request is met with no response, vague promises, or partial records sent weeks apart.

A trustee does not need to be perfect on day one. A trustee does need to respond, preserve records, and work toward a complete accounting. If more time is needed, say so plainly and give a realistic date. That kind of response often lowers tension because it shows the trustee is handling the job seriously.

Sending a stack of documents instead of a usable accounting

Boxes of bank statements are not the same as an accounting. Neither is a long email with scattered attachments.

A proper accounting should let a beneficiary follow the story of the trust: what came in, what went out, what the trust owned at the start, what it owns now, and why major changes occurred. If asset values are missing, trustee compensation is unexplained, or a sale of property appears with no supporting detail, the accounting may still be inadequate even if it is hundreds of pages long.

For a nonprofessional trustee, this is a common point of confusion. The goal is not to overwhelm the beneficiary with paper. The goal is to make the trust's financial history understandable.

Treating communication as optional

Numbers alone rarely settle family concern. If a ranch was sold, a brokerage account was closed, or one beneficiary received a larger distribution because the trust allowed it, a brief written explanation can prevent a minor question from turning into a claim of misconduct.

That does not mean the trustee must debate every decision. It means the trustee should explain major actions clearly enough that a beneficiary can connect the transaction to the trustee's duty.

What beneficiaries can do before filing suit

Beneficiaries often have more room to act than they realize before a lawsuit is filed. The goal at this stage is to narrow the dispute. Is the problem delay, missing backup, unclear categories, or signs of actual misuse?

A measured approach often works better than an angry one:

Send a focused follow-up letter

Identify the missing items with specificity. Ask for the closing balance of a named account, support for trustee fees, the reason for a large transfer, or the value assigned to a piece of real property.Ask for a correction, not just "more information"

If the accounting lists "miscellaneous expenses" for $18,400, ask for the itemization. If it shows a distribution with no recipient listed, ask the trustee to identify who received it and why.Request a meeting with records available

Some disputes come from poor labeling, not theft. A meeting where the trustee brings statements, invoices, and closing documents can answer questions quickly.Have counsel send a letter if the response stays incomplete

A lawyer's letter often changes the tone. It also helps define whether the trustee is behind or refusing to meet legal duties.

For a broader explanation of the standards that apply, this overview of fiduciary duties of trustees gives useful context.

Disputes over accountings often resolve before trial, and mediated resolutions can reduce cost compared with full litigation, according to this article on why an accounting may be needed in trust disputes.

If a trustee cannot show the path of the money, the dispute is no longer only about family tension. It is about proof.

What penalties may follow

Texas courts have several remedies when a trustee fails to keep proper records or provide a sufficient accounting. The remedy depends on what happened. A careless trustee is different from a dishonest one, but both can face serious consequences.

Possible outcomes can include:

- a court order requiring a proper accounting

- removal of the trustee

- denial or reduction of trustee compensation

- personal liability for losses caused by a breach

- payment of attorney's fees in the right case

For family trustees, the practical lesson is simple. If you are behind, get organized now. Open a separate trust account if one is missing. Rebuild the ledger from statements and receipts. Ask a CPA or trust administration lawyer for help if the trust owns real estate, business interests, mineral interests, or years of mixed transactions.

That is not an admission of wrongdoing. It is often the step that protects both the trustee and the family's legacy.

When to Seek Court Action for a Trust Accounting

Court should usually be a last resort, not the first move. But there are times when waiting only makes things worse. If a trustee refuses to provide a formal accounting, provides something plainly incomplete, or uses delay as a tactic, legal action may be the step that protects the trust and the beneficiaries.

Red flags that suggest the matter is no longer informal

Some warning signs are hard to ignore:

- No response to a proper written demand

- Repeated promises with no delivery

- Large transactions with little or no explanation

- Disappearing assets or unexplained reductions in value

- Distributions that appear inconsistent or self-serving

- Hostility whenever records are requested

One red flag alone doesn’t always mean wrongdoing. But a pattern often does. Beneficiaries should pay close attention when the trustee has the information and still won’t produce it.

What a court action may involve

Texas law allows beneficiaries to ask the court for relief when a trustee fails to provide a required accounting. In practical terms, that usually means filing a petition asking the court to order the trustee to produce a proper accounting and, if needed, to address related breaches of trust.

A court case may focus on one issue at first. Produce the accounting. Once the accounting appears, additional issues may come into focus, such as unauthorized distributions, excessive fees, self-dealing, or poor investment handling.

Mediation can still be the better path

Filing a case doesn’t always mean the matter ends in a trial. Many courts and lawyers use mediation to resolve trust disputes after the issues have been framed more clearly. Mediation can work well when the beneficiary wants transparency and correction, and the trustee wants to avoid a prolonged public fight.

That approach is often especially useful in family trusts. Litigation may decide the legal issues, but it rarely repairs personal relationships. A mediated accounting, paired with a corrective plan, sometimes does more good.

What trustees should understand

A court petition is not just a paperwork annoyance. It signals that the trustee’s handling of the trust may now be judged by a third party with authority to compel compliance. If you’re a trustee facing that risk, early legal advice matters. A Texas trust administration lawyer can help assess whether the records are sufficient, whether supplementation is needed, and whether a negotiated solution can avoid deeper exposure.

What beneficiaries should understand

Court action can be necessary, but it takes time, energy, and money. A beneficiary should enter that process with clear goals. Do you want records? An explanation? Removal of the trustee? Repayment to the trust? A better legal strategy starts when the objective is specific.

Get Trusted Guidance on Your Texas Trust Matter

Trust accountings are about more than numbers. They’re about accountability, communication, and family confidence during a time that often feels fragile. A well-prepared accounting can protect a trustee who acted properly. It can also protect a beneficiary who needs answers before distributions, decisions, or losses become harder to address.

If you’re a trustee, the safest course is usually proactive organization. Keep trust property separate. Maintain clear records. Document why major decisions were made. Ask for help early if the trust holds complicated assets or if family tension is building.

If you’re a beneficiary, don’t assume silence means you have no rights. A calm written demand, a careful review of the response, and strategic legal advice can often move the matter forward before the conflict becomes more expensive.

These issues also connect to larger planning concerns. Families dealing with a trust often also need help with estate planning, probate, guardianship, or asset protection. A problem in one area can spill into another. For example, poor trust administration may delay distributions, complicate tax planning, or intensify probate disputes involving the same relatives and assets.

The law gives structure to these moments, but families still need judgment. Not every incomplete accounting is fraud. Not every trustee delay is innocent. The hard part is telling the difference early enough to protect the trust and the people who depend on it.

If you’re managing a trust, reviewing a trustee’s actions, or trying to avoid a dispute before it reaches court, specialized advice from a Texas trust administration lawyer or Texas estate planning attorney can make the process clearer and safer. The same is true if you’re asking broader questions about fiduciary duties in Texas or even how to modify a trust in Texas as family circumstances change.

If you’re managing a trust or planning your estate, contact Law Office of Bryan Fagan, PLLC for a free consultation. Our attorneys provide trusted, Texas-based guidance for every step of the process, including trust administration, probate, guardianship, estate planning, and asset protection. Whether you’re a trustee trying to comply with Texas law or a beneficiary seeking clear answers, our team can help you protect your rights and your family’s legacy.